GBP/USD Week Ahead Forecast: Stifled and Risking Deeper Setback

- Written by: James Skinner

- GBP/USD rebound stifled from home & abroad

- As data stokes U.S. bond yields, USD rebound

- BoE's rate policy & economic outlook stifle GBP

- U.S. inflation data & Fed policy outlook in focus

- Supports near 1.2044, 1.2012, 1.2003, 1.1977

Image © Adobe Images

The Pound to Dollar exchange rate drew a bid from the market when falling near to the 1.20 handle ahead of the weekend but could slip back toward or even below that level later this week if July’s U.S. inflation figures offer a further incitement to the still-hawkish Federal Reserve (Fed).

Sterling had made it almost as far as the 1.23 level against a retreating Dollar early last week before being turned lower by a volley of U.S. economic data that argued strongly against the recently popular idea of a recession being underway in the world’s largest economy.

“The persistent huge appetite for workers is stoking large wage gains, providing households with bigger paychecks that will support spending for the foreseeable future,” says Bob Schwartz, a senior economist at Oxford Economics.

“Prior to the jobs report, market sentiment had increasingly pivoted to the belief the Fed would lower its rate-hiking sights at the next policy meeting. That narrative has lost credibility, as the robust jobs report and sturdy wage gains stiffened the inflationary tailwinds,” Schwartz also said on Friday.

Above: Pound to Dollar rate shown at 2-hour intervals. Click image for closer inspection.

Above: Pound to Dollar rate shown at 2-hour intervals. Click image for closer inspection.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Bond yields and the Dollar were lifted after Institute for Supply Management PMI surveys of the manufacturing and services sectors rose for July in contradiction of their gloomier S&P Global counterparts before the July non-farm payrolls report out on Friday made an open mockery of the notion of a faltering economy.

Meanwhile, and along the way, Fed policymakers appeared to repeatedly warn financial markets away from their recent assumption that U.S. interest rates could be cut as soon as the second quarter next year from highs that are expected to be reached in the final quarter of this year.

“Over the last couple weeks, it has been clear that the FOMC would like to slow the pace of rate hikes. What is much less clear is whether the data will finally give them a chance to do that,” writes Michael Cahill, a G10 FX strategist at Goldman Sachs, in a Friday research briefing.

“Recently, the data the FOMC has highlighted as important inputs to its decision to slow have continued to show signs of an overheated labor market and strong wage pressures. Next week’s inflation report seems very unlikely to offer “compelling evidence” of a slowdown,” Cahill added.

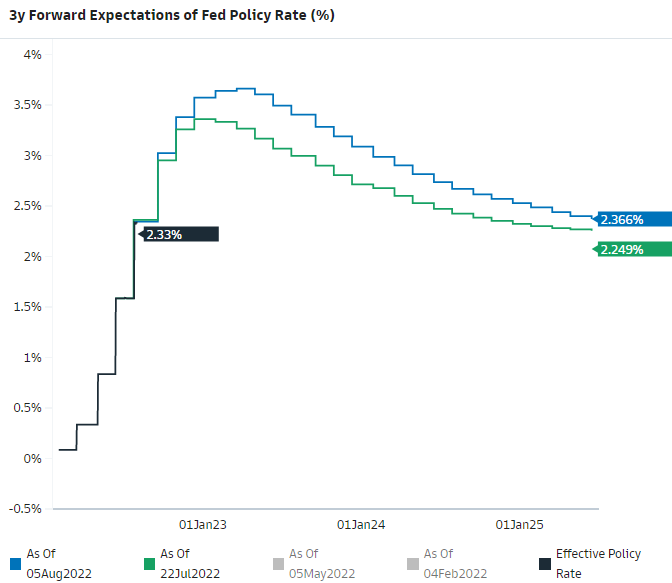

Above: Market implied expectations for midpoint of the Fed Funds interest rate on August 05 and July 22. Source: Goldman Sachs Marquee. Click image for closer inspection.

Above: Market implied expectations for midpoint of the Fed Funds interest rate on August 05 and July 22. Source: Goldman Sachs Marquee. Click image for closer inspection.

