Euro-Dollar: Growing Risks ECB Underwhelms Expectations

- Written by: James Skinner

Image © European Union - European Parliament, Reproduced Under CC Licensing.

The European Central Bank has recently prepped markets for a pending uplift in its interest rates and chief economist Philip Lane suggested this week that it could now look to “validate” market expectations with actions, although this might have mixed blessing for the Euro to Dollar exchange rate.

Europe’s central bankers have dived headlong into an ongoing debate over whether to lift their negative deposit rate in a typical 25 basis point increment or by a larger 50 basis point measure following an anticipated end to the ECB’s remaining quantitative easing programme next week.

This is the backdrop against which the next round of forecasts will be unveiled on June 09 and the context within which they are likely to be assessed by markets.

“It’s robust to make the initial steps in normalisation to validate the tightening that has already happened in many financial markets,” chief economist Phlip Lane reportedly told the Centre for Economic Policy Research (CEPR) Paris Symposium on Wednesday.

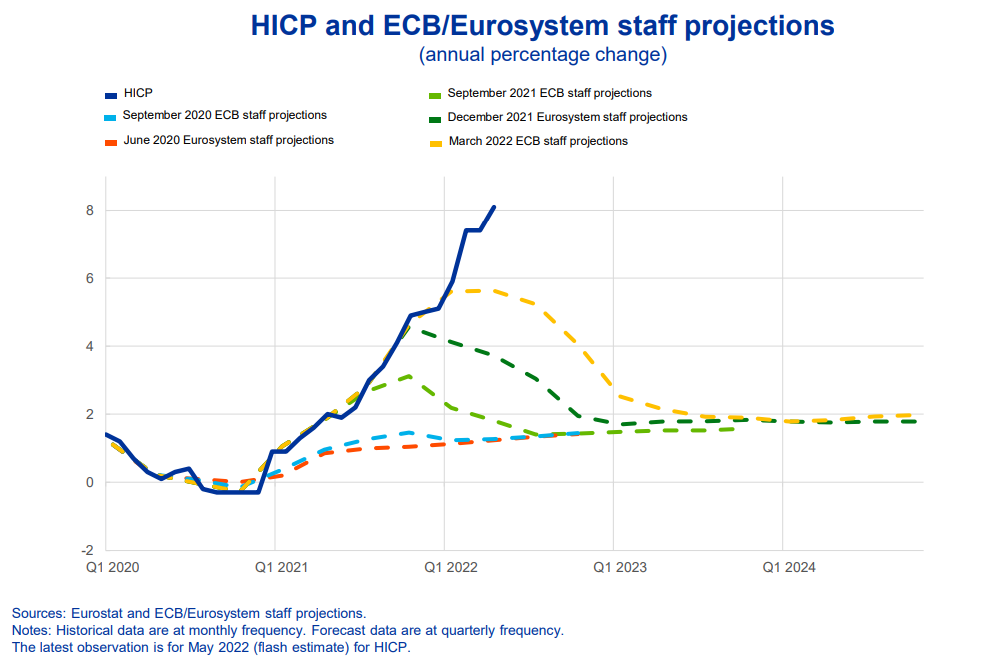

Above: Eurozone inflation path relative to ECB’s various forecasts. Source: ECB.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

The remark is ambiguous with its implication for the likely size of an anticipated July increase in the ECB’s key interest rates and in part because of implied uncertainty in financial markets about exactly how large that move might be.

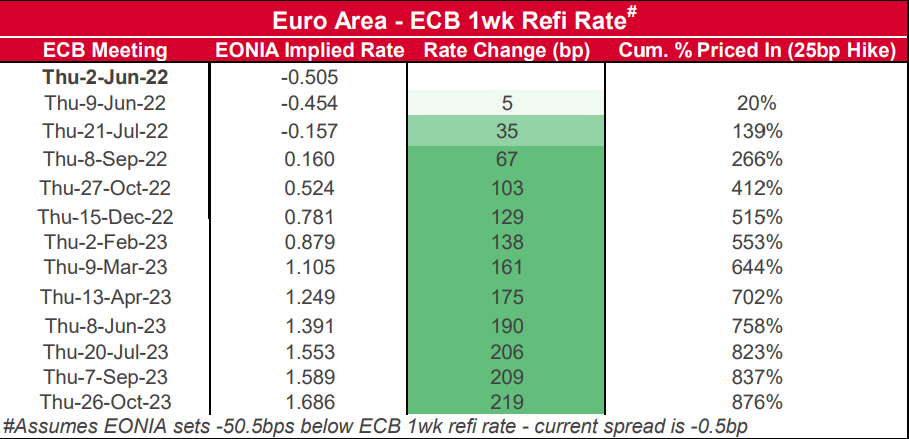

So far financial markets have shifted to price-in a 35 basis point increase in the deposit rate, the rate which commercial banks are charged for depositing money with the ECB, this July and there is a danger that these expectations would rise further following next Thursday’s policy decision.

