GBP/NZD Rate Rally Stalled and at Risk of Reversal

- Written by: James Skinner

- GBP/NZD’s April rebound stalled at 1.94

- Steadier NZD/USD weighs on GBP/NZD

- Recovery may push GBP/NZD sub-1.90

Image © Adobe Stock

The Pound to New Zealand Dollar exchange rate’s April rally has partially unwound thus far in the new week and could reverse further if the influential NZD/USD pair continues to find its feet over the coming days.

New Zealand’s Dollar was one of the better performing major currencies on Tuesday after the NZD/USD exchange rate appeared to stabilise around the 0.66 level while Sterling notched up further declines against almost all counterparts in the G20 basket of currencies.

The Kiwi had fallen further on Monday, building on last week’s Dollar and Renminbi-induced losses just as the Chinese currency reached its lowest level against the greenback since November 2020, although both were steadier on their feet by Tuesday.

“NZ-US interest rate differentials have narrowed and could further weigh on NZD/USD in the near term,” says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

“GBP/USD has slumped by three US cents since UK retail sales sank by 1.1%/mth in March and the UK PMI eased by more than expected (though remains strong),” Capurso also said in a Tuesday research briefing.

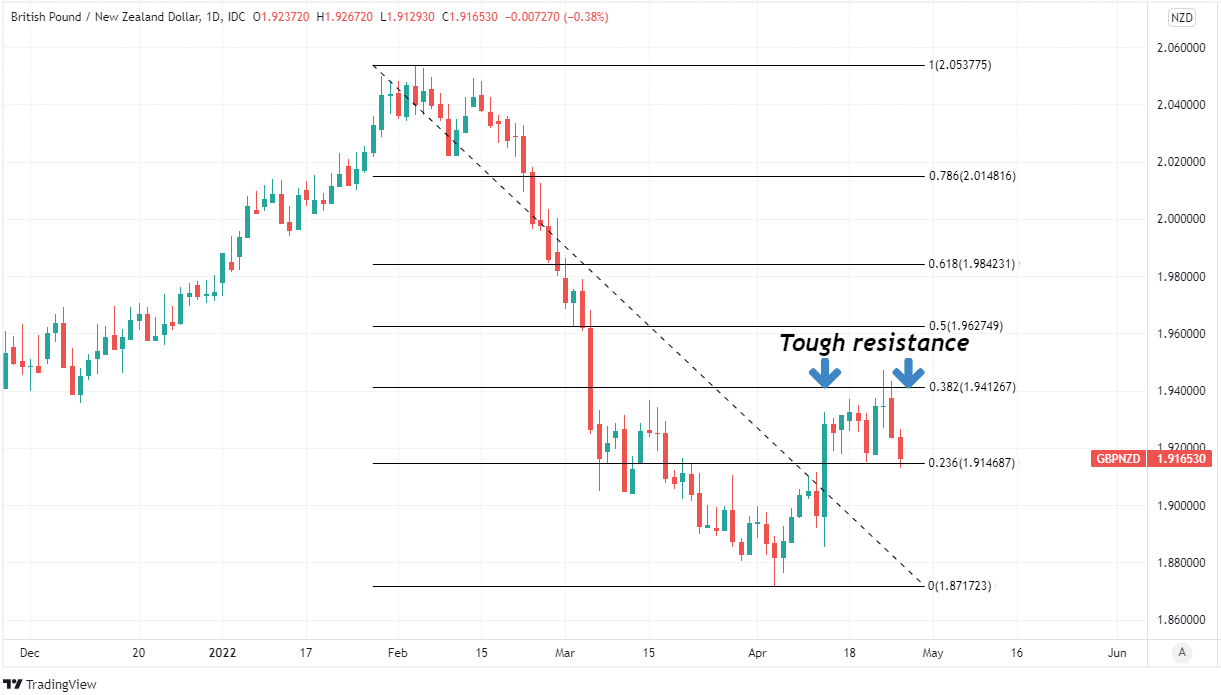

Above: Pound to New Zealand Dollar rate shown at daily intervals with Fibonacci retracements of late February decline indicating likely areas of short-term technical resistance to any further recovery by Sterling. Click image for closer inspection.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

Sterling has, meanwhile, continued an underperformance that escalated last Friday when official data revealed that UK retail sales fell far further in March than was expected by economists in an indication that rising energy and food costs may now be cannibalising other parts of the economy.

But GBP/NZD is also highly sensitive to price action in NZD/USD - as it tends to closely reflect the relative performance of GBP/USD and NZD/USD - and would be likely to remain under pressure this week if the latter remains above the 0.66 handle it managed to hold onto on Monday. (Set your FX rate alert here).

“The multi-week decline remains in progress, with potential to reach 0.6530 during the week ahead. The USD is likely to remain strong into the 4 May FOMC, and yield spreads (for longer maturities) are likely to be a headwind for the NZD near term,” says Imre Speizer, head of NZ strategy at Westpac.