Last week’s data and policy chatter lifted expectations for the Fed’s interest rate in September and beyond while reviving a previously-stalled rally in U.S. bond yields and calling a halt to the Dollar’s recent corrective fall.

The Pound-Dollar rate did draw a bid from the market when trading down to 1.2003 in the wake of Friday’s payrolls report, however, although whether it can hold above that level this week likely depends on Wednesday’s U.S. inflation figures and market appetite for Sterling in the interim.

"Monitoring the relationship between GBP/USD fundamentals and spot, the short-term fair value model calculates a -0.37% undervaluation of spot, signalling spot is being driven more closely by fundamentals," says Lee Hardman, a currency analyst at MUFG.

"Fed officials have in recent days encouraged market participants to price in a higher terminal rate," Hardman and colleagues said on Friday.

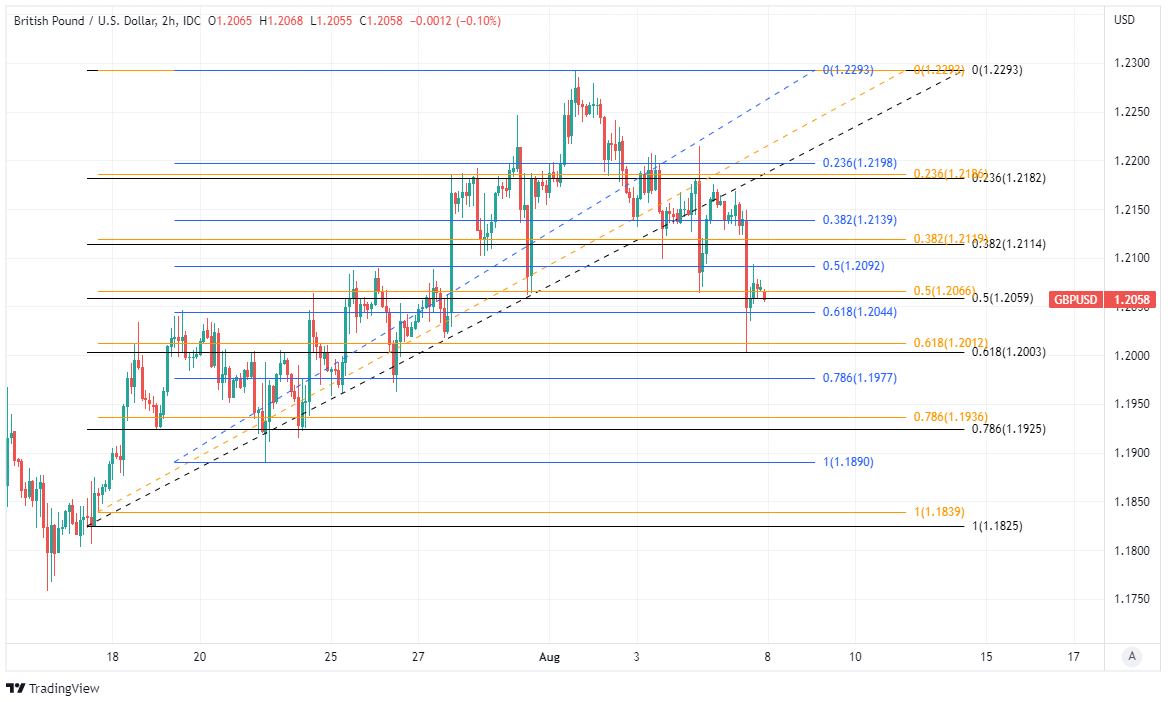

Above: Pound to Dollar rate shown at 2-hour intervals with Fibonacci retracements of various recent rebounds indicating possible areas of short-term technical support. Click image for closer inspection.

Above: Pound to Dollar rate shown at 2-hour intervals with Fibonacci retracements of various recent rebounds indicating possible areas of short-term technical support. Click image for closer inspection.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

“We had been hoping that the Fed would be able comfortably to pivot to 50bp in September or even 25bp, but the latter is now off the table,” says Ian Shepherdson, chief economist at Pantheon Macroeconomics.

