GBP/EUR Week Ahead Forecast: Against the Ropes and at Mercy of ECB

- Written by: James Skinner

- GBP/EUR supported at 1.1645, stronger support below 1.16

- GBP/EUR against ropes, at risk of further losses short-term

- If ECB foments more market hawkish interest rate outlook

- But as inflation risk rises, GBP/EUR’s downside diminishes

- GBP/EUR trend matters for BoE's CPI outlook, rate stance

- ECB key ahead of UK's wage data & June 16 BoE decision

Image © Adobe Images

The Pound to Euro rate enters the new week with its back against the ropes and the outlook for it hinged upon how the European Central Bank’s (ECB) handles its besiegement at the hands of hawkish financial markets this Thursday.

Thursday’s ECB decision is the foremost determinant of the outlook for a recently softer Pound to Euro exchange rate leading into next week’s UK wage data and the June 16 Bank of England monetary policy decision.

This is because of the direct impact that Thursday’s decision will have on the Euro and the indirect effect it could have on Sterling through knock-on implications for the BoE’s inflation outlook and interest rate stance that could become apparent as soon as the June 16 decision.

With the single currency accounting for just less than half the trade-weighted or overall Sterling, further pressure near current lows could impact the BoE’s rate stance in ways that would provide one more suggestion that the bottom may be increasingly near for the Pound to Euro exchange rate.

“It’s robust to make the initial steps in normalisation to validate the tightening that has already happened in many financial markets,” ECB chief economist Phlip Lane reportedly told the Centre for Economic Policy Research (CEPR) Paris Symposium last Wednesday.

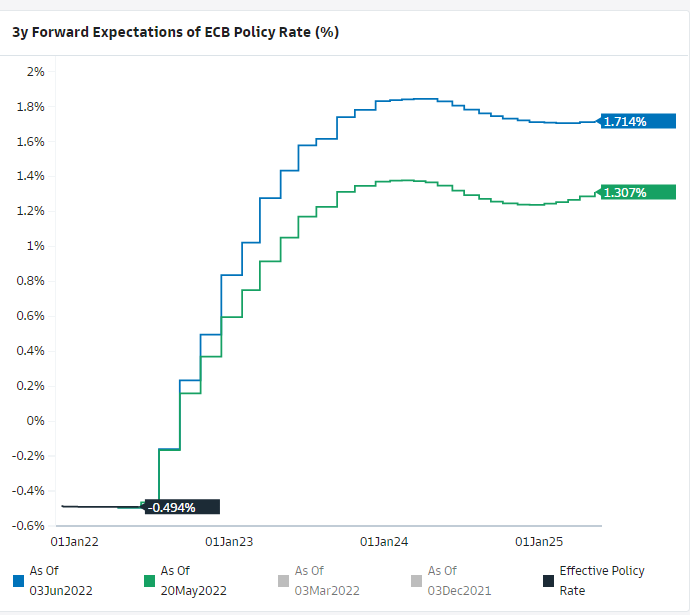

Above: Blue line shows expectations for ECB deposit rate in years ahead as implied by forward-rate-agreements on June 05. Green line shows the same measure of implied expectations on May 20. Source: Goldman Sachs Marquee.

Above: Blue line shows expectations for ECB deposit rate in years ahead as implied by forward-rate-agreements on June 05. Green line shows the same measure of implied expectations on May 20. Source: Goldman Sachs Marquee.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

The Euro would either rise or fall this week according to whether increasingly hawkish markets will be satisfied with any indications of how fast the ECB is likely to lift Eurozone interest rates this summer, as well as any clues about the likely pace of rate rises thereafter.

“While the Euro area activity data flow since the start of the war has been mixed, the incoming information points to much higher and more persistent inflationary pressures than anticipated in the March ECB staff projections,” says Soeren Radde, a senior economist at Goldman Sachs.

“During the press conference, we expect President Lagarde to reiterate the key signals provided in her recent blog post, guiding towards (1) 25bp hikes in each July and September and (2) a data dependent approach, where sequential hikes above the neutral rate might be needed if the Euro area economy overheats as a result of stronger demand,” Radde and colleagues said last week.

