Dollar-Yen: 143 in Sight Shows XS.com Forecast

- Written by: Rania Gule, Market Analyst at XS.com.

Image © Adobe Images

"I believe that the narrowing of the yield spreads between U.S. Treasury yields and Japanese government bond yields is likely to reinforce the bearish trend for the USD/JPY pair."

Dollar-Yen (USD/JPY) experienced a sharp decline yesterday, starting today, Thursday, at 143.87, after falling below 144.00 for the first time since last week, reaching 143.77 with a loss exceeding 1%.

In my view, this drop is a result of several pressures, notably disappointing U.S. job data for July (JOLTS), which has heightened expectations for a potential interest rate cut by the Federal Reserve at its upcoming meeting.

The pair declined following the release of U.S. data, and momentum turned bearish. The Relative Strength Index (RSI) also remained bearish, with its slope shifting from upward to downward, signalling a short-term trend reversal.

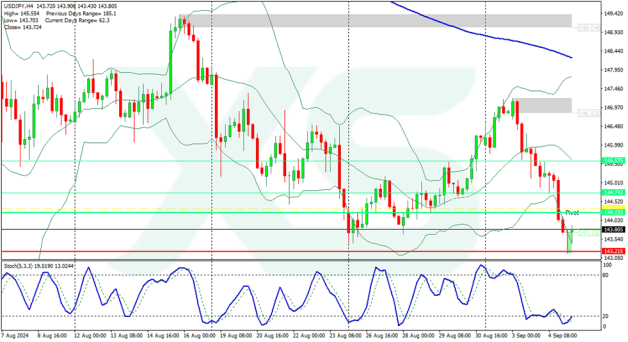

The first support for the USD/JPY pair is the daily low of 143.45 on August 26. A break below this level would target key psychological support levels, such as 143.00, followed by 142.50 and 142.00. Once breached, the major support would be the low of August 5 at 141.69. For the bulls to regain control, they would need to reclaim the peak at 148.45 before targeting the 150.00 level in the medium term.

Image: XS.com

The four-hour chart indicates a move in a downward wave that reached support at 143.18. A corrective move to 145.66 could occur, testing it from below. Further declines might follow, down to 141.80 and then to 137.77. The MACD indicator supports these bearish expectations, with the signal line above zero but trending sharply downward.

On the hourly chart, the USD/JPY pair dropped sharply from the 145.66 level and has since consolidated around 143.60 – 143.11. A retest of 145.66 in an upward correction could be expected before resuming the downtrend. This bearish scenario aligns with stochastic oscillator readings, where the signal line is slightly above 50 but indicates a downward movement in the near term.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Dollar-Yen's decline comes as U.S. 10-year Treasury yields were negatively affected by reduced rate cut expectations, falling to 3.757% with losses nearing 2%. This sharp decline in yields directly impacts the USD/JPY pair, as the close relationship between yield movements and this currency pair's performance is evident.

Any drop in bond yields leads to a weakening of the dollar against the yen. With markets returning from the U.S. Labor Day holiday, risky assets were most affected due to the cautious sentiment that prevailed.

Thus, we observed a boost in risk aversion in the foreign exchange market. Safe-haven currencies, such as the Japanese yen, Swiss franc, and U.S. dollar, gained momentum, while risk-sensitive currencies like the Australian and New Zealand dollars and the Norwegian krone fell.

Increasing concerns about global growth and upcoming economic data are driving investors towards safe havens, raising the likelihood of continued pressure on the USD/JPY in the near term.

From my perspective, fears about global economic growth are rising, which we expect will extend negative performance trends in the currency and stock markets within the G10, at least until the Federal Open Market Committee meeting on September 18.

The weak manufacturing report from the Institute for Supply Management added to the instability, leading to a downward wave in U.S. stock markets, with technology stocks leading the decline.

In Japan, the Bank of Japan remains committed to its accommodative monetary policy but has hinted at potential adjustments if economic forecasts align with actual data. There is also talk of a possible rate hike in December, reflecting the bank's cautious stance amid global economic developments.

Additionally, the slight improvement in Japanese data, such as the rise in the manufacturing PMI to 49.8 from 49.5, suggests potential stability in the manufacturing sector. This development could impact USD/JPY forecasts as the market re-prices the effects of monetary policy and economic growth in Japan.

Based on these factors, I believe that the narrowing of the yield spreads between U.S. Treasury yields and Japanese government bond yields is likely to reinforce the bearish trend for the USD/JPY pair.

With the continued risk aversion affecting stock markets and other assets, the pressure on the dollar seems set to persist, boosting the strength of the Japanese yen in the near term.

Ultimately, future developments will remain closely tied to Federal Reserve and Bank of Japan policies, which will significantly influence the potential movements of this pair soon, especially with the release of U.S. employment data and any data that could surprise the markets before the Fed’s next meeting.