Pound to Euro Week Ahead Forecast: Pressured Ahead of UK Wages & ECB Rate Cut

- Written by: Gary Howes

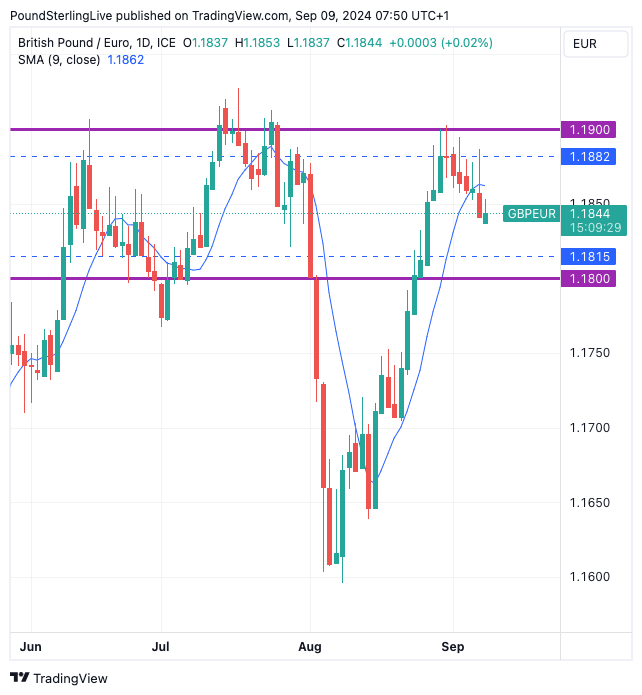

Image © Pound Sterling Live

Pound Sterling is under a spell of short-term pressure against the Euro amidst deteriorating global equity sentiment, but UK wages and GDP figures and an ECB interest rate cut could limit the extent of the selloff.

Last week, we reported September is historically a month in which global equities fall, which can keep the Pound-Dollar and Pound-Euro exchange rates under pressure in the coming three weeks. However, we also pointed out that supportive UK interest rate expectations can limit the downside.

We think price action is verifying this, and any further selling pressure in the Pound to Euro exchange rate (GBP/EUR) should be limited at the first support zone of 1.1815 and then 1.18 (both of which proved supportive during the June-July spell of weakness).

Above: GBP/EUR at daily intervals.

GBP/EUR has dipped below its short-term nine-day moving average, a level that has some useful predictive power for this particular exchange rate: we note that when it breaks below here, it can typically spend up to two trading weeks below it. This will limit recoveries to 1.1862.

A test of the 1.1815 and 1.18 support zones can happen if this Tuesday's UK jobs report is much weaker than expected. The market looks for employment to have risen 84K in the three months to July, with the unemployment rate at 4.1%.

🎯 GBP/EUR year-ahead forecast: Consensus targets from our survey of over 30 investment bank projections. 📩 Request your copy.

However, it will be the wage figures that will potentially be of more significance for the Pound as this is something that Bank of England will be watching closely. The Bank is not expected to cut rates again in September, but there is some debate over whether they will move again in October and November.

A weaker-than-forecast wage print could boost these odds, which will weigh on the Pound. Average earnings is predicted to have risen by 4.1% in the three months to July, down from 4.5%. Wage pressures have been coming down, but some economists are concerned that they are not coming down fast enough.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

If this is the case, then the data can beat expectations and lower the odds of an October rate cut, which can boost the Pound against the Euro and other currencies. "Another decline in nominal pay could ease UK inflation fears and allow the BOE to cut rates later this year, although we still believe that they will cut rates at a slower pace than the ECB and the Federal Reserve," says Kathleen Brooks, an analyst at XTB.

For Pound-Euro, we think any strength will be limited owing to the febrile global sentiment backdrop and look for gains to struggle to make it beyond 1.1882. Note, the exchange rate has not closed above here since July and recent attempts to break and record a daily close above this level have failed.

From a technical perspective, therefore, the data should determine at which end of the 1.1882-1.1815 spectrum the exchange rate trades, and we place low odds of a sustained break on either side of these levels.

Wednesday will see the release of UK GDP figures for July, with the market looking for 0.2% growth, up from the previous month's flat 0% outturn. On paper, the GDP figure is secondary to the wage release, but any sizeable surprises (i.e. more than 0.2pps) can shake the market, with Sterling likely to weaken on any disappointments and rise on any surprising strength.

Note too that the U.S. monthly inflation release is due later in the day, and given the importance of global drivers, this could ultimately prove to be the highlight of the week for Pound exchange rates. Should U.S. inflation undershoot forecasts, market expectations for a 50 basis point rate cut at the Federal Reserve on September 18 will increase, boosting equity markets and supporting Pound-Euro.

However, should the data come in stronger, expect further selling pressures as the odds of a 50bp cut are completely erased, in which case stocks and the Pound can come under further pressure.

Last week, we heard from an influential member of the Federal Reserve's rate-setting committee that although rates need to come down, the path of progress remains dependent on the data. Markets read this as a signal that the Fed is not concerned enough to pursue 50bp cuts and will prefer to stick to more conventional 25bp increments. There is more room for the market to adjust to this view, which would mean softer equity markets, a firmer dollar and a downside bias in the Pound.

ECB in Focus

![]()

Image © European Central Bank, reproduced under CC licensing

Thursday brings the European Central Bank (ECB) decision and an interest rate cut is fully expected by the market. What is less certain is whether or not the central bank will cut rates again in October. Updated guidance will therefore be of more importance to the market than the cut itself.

"Although wage growth is slowing, it is still well above the ECB’s target rate of 2%, and the concern is that wage growth could pick up in Q3, especially in Germany. Thus, while we expect a rate cut on Thursday, the ECB may not provide forward guidance, and instead say that they remain data dependent for the rest of this year," says XM's Brooks.

The odds of an October rate cut were reduced last week after a number of Governing Council members aired their views. "Recent ECB rhetoric suggests a high bar to a follow-up cut in October after a likely September easing," says a note from currency analysts at HSBC.

This matters for euro exchange rates as consecutive rate cuts are not fully 'priced in', meaning such an outcome would necessitate a readjustment lower in Eurozone bond yields and exchange rates. But a pause in October would underpin current levels in the single currency, all else equal.

"The hawks, predictably, point to concerns about still elevated services inflation and wages growth," says HSBC. German Bundesbank President Joachim Nagel is one such hawk, and he said this week that "we shouldn’t prematurely burst into cheers and pat ourselves on the back."

Gediminas Simkus said there are "compelling arguments for an ECB cut in September", citing "structurally sluggish" growth, "clear disinflationary trends" and economic risks which are "tilted downwards".

However, despite this dovish cocktail, he argued that an October rate cut is "quite unlikely" as changes in the upcoming economic projections will likely be unsubstantial.

The market currently views a follow-up October cut as a 1-in-3 likelihood. Should the odds of a cut in October rise in the coming days and weeks, we would anticipate the Euro to weaken.

But given how slim such an outcome is, we think the Euro can remain supported near current levels against the Pound and Dollar.