EUR/USD Week Ahead Forecast: ECB Guidance Key to Extended Recovery

- Written by: James Skinner

- EUR/USD facing resistance near 1.0786 in short-term

- ECB guidance on July & Sept decisions key to outlook

- Elevated expectations set high bar for EUR/USD gains

- U.S. inflation also key amid signs of EU-U.S. inflection

© European Central Bank, reproduced under CC licensing

The Euro to Dollar exchange rate has continued an attempted climb from near five year lows but may need the European Central Bank (ECB) to outhawk an already hawkish market on Thursday in order to sustain its recovery momentum ahead of the latest U.S. inflation data.

Europe’s single currency held above the recently recovered 1.07 handle against the Dollar throughout much of the week to Monday after having been aided substantially by a hawkish market repricing of the outlook for European Central Bank interest rates ahead of the June policy decision.

Thursday’s policy decision and subsequent press conference are widely expected to herald an announced end to the ECB’s last remaining and longest running quantitative easing programme while offering insights into the probable future path of interest rates.

But the currency market will be most interested in anything revealed about the ECB’s likely policy actions in July and September and specifically, any indications of the increment by which Eurozone interest rates could rise in July.

“EUR/USD can lift this week because of a hawkish European Central Bank (ECB) on Thursday and a weaker USD. Upside resistance at 1.0791 is very likely to be tested,” says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of February decline and various extensions thereof indicating likely technical resistances to any further recovery. Click image for closer inspection.

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of February decline and various extensions thereof indicating likely technical resistances to any further recovery. Click image for closer inspection.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

“The post–meeting communication from Thursday’s will be important to monitor for hints of a more aggressive tightening cycle. There is a small chance the ECB hikes this week,” Capurso and colleagues said on Monday.

The single currency will also likely listen closely for clues about the likely pace and size of additional steps thereafter given that a recent shift in pricing has left some markets implying that investors and traders expect the ECB’s deposit rate to rise by 0.35% next month and by a total of 1.25% this year.

That would take the deposit rate well above zero, bringing an end to the lengthy era of negative interest rates that has seen commercial banks charged for depositing money at the safe-haven that is the ECB and potentially marking a turning point for the Euro to Dollar rate outlook.

All of this follows a publicly aired debate among Governing Council members over whether to lift the benchmark in a typical 0.25% increment or by a larger 0.50% in July, and after an anticipated end to the ECB’s last remaining quantitative easing programme this week.

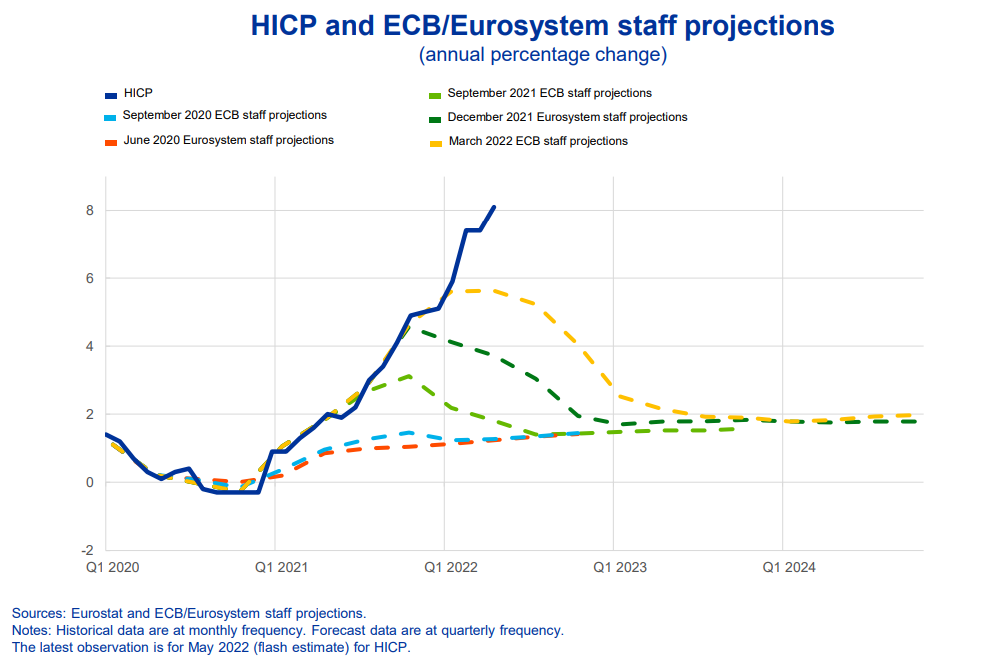

“HICP inflation is now 3% higher than prior to the last forecast update. As a consequence, this may result in Lagarde not completely ruling out a more aggressive response than graduated 25bps moves,” says Jeremy Stretch, head of FX strategy at CIBC Capital Markets.

Above: Eurozone inflation path relative to ECB’s various forecasts. Source: ECB.

Above: Eurozone inflation path relative to ECB’s various forecasts. Source: ECB.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

“Any such realization should help to continue to underpin the EUR,” CIBC’s Stretch also said on Friday.

Thursday’s decision comes after Eurostat figures revealed last week that Europe’s inflation rate leaping to a new record of 8.1% in May, which significantly erodes the gap between levels of annual price growth in the Eurozone and those in the U.S. where annual inflation was last 8.3%.

This could indicate that an inflection point is approaching for not only relative Transatlantic balance of inflation pressures but also potentially the relative stance of interest rate policy in Europe and the U.S. too, which could have knock-on implications for the Euro to Dollar rate outlook.

Much about Euro-Dollar price action in the weeks ahead will depend in large part on the extent to which the ECB signals agreement with recently escalating market expectations for its interest rate, or if it leans against them on Thursday.