“The policy decision will be 50bp or 75bp. We still hope for the former, but the data over the next seven weeks will need to be more or less uniformly on the soft side for that to happen,” Shepherdson said following Friday’s release.

Friday’s payrolls report had U.S. wage growth picking up further in July and if combined with an additional increase in U.S. inflation this Wednesday the two could easily become viewed at the Fed in the same way as a red rag waved before a raging bull might be.

“For the July CPI report we expect the headline CPI to post a modest advance of 0.1% as energy prices likely fell last month while the core rate could have posted another firm increase of 0.5% after a 0.7% jump in June,” says Kevin Cummins, chief U.S. economist at Natwest Markets.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of various recent extensions of 2021 downtrend indicating possible areas of short-term technical resistance. Click image for closer inspection.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of various recent extensions of 2021 downtrend indicating possible areas of short-term technical resistance. Click image for closer inspection.

“On a year/year basis, a realization of our forecast would push down the headline rate from a 40-year high of 9.1% in June to 8.6% in July. In contrast, after dipping slightly in June (due to base effects) to 5.9% (after 6.0% in May), the core inflation rate is likely to rise to 6.1%,” Cummins added.

The danger is now that another inflation acceleration compounds to force financial markets into pricing-in a more aggressive interest rate response from the Fed through the remainder of the year, which would risk sending the Pound-Dollar rate back below the 1.20 handle later this week.

This is very much the outlook of Karen Jones and colleagues at the Society of Technical Analysts, who say Sterling's inability to recover above the 55-day moving-average (pink line in the above chart) is one of several indicators warning of a potential fresh turn lower.

Readers can hear more from Jones and the STA in the below video.

Source: Society of Technical Analysts, Youtube.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Sterling itself was sold widely last week when the Bank of England (BoE) lifted Bank Rate for a sixth time, taking it up to 1.75%, but warned of an imminent recession that that it expects will run as deep and last for even longer than the recessions seen in both the early 1990s and the early 1980s.

It remains to be seen how it will trade over the coming days, although the week ahead calendar is devoid of major appointments for the Pound in advance of Friday’s GDP data for June and the second quarter, both of which are expected to reveal economic contractions.

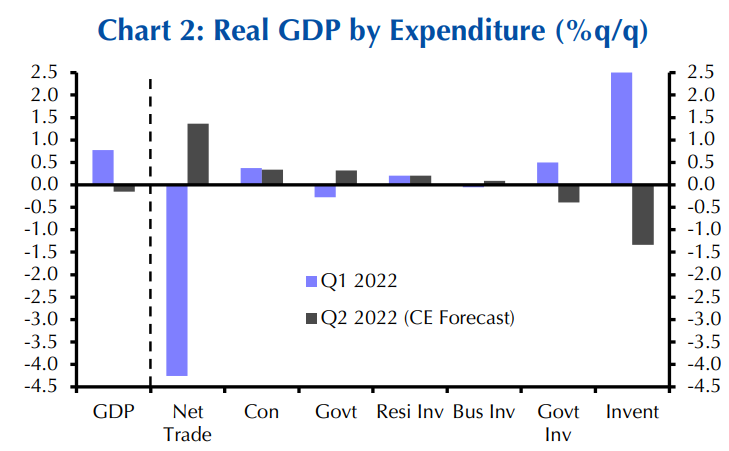

“We estimate that the extra Jubilee bank holiday in June was the main reason why GDP fell by 1.3% m/m in June and by 0.2% q/q in Q2. GDP will rebound in July, but a recession is still on the way,” says Ruth Gregory, a senior UK economist at Capital Economics.

“Within our estimate of a 0.2% q/q fall in GDP in Q2, inventories and government investment fell while consumer spending held up well, rising by 0.3% q/q versus the 0.4% q/q gain in Q1. But with high inflation reducing real incomes, consumer spending will be at the epicentre of the recession,” Gregory and colleagues wrote in a Friday research briefing.

Source: Capital Economics.

Source: Capital Economics.