A Bet on a Sterling Recovery: Nordea Reckon the GBP/EUR Exchange Rate Could go Higher

- Exchange Rates for Reference:

- 1 GBP converts into 1.1345 Euros on the inter-bank market

- 1 EUR converts into 0.8815 Pound Sterling

It's deadlock between the Euro and Pound at present with markets unable to push the GBP/EUR exchange rate out of the 1.13-1.14 band.

Part of the reason lies with the fact that both the European Central Bank and Bank of England are threatening higher interest rates in the not-to-distant future.

When central banks adopt this kind of tone their respective currencies tend to rise. The latest salvo fired in this battle comes from the ECB whose latest communication regarding policy suggests they are on course to turn their monetary stimulus taps off in the near-future.

But what happens to a currency pair when both sides of the equation adopt this kind of tone is a stalemate, as we are seeing in GBP/EUR.

This presents us with an intriguing scenario - which central bank will blink first - the BoE or the ECB? This is an important question, because whoever rows back from their pro-hike rhetoric first will likely see their currency fall.

Whoever acts first will likely see theirs rise.

Nordea Bank AB - the Nordic financial services group - reckon that the Bank of England has more reason to go for an interest rate rise than their European counterparts and this makes the Pound a potential buy.

Analysts at Nordea’s Markets division have looked at the UK’s inflation level - and the Bank of England’s record-low interest rates - and reckon something has to give.

A situation in which the Bank keeps rates at 0.25% while inflation creeps towards 3% is untenable and those warnings from Mark Carney and other policy-makers that rates might rise in 2017 actually have some credibility.

Central banks seek to quell inflation by raising interest rates; the idea is that this cools spending. A byproduct of higher interest rates is a stronger currency.

Hence, all this sounds quite good for those hoping for a stronger Pound.

But, Nordea Markets reckon the Pound is still not as high as where it should be in a situation where markets see a 50/50 chance of an interest rate rise happening in 2017.

“The GBP hasn’t adjusted to the new more hawkish outlook yet,” says Andreas Steno Larsen at Nordea Markets in Stockholm. “Is it time for a bet on a rate hike?”

His answer is yes - and the way this is done is by buying Sterling.

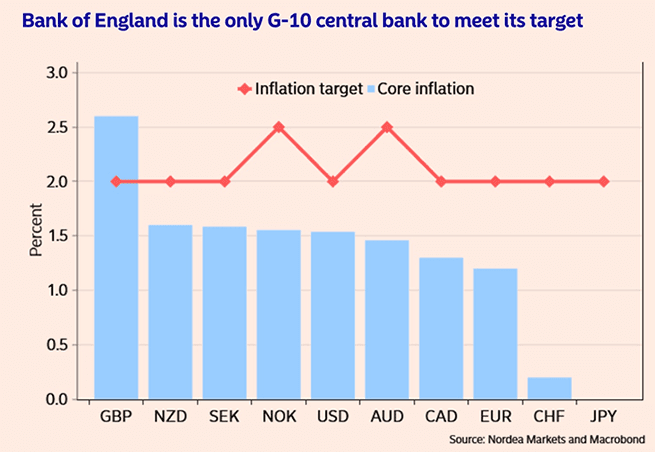

UK Inflation Ahead of the Pack

What the ECB’s Forum on Central Banking held in late June in Sintra, Portugal taught us is that western central banks are now looking to push interest rates higher as economic growth improves.

A signal of improved growth is higher inflation - as rising wages prompt higher spending and higher prices.

Of course, if prices rise too fast it can be destabilising, and that is why the majority of banks tend to target inflation at 2%.

This magical number remains out of reach for many central banks, leading some to believe higher interest rates are still some way off.

If we look at the following picture though, there is one country that stands out:

The UK’s inflation rate is well above the Bank of England’s target.

“Looking at the inflation outlook, there actually could be a decent case for a hike baking,” says Larsen. “Assuming that the trade weighted GBP stays at current levels throughout 2018 and 2019 – core inflation could, judged by historical patterns, be on the path of breaching the 3% mark as well.”