"Indeed, with Chief Economist Philip Lane having explicitly pre-committed last week to a 25bp rate hike in July and another one in September, a hawkish surprise this week would likely require the open discussion of a 50bp hike by President Christine Lagarde. Even in such a scenario, the market’s pricing for 118bp of tightening by year-end means that the room for the EUR to benefit from this is somewhat contained,” warns Chris Turner, global head of markets and regional head of research for UK & CEE at ING.

"In our view, a reiteration of the recent pre-committed policy path looks more likely, and EUR/USD may slip back to the 1.0600 mark over the coming days," Turner and colleagues also said on Monday.

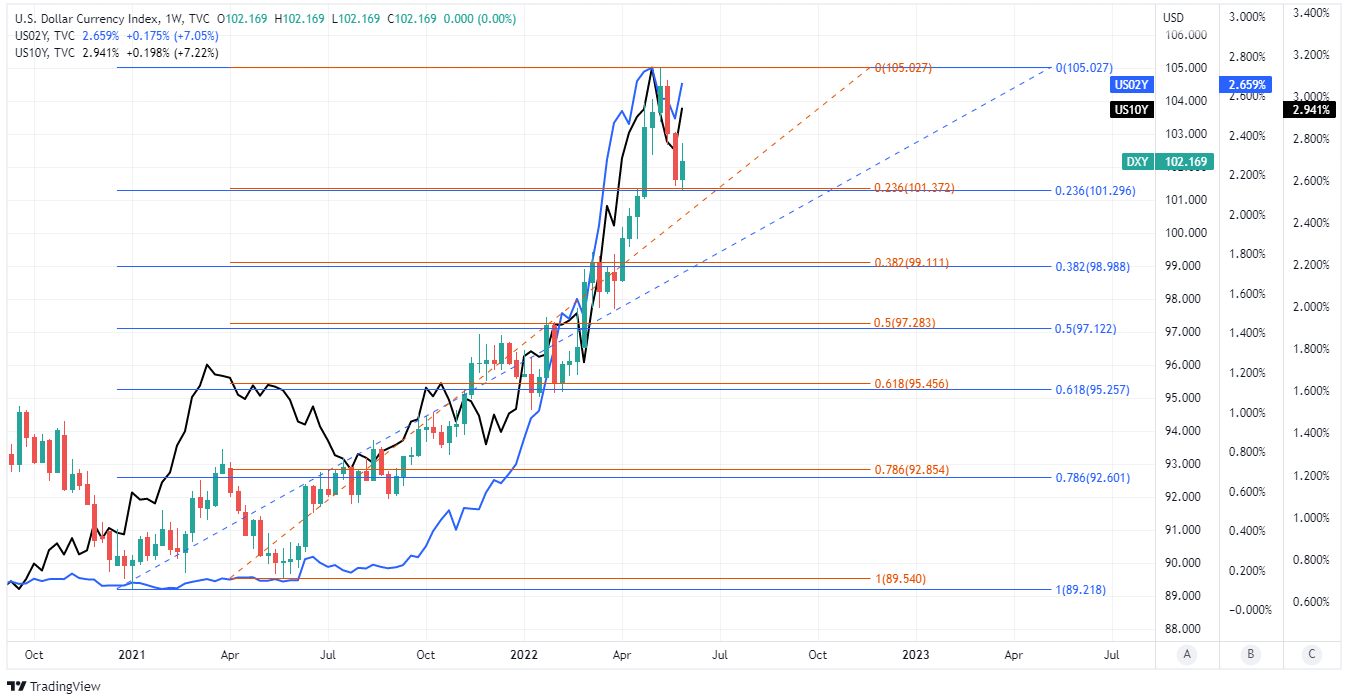

Above: U.S. Dollar Index shown at weekly intervals with Fibonacci retracements of January and June 2021 recoveries indicating possible short and medium-term areas of technical support for U.S. Dollar and selected U.S. government bond yields. Click image for more detailed inspection.

Above: U.S. Dollar Index shown at weekly intervals with Fibonacci retracements of January and June 2021 recoveries indicating possible short and medium-term areas of technical support for U.S. Dollar and selected U.S. government bond yields. Click image for more detailed inspection.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

Elsewhere the Euro will also likely be sensitive this week to the release of U.S. inflation figures for the month of May, and especially whether or not they continue to tell a story of month-on-month price pressures being in retreat.

This is after Federal Reserve policymakers appeared to indicate last week that they are still at risk of becoming more ‘hawkish’ with their interest rate outlooks in the months ahead if U.S. inflation rates do not continue to come down, which implies ongoing upside risks for the Dollar.

“On inflation I am going to be looking to see a consistent string of decelerating monthly prints on core inflation before I am going to feel more confident that we’re getting to the kind of inflation trajectory that is going to get us back to our two percent goal. In terms of our tools, they are very effective at cooling aggregate demand,” Vice Chair of the Fed Board Lael Brainard said Thursday.

Elsewhere in Fedspeak last week Federal Reserve Bank of Cleveland President Loretta Mester suggested the Fed’s interest rate may yet have to be lifted above the neutral rate this year, which is estimated to be between 2% and 3%, while board colleague Christopher Waller came across almost as hawkish as Federal Reserve Bank of St Louis President James Bullard.

“I support tightening policy by another 50 basis points for several meetings. In particular, I am not taking 50 basis-point hikes off the table until I see inflation coming down closer to our 2 percent target. And, by the end of this year, I support having the policy rate at a level above neutral so that it is reducing demand for products and labor, bringing it more in line with supply and thus helping rein in inflation,” Governor Waller said in part.