Pound to Dollar Rate Weekly Outlook: Staying Pressured

- Written by: Gary Howes

Image © Giuseppe Milo, CC BY 2.0. Source.

Pound Sterling tried to extend Friday's rebound against the U.S. Dollar, but the rally looks to have failed, confirming difficult conditions into year-end.

The Pound to Dollar (GBP/USD) exchange rate fell to a new multi-month low last week before picking itself up and rebounding into the final holiday-interrupted sessions of the year.

That rebound extended into Monday before ultimately failing.

"The GBP’s short-term downtrend remains intact, putting key, short-term support at 1.2485/90 at risk in the short run. GBP gains late last week stalled above 1.26 as strong selling pressure continued to greet minor GBP rallies. A break under support in the upper 1.24s targets a drop to 1.23," says Shaun Osborne, an analyst at Scotiabank.

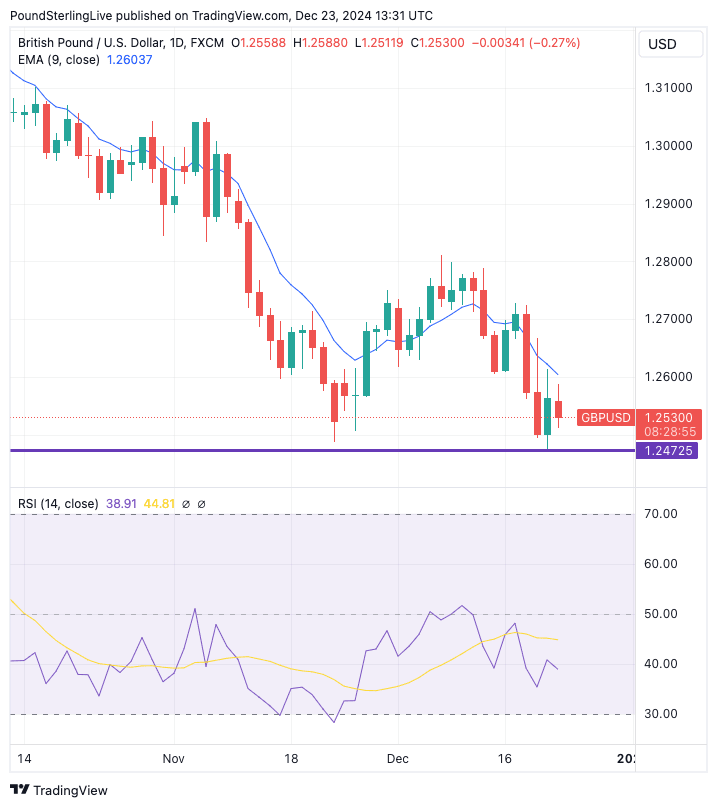

Last week's low at 1.2472 will be the interim support zone that sellers will target. It could potentially see us through the Christmas period, a time that will be characterised by think liquidity conditions.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Although there is little on the calendar to bother markets, thin conditions can often see some outsized moves, which could provide those still watching the market with some excitement.

The general rule, however, is that such moves will ultimately fade, and we do not anticipate any new directional trends emerging in the coming days.

GBP stays heavy with UK economic data released Monday by the ONS showing the UK economy flatlined in the third quarter (0% q/q growth), marking a disappointing start to Keir Starmer's term as Prime Minister.

Above: GBP/USD at daily intervals, showing the nine-day EMA (blue line) and the 1.2472 interim low.

The ONS said Q2 growth stood at 0.4%, giving us a picture of an economy that has seen the brakes slammed by the new leaders on Whitehall.

It is little wonder, then, that the Bank of England last week expressed concerns about the economy's trajectory, raising the possibility that it will cut interest rates by more than the market currently expects.

The market went into last week's policy decision expecting two more 25 basis point cuts in 2025 but exited the week expecting between three and four.

🎯 GBP/USD year-ahead forecast: Consensus targets from our survey of over 30 investment bank projections. Request your copy.

The readjustment came after three of the nine members of the Monetary Policy Committee voted to cut rates immediately. Furthermore, the Bank lowered economic growth projections and sounded more cautious about the outlook.

It looks as though the Bank intends to maintain a quarterly pace to its rate-cutting cycle, forcing a readjustment in market expectations that was reflected in a weaker Pound.

2024's best-performing currency remains the U.S. Dollar, and the trend for GBP/USD is lower. Given this, the playbook is for any GBP/USD rebounds to prove short-lived ahead of a fresh impetus lower.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

A retest of 1.2472 should play out in the near-term, with a break to 1.23 then forming in the new year.

Early 2025 could see weakness resume as further U.S. economic outperformance is confirmed. "The setup for markets into 2025 is good for a continuation of trends. The U.S. election and the pivot to a stronger USD received support from the FOMC reducing expectations for rate cuts in 2025," says Bob Savage, Head of Markets Strategy and Insights at Bank of New York (BNY).

It's not all quiet this week as we have U.S. durable goods, Manufacturing ISM and jobless claims releases to digest.

"The risk of Q4 upside growth surprises dominates," says Savage.