Very good to see #MPC members talking of higher interest rates but the process should have started years ago https://t.co/MVwYgnXrKC

— Andrew Sentance (@asentance) July 5, 2017

“Assuming that the trade weighted GBP stays at current levels throughout 2018 and 2019 – core inflation could, judged by historical patterns, be on the path of breaching the 3% mark as well,” says the analyst.

Of course there is a hesitancy at the Bank to raise rates in light of the recent slowdown in economic activity and ongoing concerns about Brexit.

But, “the good news for Bank of England is that if US data rebounds – so does UK data – at least if history is any guide,” says Larson.

The US economy is emerging from the soft start to the year with most surveys suggesting the second-quarter will be improved.

Thus far, second-quarter surveys in the UK confirm this trend has indeed crossed the Atlantic, perhaps opening the door to an interest rate a little further.

“Why not be short-term long the currency, where the central bank is actually already at target? Then Sterling is your answer,” says Larsen.

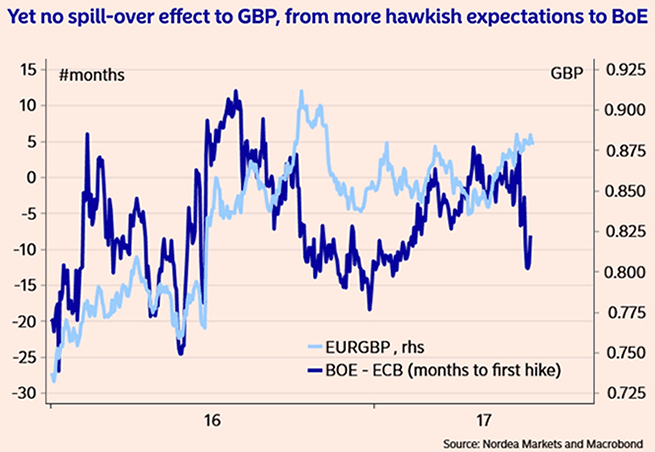

The Euro Must Fall Against the Pound (if Markets are Fair)

Another interesting graph explains why the Euro might be at risk of a fall against the Pound:

What the above is telling us is that markets are suddenly betting the Bank of England is much closer to raising interest rates than is the ECB.

But, the Euro-Pound exchange rate has not caught up with this reality.

Nordea Markets reckon this anomaly must be erased via a fall in Euro-Sterling.

Indeed, on this basis EUR/GBP should be around 0.81 which is 1.2446 in Pound to Euro terms.

But, with Brexit on the horizon there remains some trepidation amongst foreign exchange analysts to bid the Pound higher against the Euro.

No one knows what Brexit negotiations will deliver, nor do they have any confidence in the strength of the present May administration.

As such, the Pound will suffer a premium demanded by investors which will likely keep EUR/GBP above the fair-value levels implied by the above graph.

But, that is not to say some movement lower cannot still happen.

“Is it time to bet on a rate hike via long Sterling? We think it is. With only 25% probability attached to a hike in August, the bet seems kind of cheap,” says Larsen.

4% Upside

Yield differentials, which represent interest rate expectations, and are a major driver of exchange rates have already moved in anticipation of a rate hike, suggesting that it there is one, Sterling’s appreciation will be muted.

“Currently, and after the sell-off of recent days, the 5Y Gilt is trading at 0.72%, or 47bp higher than the BoE base rate (and 2Y yields have also risen sharply). Therefore, the market seems already to have discounted a rate hike,” says Unicredit Bank’s Katherin Goretzki.

Analysts at UniCredit believe raising interest rates at the Bank of England would represent a policy mistake.

Nevertheless, there would be some reaction by the Pound, and Unicredit calculate that expectations of a hike would probably lead to a fall of 4.0% in EUR/GBP:

“Even if we allow for German yields to remain unchanged and inflation differentials to remain flat, this would imply a modest drop in the model’s “short-term fair value” to close to 0.84. Still, this corresponds to a drop of roughly 4% from current trading levels, a meaningful depreciation in EUR/GBP,” said Goretzki.

EUR/GBP at 0.84 gives a Pound to Euro exchange rate of 1.1905.