Pound-to-New Zealand Dollar Week Ahead Forecast: 2.27 Back in Scope

- Written by: Gary Howes

Image © Adobe Images

The Pound is forecast to maintain a constructive trade against the New Zealand Dollar in the short term.

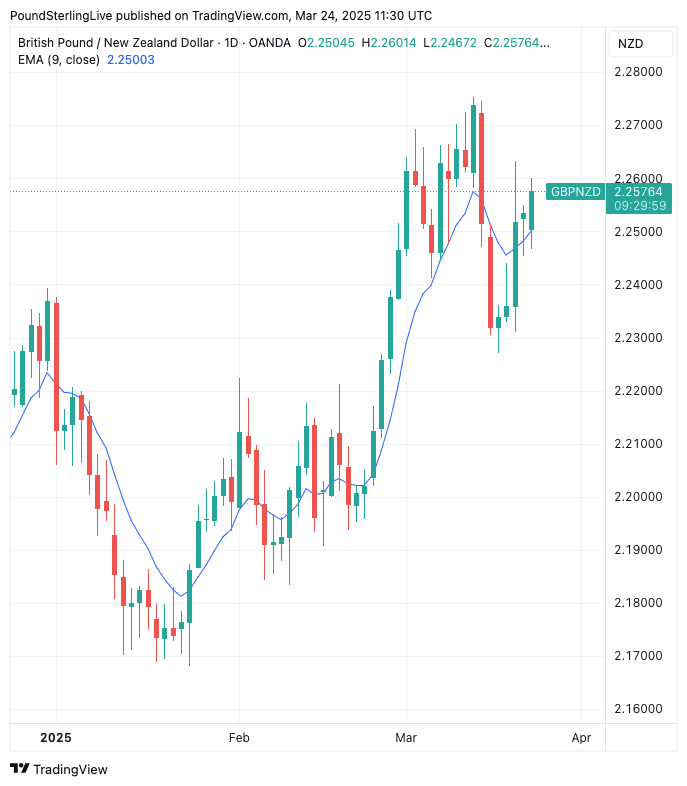

This time last week, we were pondering what was quite an aggressive selloff in the Pound-to-New Zealand Dollar exchange rate (GBP/NZD), which saw it fall from a peak of 2.2754 to 2.2304 in the space of three days.

At the time, we said GBP/NZD was due to a setback in order to unwind heavily overbought conditions, and it looks as though the subsequent weakness was simply this unwind finally occurring.

Above: GBPNZD at daily intervals.

🎯 GBP/NZD year-ahead forecast: Consensus targets from our survey of over 30 investment bank projections. Request your copy.

Weakness attracted dip buyers, and GBP/NZD has since recovered to 2.2576 and is back above the nine-day exponential moving average (EMA).

Above the nine-day EMA GBP/NZD is in a short-term uptrend, which means we expect a retest of levels towards 2.27 in the coming days.

Sterling remains well supported on weakness against the Kiwi, and any setbacks should see support emerge once more at 2.23, as was the case early last week.

Global sentiment support the constructive technical GBP/NZD setup we see guiding price action:

Our top theme for NZD coverage in 2025 has been the currency's ongoing correlation with U.S. stock markets. As these markets have fallen, so too has the New Zealand Dollar, reflecting its well-established 'high beta' to global investor sentiment.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

U.S. stocks have struggled in 2025 as the erratic nature of President Donald Trump's policymaking breeds uncertainty and raises expectations of an economic slowdown.

The April 02 tariff announcement will be the biggest tariff announcement of the presidency, meaning it poses significant risks to U.S. stocks and risk proxies, such as the NZD Dollar.

Given this, the scope for NZD strength is limited in the run-up to the announcement.

Looking at the calendars, it is a relatively subdued week in New Zealand, while the UK calendar should offer some two-way risks for GBP.

🇳🇿 New Zealand – Economic Events (Week of March 25–29, 2025)

Wednesday, March 26

📌 Monthly Trade Balance (February)

Previous (Jan): NZD -976 million

🔹 NZD Impact: This report has traditionally had limited currency implications.

Friday, March 28

📌 ANZ Business Outlook Survey (March)

Previous: Business Confidence: -52.0 | Own Activity Outlook: -4.0

🔹 NZD Impact: An improvement in business sentiment would suggest stabilising domestic conditions, potentially supporting NZD. Continued pessimism could raise recession risks, increasing RBNZ rate cut expectations and weighing on NZD.

British Pound Calendar

Picture by Kirsty O’Connor / HM Treasury.

Monday, March 24

📌 S&P Global Flash PMIs (Mar)

Sterling firms after S&P Global's services PMI rose to 53.2 in March, easily beating estimates for 51.2 and marking a notable uptick from February's 51.

Manufacturing is, nevertheless, in trouble, with the Manufacturing PMI slumping to 44.6 from 46.9.

However, because manufacturing now represents a small portion of the broader economy, the composite PMI, which gives a sector-adjust reading, read at 52. This is a marked increase on February's 50.5 and is the biggest rise in six months.

"An upturn in business activity in March brings some good news for the government ahead of the Chancellor’s Spring Statement," said Chris Williamson, Chief Business Economist at S&P Global Market Intelligence. "However, one good PMI doesn’t signal a recovery. The economy is eking out modest growth, with employment still falling and confidence close to two-year lows."

📌 BoE Governor Bailey Speech (18:00 GMT)

🔹 GBP Impact:

A hawkish tone (concern over inflation, rate cut caution) could lift GBP. A dovish tone may signal future easing, pressuring GBP.

Wednesday, March 26

📌 CPI (Feb)

Expected:

Monthly: +0.5%

Annual Headline CPI: 2.9%

Annual Core CPI: 3.6%

Previous:

Monthly: -0.1%

Annual Headline CPI: 3.0%

Annual Core CPI: 3.7%

🔹 GBP Impact:

A higher-than-expected print could delay BoE rate cuts, supporting GBP.

A cooler-than-expected CPI would reinforce disinflation and increase easing expectations, likely weighing on GBP.

📌 Chancellor Rachel Reeves Budget Update (12:30 GMT)

🔹 GBP Impact:

Fiscal stimulus or prudent budgeting could support GBP if seen as growth-positive or fiscally responsible. Loose spending without funding clarity might raise debt concerns, which are mildly bearish for GBP.

A repeat of the Liz Truss 'mini budget' currency collapse is highly unlikely.

Friday, March 28

📌 Final Q4 GDP (QoQ & YoY)

Expected (QoQ): +0.1%

Expected (YoY): +1.4%

Previous: +0.1% QoQ, +1.4% YoY

🔹 GBP Impact:

As a final print, market impact will be limited unless revised. A surprise upward revision could boost GBP modestly.

📌 Retail Sales (Feb)

Including Fuel:

Expected: -0.4% MoM (0.6% YoY)

Previous: +1.7% MoM (1.0% YoY)

Excluding Fuel:

Expected: -0.5% MoM (0.4% YoY)

Previous: +2.1% MoM (1.2% YoY)

🔹 GBP Impact:

A sharp drop in sales could signal weakening demand, negative for GBP. If data surprises positively, it may support GBP by reducing growth concerns.