“An aggressive 180bp in ECB rate hikes are priced through to end-2023, about the same as the Fed, yet it’s hard to see the ECB moving toe to toe,” says Richard Franulovich, Sydney-based head of FX strategy at Westpac.

“The ECB is surely more likely to underwhelm expectations, the region facing more material hardship as sanctions on Russian energy supplies continue to incrementally tighten,” Franulovich and colleagues said on Thursday.

Above: Expectations for ECB deposit rate implied by prices in overnight-indexed-swap markets.

The publicly aired ECB policy conversation has helped lift the Euro from near five year lows in recent weeks and has raised European yields sharply.

"Most of the action happened in rates, and specifically in the Eurozone front-end of the yield curve with some 3+ weekly standard deviation moves: wow!" says Alfonso Peccatiello, writing for The Macro Compass.

"The-ECB-will-never-really-hike mantra is melting under the eyes of bond investors married to a dovish narrative which has been successful for a decade but offers a very bad risk-reward today," he explained in the latest edition.

But for the Euro it’s possible market expectations could soon reach levels that the ECB would find difficult to deliver upon, and potentially as soon as the immediate aftermath of next Thursday’s decision, depending upon how financial markets interpret the new forecasts.

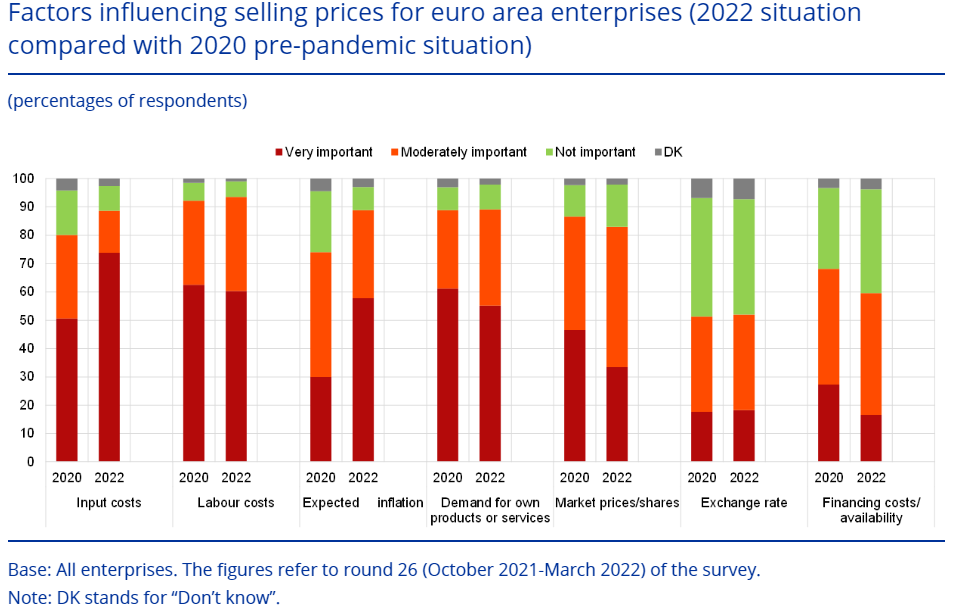

Above: Results from survey of influences on corporate selling prices. Source: ECB.

Above: Results from survey of influences on corporate selling prices. Source: ECB.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

“For now the prospect of advancing German yields, 10-year Bunds are at levels not seen since July 2014, impacting spreads has helped preclude EUR/USD testing 1.0620 support and is encouraging an extension back towards 1.0710,” says Jeremy Stretch, head of FX strategy at CIBC Capital Markets.

The danger for Euro-Dollar may be that by the time of July’s eagerly anticipated interest rate decision, expectations may have become excessive enough to leave the ECB in a position where it’s then apt to disappoint.

But a market disappointment over the eventual delivery of ECB monetary policy actions is not the only risk faced by the Euro.