Much about the Pound to Euro rate outlook ahead of the next BoE meeting is likely to be determined by the ECB’s inflation forecasts and guidance on interest rates, especially in terms of whether it supports recently escalating market expectations or if it leans against them.

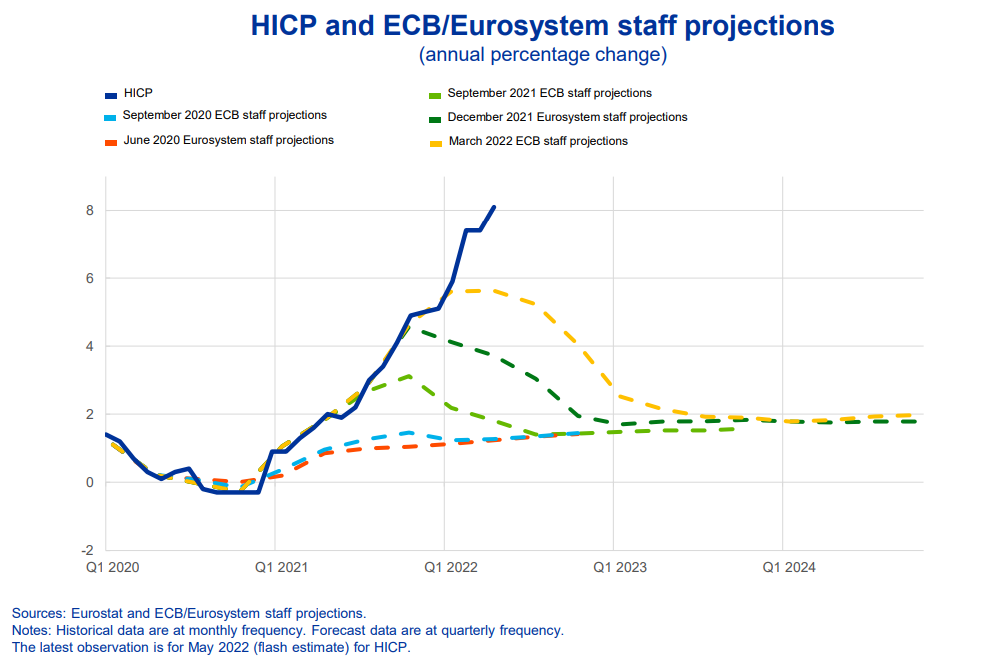

Above: Eurozone inflation path relative to ECB’s various forecasts. Source: ECB. Click image for closer inspection.

Above: Eurozone inflation path relative to ECB’s various forecasts. Source: ECB. Click image for closer inspection.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

In one context Thursday’s guidance and this week's price action will reflect whether or not the ECB wants to fire a shot in what Radde’s colleagues have loosely termed a “reverse currency war,” or if it instead uses its size and weight in a more neighbourly endeavour of leaning against a broader European trend of escalating market expectations for interest rates.

“We argued that the high inflation environment would mean that central banks will be resistant to currency depreciation, in sharp contrast to much of the last cycle. We call this the “Reverse Currency Wars” and think this will be a key theme in FX and rates markets this year, potentially leading to “competitive hikes” and heightened rates and FX volatility,” write Michael Cahill, a G10 FX strategist at Goldman Sachs in a May research note.

This is all after Eurostat figures revealed last week that Europe’s inflation rate leaping to a new record of 8.1% in May, leading markets to anticipate a 0.65% increase in the ECB’s key interest rates by July and a total 1.25% increase before December, which is relevant in determining the outlook for Sterling.

“We estimate the size of policy rate adjustment required to offset the inflationary impact of a 1ppt movement in the TWI is on average around 10bp for the G10, though it varies slightly depending on the currency's role in each country's financial conditions and the degree of exchange rate pass-through,” Cahill and colleagues also said in May.

