GBP/USD Higher as US Growth Splutters BUT Resistance Lies Ahead

The outlook for the pound v dollar exchange rate has improved considerably with the pair rallying higher from the lows set at 1.4560 in early April.

"It seems like nothing could keep sterling down as it powered higher for the sixth consecutive trading day despite weak UK GDP numbers," says Kathy Lien at BK Asset Management summing up the currency market's current stance on the sterling dollar rate.

While recent GDP data took some of the shine off the UK pound, forecasts suggest it would be premature to call the end of the GBP-USD rally.

The UK's disappointing GDP data was overshadowed by the mid-week GDP reading out of the United States where it was shown that the US economy is indeed slowing down.

The steady climb higher from the April lows has reinforced further positivity with technical momentum signals convincing further speculative buying interests.

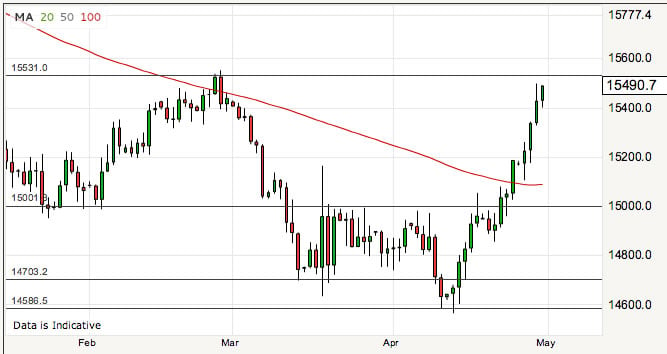

Technically, the improvement in fortunes for the British pound’s outlook against the Greenback is represented in the following graphic:

Further buying interest would no doubt have been sparked when the important threshold that is the 100 day moving average was crossed.

This is represented by the red line above. The crossover is seen by many technical players as confirmation that momentum has turned. Those that backed the rally at this point will be sitting pretty.

Note though that the February resistance at 1.5530 now looms large - many in the market will be setting up their exits at this level; such positioning may well take some wind out of GBPUSD's sails.

A break above here would however attract further buying interest and the rally could extend yet further.

“GBP/USD has traded through the 2014-2015 downtrend and now eroded the double Fibonacci retracement at 1.5175/86. We have a confirmed buy signal on the DMI, and we suspect dips lower will remain shallow,” says Karen Jones at Commerzbank confirming the GBP remains favoured.

Beware. All currency quotes mentioned above refer to the wholesale market. Your bank will affix a discretionary spread when transferring money internationally. However, an independent provider will seek to undercut your bank's offer, thereby delivering up to 5% more currency in some instances. Please learn more.

USD Sinks on Growth Data

US GDP figures showed the world's largest economy scraped by with growth of 0.2% in the first quarter of 2015.

The data was a disappointment to those who had been expecting growth of 1% to be regiesterd.

Markets are now seeling the USD as they bet that the US Federal Reserve will have to delay their first interest rate hike.

It was expectations for an interest rate rise in summer of 2015 that fuelled much of the impressive USD rally over the past year.

The Fed meets from the 28th to 29th of April to arrive at their latest decision on monetary policy settings.

No major change is expected, but markets will likely play on the safe side when it comes to the USD ahead of the results being announced on the 29th.

GBP Sterngth Could be Temporary

While the technical outlook remains supportive of further gains for the GBP-USD we should be aware that the fundamental economic backing for the move ultimately remains questionable.

Watch out for turbulence to potentially hit sterling in the run-up and through the UK General Elections to be held on the 7th of May.

GBP-USD remains vulnerable to political risk and the pair may find resistance at current prices until the election picture begins to clear up.

US Economy to Start Strengthening in the Third Quarter of 2015

A recent run of poor economic figures, combined with over-bought conditions on the USD family, have conspired against the Greenback as of late.

Latest news on the economy’s service sector does however confirm the worst may be over, and this is an important observation for those waiting on a higher pound dollar exchange rate.

The Markit US Composite PMI, which weights together the output indices from the manufacturing and services surveys, hit a seven-month high of 59.2 in March and remained elevated at 57.4 in April.

However, this translates into a ‘mere’ 1pct uptick in GDP growth. This slowdown, cited as being due to the harsh winter is being cited by many analysts as the reason the US dollar’s rally has stalled.

However, be aware that further USD strength may well be on the cards.

“The surveys are pointing to growth accelerating to around 3% in the second quarter,” says Chris Williamson at Markit.

As such we would view the current dip in the USD as a temporary pause ahead of a return-to-strength.