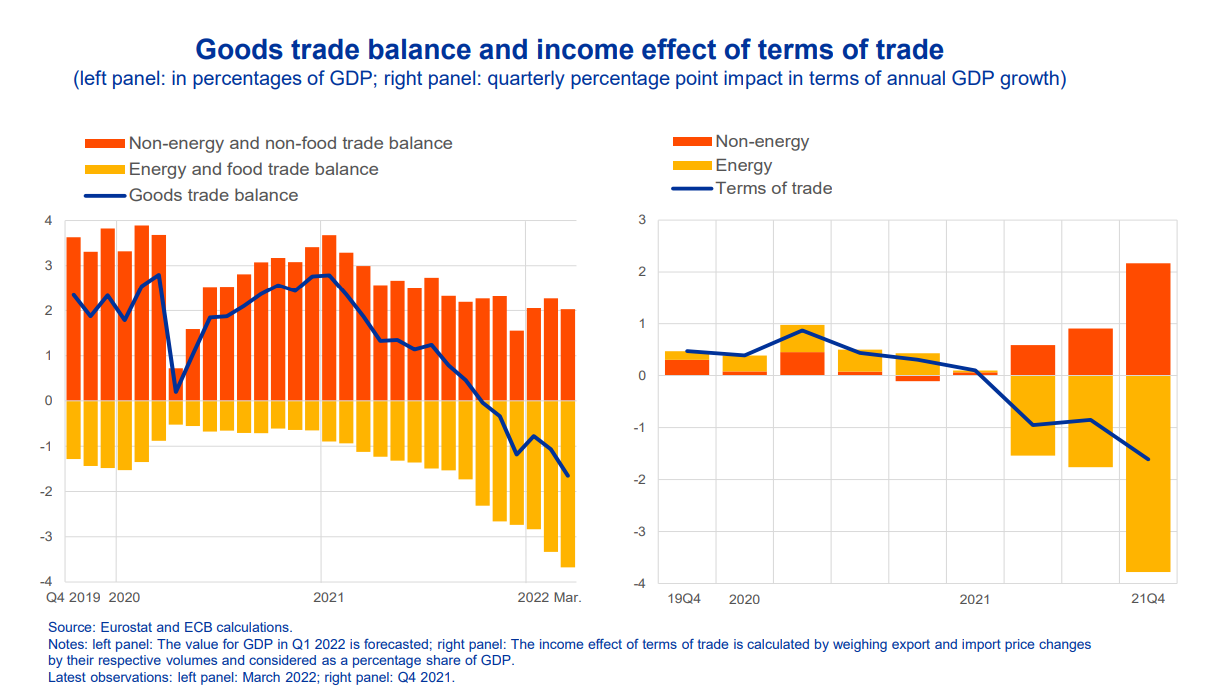

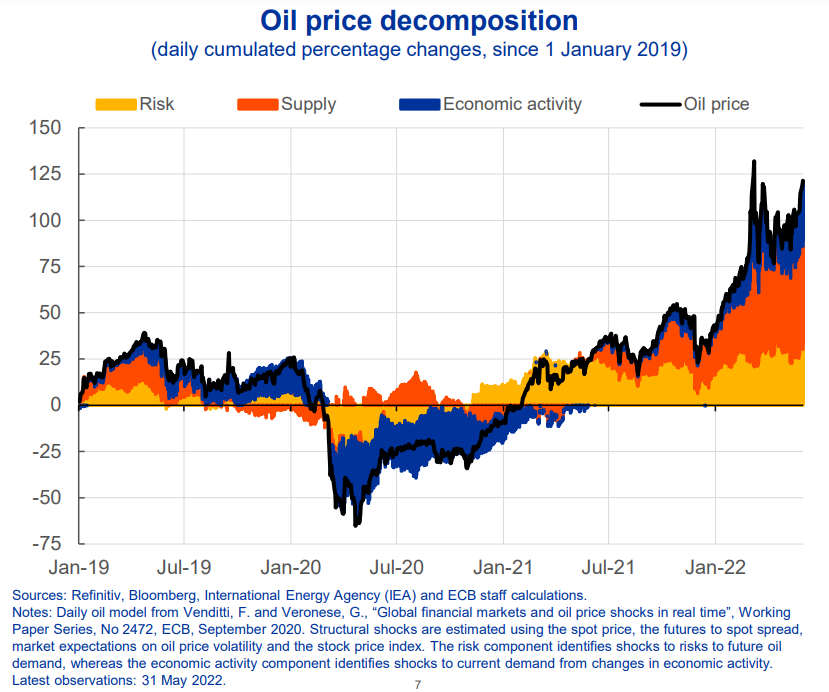

Others include oil prices and their tendency to rise whenever and wherever the Euro rises or the Dollar falls, which lifts manufacturing costs for companies and can meaningfully raise inflation across the world.

Source: ECB.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

This not only exacerbates the deterioration of the Eurozone trade balance, which has flipped from sizable surplus to a deficit during recent quarters, but also raises prices in the U.S. where the Federal Reserve is under immense pressure to counteract those pressures.

Some strategists have suggested that the oil induced aspect of the present inflation cycle could soon become a bit like a red rag to a raging Fed.

“The Fed needs to get serious about rates to deal with the commodity upswing and the ongoing geopolitical shift away from using the dollar towards dollar-priced barter trade,” says Michael Every, a global strategist at Rabobank.

"Take down commodities, especially oil, and you take down inflation and blow up commodity barter trade, and certain EM (and DM) currencies," he added.

Source: ECB.