Much like in the UK, New Zealand’s economic calendar is devoid of major appointments for the Kiwi this week and that potentially leaves both currencies more susceptible to the ebb and flow of market appetite for the U.S. Dollar

“A lot depends on oil and food prices, which are held hostage by the war in Ukraine, as well as spreading Covid lockdowns in China, which may prolong supply-chain shortages,” says Bob Schwarz, a economist at Oxford Economics.

“Core consumer prices are already moderating but a sharp drop in used car prices heavily influenced the slowdown in March,” Schwarz adds.

Widespread strength in the U.S. Dollar has weighed heavily on the Kiwi and Sterling in recent months but all currencies will be sensitive to the implications of this Friday’s release of the core PCE price index inflation figure in the U.S.

Friday’s data will provide an indication of whether or not March marked a turning point for the U.S. inflation trend after last month’s figures revealed an easing in the strength of month-on-month price increases that was echoed in the core measure of the official consumer price index for March.

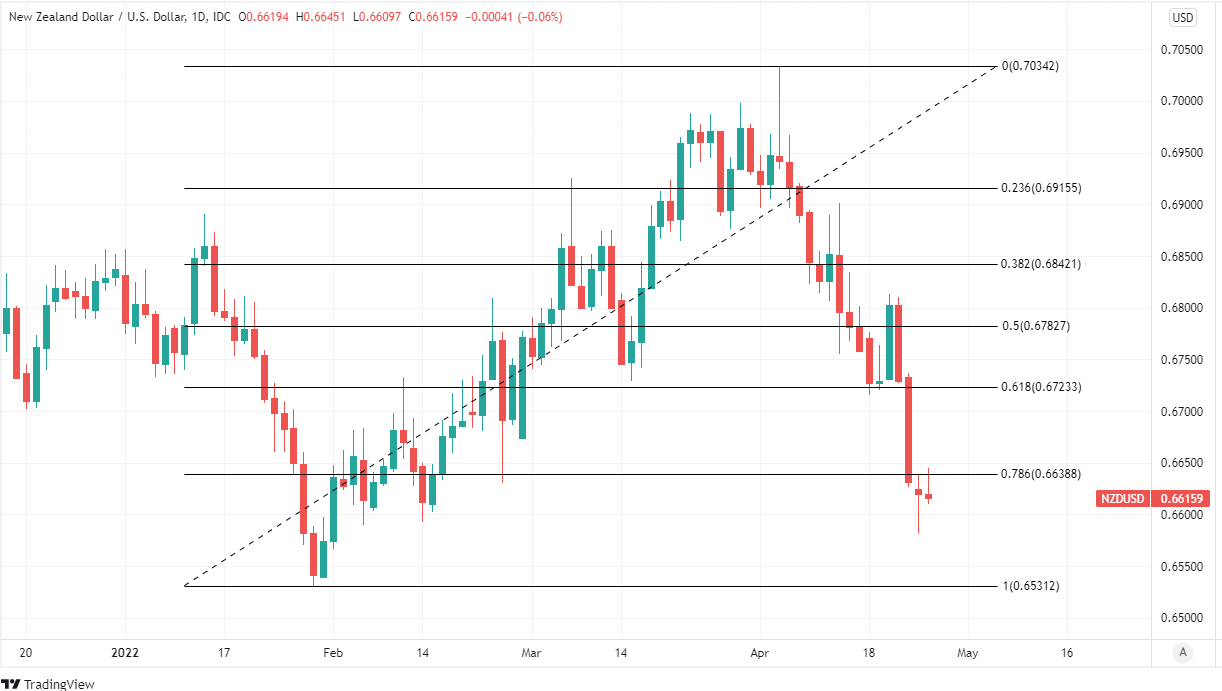

Above: NZD/USD shown at daily intervals with Fibonacci retracements of the February rally indicating possible areas of short-term technical support for the New Zealand Dollar. Click image for closer inspection.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

To the extent that April’s PCE data further echoes the March message it would indicate that the Federal Reserve monetary policy stance has already become as ‘hawkish’ as it’s likely to, and so would potentially take some wind from the sails of the U.S. Dollar

This in turn would be supportive of other currencies including the New Zealand Dollar, which has itself benefited in recent months from a ‘hawkish’ Reserve Bank of New Zealand (RBNZ) monetary policy and may also be close to seeing the peak of Kiwi inflation pressures.

“Q1 saw the Omicron wave peak in New Zealand, as well as massive commodity price volatility due to the war in Ukraine. Touch wood, that means inflation prints will start to ease from here (albeit remaining uncomfortably high for some time),” says Sharon Zollner, chief economist at ANZ.

“We’re not out of the inflation woods yet – and without ongoing monetary tightening (including we think a 50bp OCR hike in May) we would likely see domestic inflation pressures continue to spiral in the wrong direction,” Zollner also cautioned in a research briefing last week.