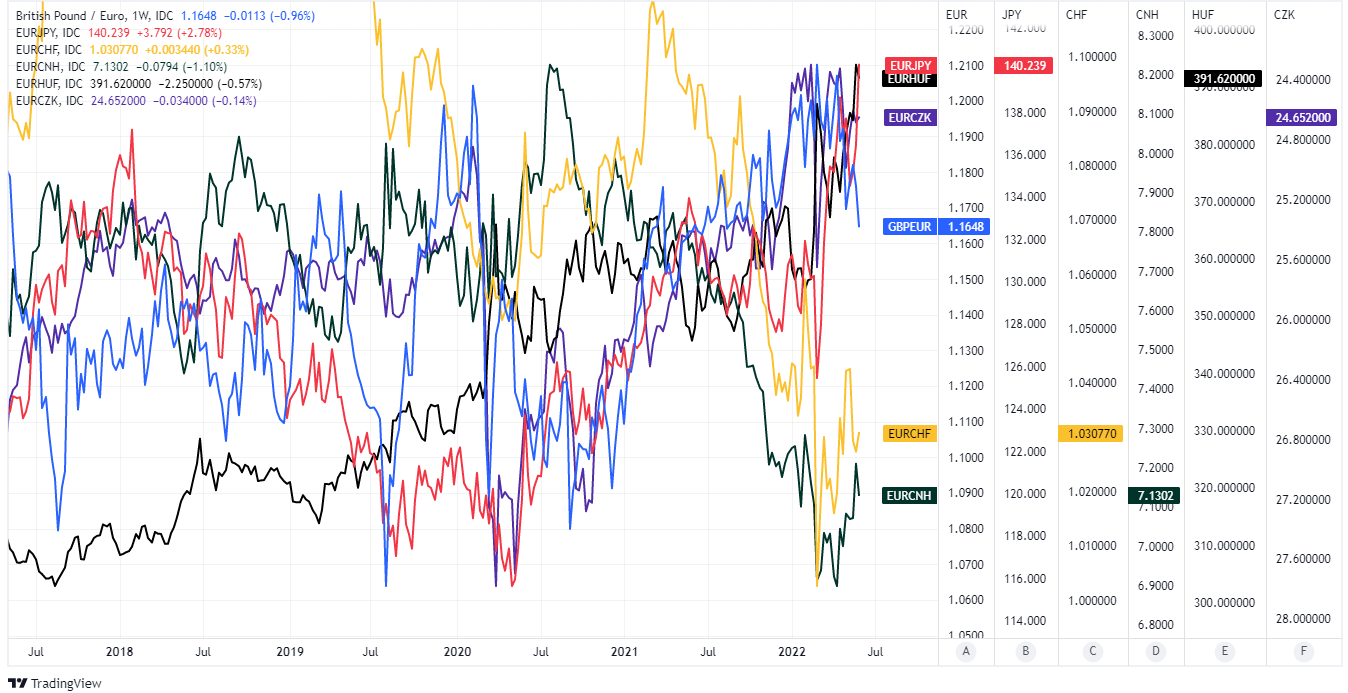

Above: Pound to Euro rate shown at weekly intervals alongside exchange rates for Euro relative to other important parts of the ECB’s trade-weighted or overall measure of the European single currency. Click image for closer inspection.

Above: Pound to Euro rate shown at weekly intervals alongside exchange rates for Euro relative to other important parts of the ECB’s trade-weighted or overall measure of the European single currency. Click image for closer inspection.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Much now depends for the Pound on the extent to which the ECB signals its agreement with the market on Thursday, and in part because any further pressure on it would potentially impact the BoE’s thinking about inflation and Bank Rate with knock-on implications for GBP/EUR later in June.

“We have to ensure that the inflation we're seeing in the economy - I think most of which but not all is coming from shocks that people understand are from abroad - that that doesn't become established in the economy. That inflation doesn't become the new normal. So interest rates may well have to rise further,” BoE Deputy Governor John Cunliffe told ITV News in an interview last week.

“While I expect interest rates having risen back to above pre-pandemic levels, not to see again the levels we saw over the last 12-months, I also don't think we're heading back to the interest rates of the 1990s," he added.

A hawkish shift at the BoE would be especially likely if wage data out next week suggests that already high pay pressures rose further in the UK during April, which would potentially be enough to see three become five in terms of the number of Monetary Policy Committee members who might then support lifting Bank Rate in a larger than usual 0.50% measure this June.

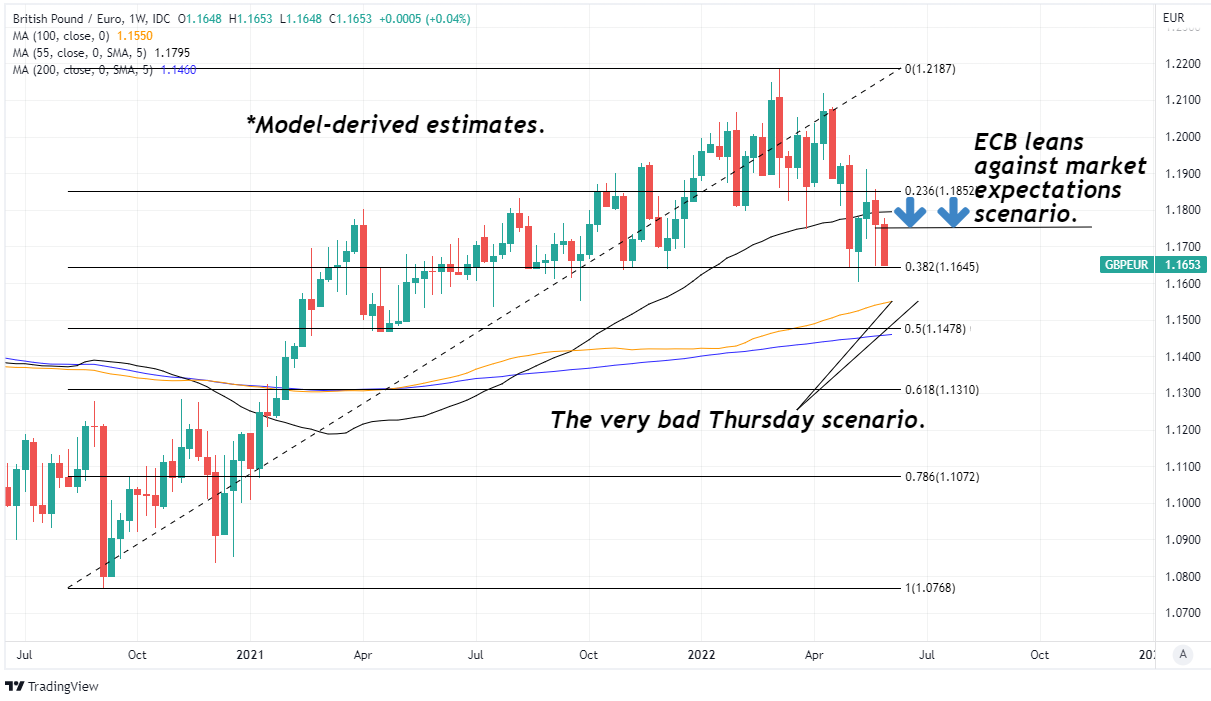

Above: GBP/EUR at weekly intervals with weekly moving averages and Fibonacci retracements of 2020 recovery indicating possible areas of technical support for Sterling and resistance for the Euro. Click image for more detailed inspection.

Above: GBP/EUR at weekly intervals with weekly moving averages and Fibonacci retracements of 2020 recovery indicating possible areas of technical support for Sterling and resistance for the Euro. Click image for more detailed inspection.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Three turning to five would make for a majority decision and a Bank Rate scenario that isn’t even close to being priced-in by markets, making it a potential catalyst for a recovery by the Pound to Euro rate in the weeks ahead.

“While we are forecasting an extensive move higher in EURGBP over the quarters ahead, our tactical signals indicate that the cross is quite stretched,” writes Mark McCormick, global head of FX strategy at TD Securities, in a research briefing last week. “The cross has also overshot its implied level to our risk model, suggesting that it would likely move lower quite quickly if risk appetite continues to consolidate."

The Bank of England has repeatedly cast doubt over market wagers that Bank Rate could rise much further in the months ahead using economic forecasts that inflation would be likely to fall back to a level that is materially below the coveted 2% target in future years if it delivered upon market expectations, although it has also been clear at each step of the way that there are multiple scenarios in which this outlook could change.

And for all of the expressed concerns about the extent to which the ongoing real income squeeze is likely to hamper the economy and inflation during the months ahead, the BoE has also been clear in each and all of its policy statements that “The MPC’s remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework.”

Source: TD Securities. Click image for more detailed inspection.

Source: TD Securities. Click image for more detailed inspection.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes