Euro-Dollar Back on it's Feet but Central Bank Log Jam May Stifle Recovery

- Written by: James Skinner

- EUR/USD recovers 1.19 after USD’s momentum fades

- But relative central bank stances may stifle recovery

- As Fed questions market pricing & ECB stands pat

Image © European Central Bank

- EUR/USD reference rates at publication:

- Spot: 1.1908

- Bank transfers (indicative guide): 1.1485-1.1569

- Money transfer specialist rates (indicative): 1.1795-1.1819

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Euro-to-Dollar exchange rate has wrestled back the 1.19 handle in an effort to draw a line under the Dollar's June rally, although evolving central bank policies on each side of the Atlantic risk making any further recovery by the single currency a stiflingly slow affair.

The Euro had appeared in danger of falling to April lows around 1.17 when June’s Federal Reserve (Fed) dot-plot of policymaker forecasts showed a majority of Federal Open Market Committee (FOMC) members minded to vote for higher interest rates sooner than was previously indicated.

Pricing in derivative markets suggests investors think U.S. interest rates could begin rising in the latter part of next year, and that the Fed Funds rate range could rise three quarters of a percent to 1% by the end of 2023, although after Chairman Jerome Powell and some other senior members of the FOMC hit the post-policy-meeting speaking circuit last week, the Dollar has lost momentum and other currencies like the Euro have caught a breather.

"The Fed leadership still wants to see the US economy close to full employment before rising rates. The latest NFP report will provide insight into how long it will take for the labour market to fully recover. Absent a significant upside surprise, recent USD gains should reverse further," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

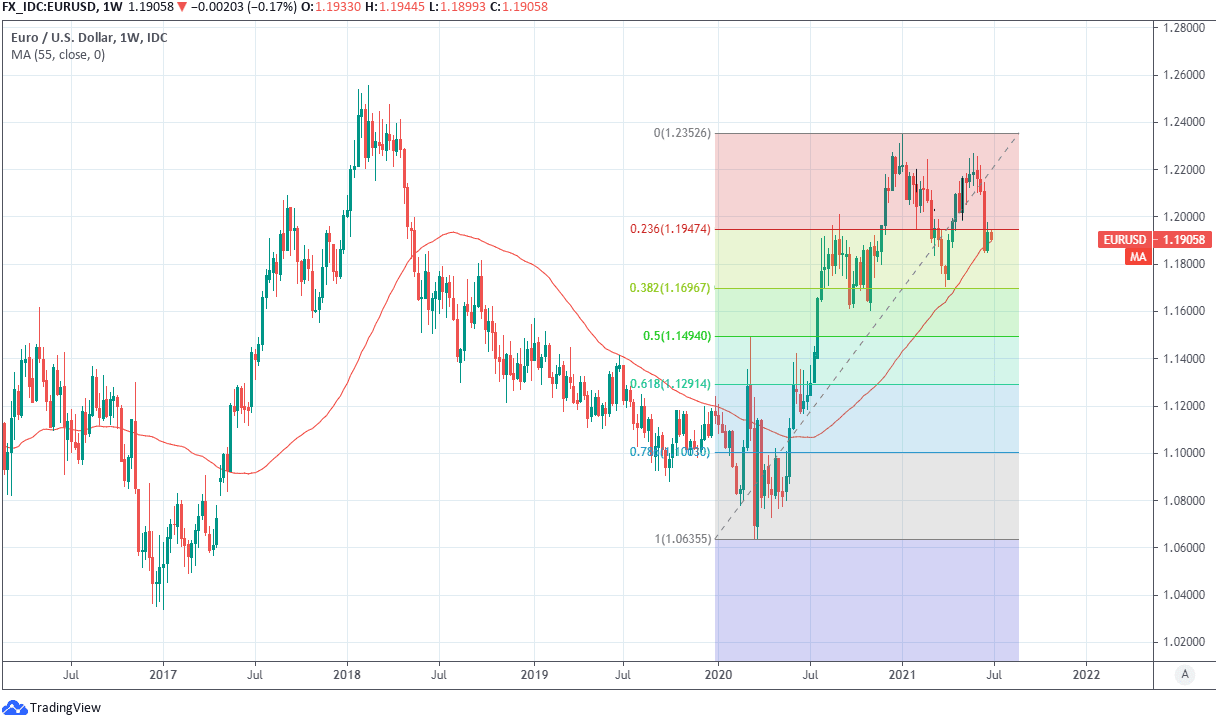

The Euro-Dollar rate’s declines were arrested last week when the single currency drew a bid from the market around the level of its 55-week moving-average near 1.1850, and it’s since reclaimed the 1.19 handle, although much now depends on the rhetoric and evolving stances of the Fed and the European Central Bank (ECB).

Above: Euro-Dollar at weekly intervals with Fibonacci retracements of 2020 recovery and 55-week moving-average.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

“What we can say is that in Q1 the stimulus led to a large revision of US economic expectations by economists, making it tough for the data to actually “surprise.” Meanwhile, for the euro area it’s the opposite, with the Q1 vaccine trouble lowering growth expectations. This low bar should keep EUR supported with a set of potentially “better-than-expected” data to come,” says Jordan Rochester, a strategist at Nomura.

Most notable for the European and U.S. currencies is whether what was perceived in June as a moment of fledgling divergence between the two central banks is sustained, or if that perception is taken apart at the seams with rhetoric from Fed Chairman Jerome Powell and FOMC colleagues as they continue on the speaking circuit.

“The reality is that US rate hikes are still not close enough to trigger a sustained reversal of reflation trades and stronger USD,” MUFG's Halpenny says.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Chairman Powell suggested strongly last week that the market may be being overly optimistic with its expectations for U.S. interest rates, saying in Congress that the Fed will wait to see its 2% inflation target achieved as an average over time and focus along the way on delivering a “broadly inclusive” form of full employment.

That means economic numbers like this Friday’s non-farm payrolls are of enhanced importance because perceptions of the job market’s recovery and of the degree to which inflation is likely to remain elevated up ahead will both have an impact on expectations of Fed policy as well as potentially the Euro and Dollar too.

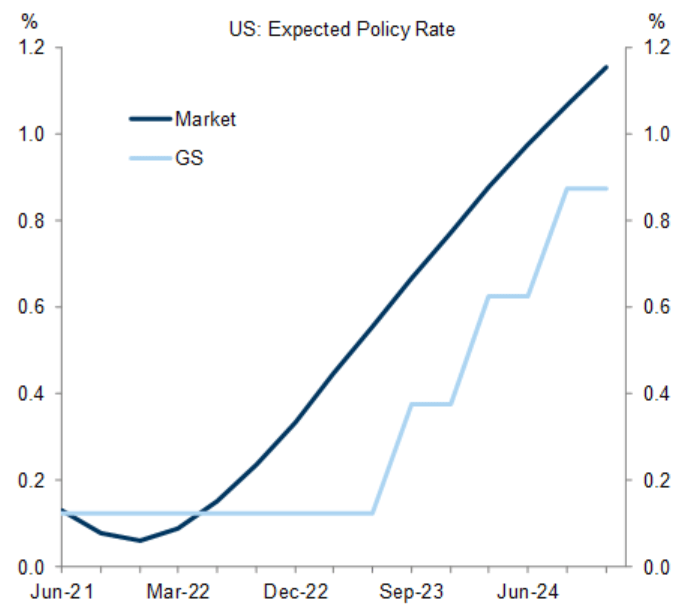

“We would caution against extrapolating the hawkish Fed signal too far, ahead of the substantial deceleration we expect into 2022. For now, we stay on the sidelines in G10 vs USD,” says Zach Pandl, co-head of global foreign exchange strategy at Goldman Sachs.

Above: Market expectations for percentage point changes in Federal Funds rate range, alongside Goldman Sachs’ forecasts.

“In our revised forecasts, EUR/USD reaches 1.20 in 3m, 1.23 in 6m, and 1.25 in 12m. Over the near-term, our forecast that EUR will move sideways partly reflects our expectation that the FOMC will hold off on any announcement around tapering its bond purchases until Q4,” Pandl adds.

The Fed’s June policy update prompted a rush among currency traders to buy the Dollar or exit wagers against it, with the latter being bets which had previously benefited the Euro-Dollar rate, and after all was said and done investors came down in the end on the side of the small minority of FOMC members who voted to lift the Fed Funds rate in late 2022: but it's since become clear that influential voices on the FOMC are at the other end of the field.

“The fed has tended to be less divided than the UK MPC (for example) but there are signs of a split, which only heightens sensitivity to the data, which is what will win the argument in the end,” says Kit Juckes, chief FX strategist at Societe Generale.

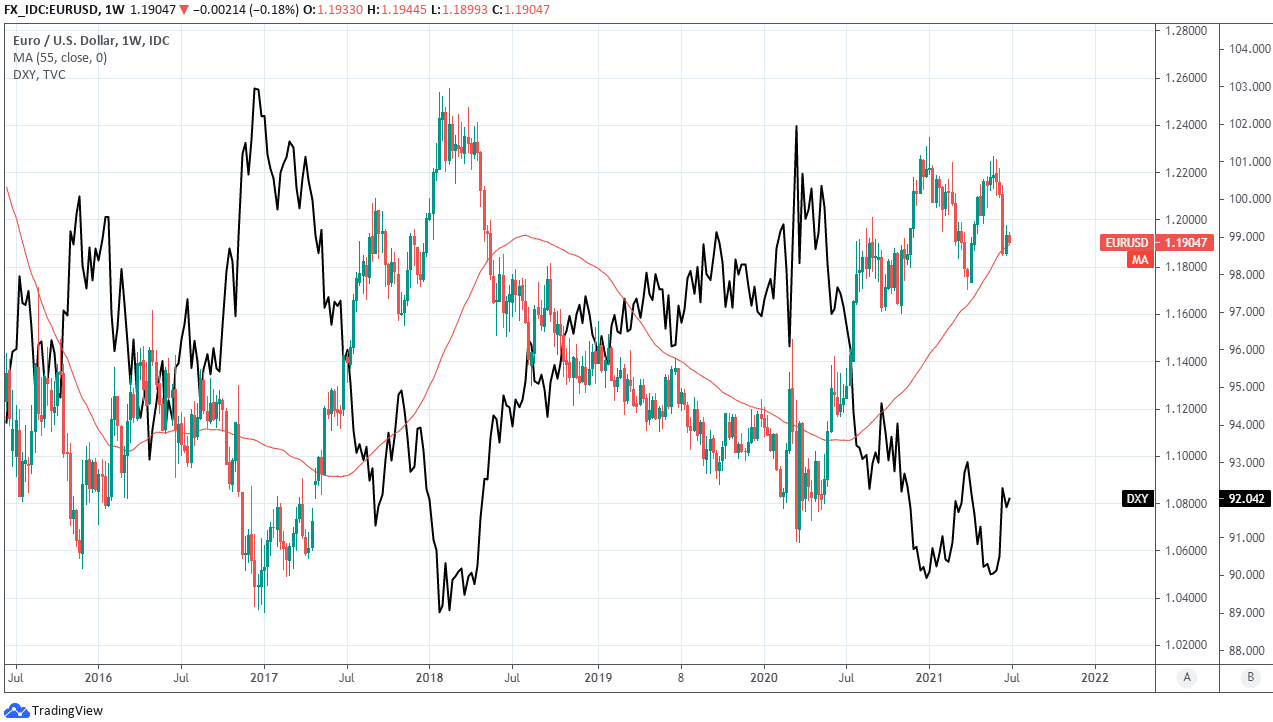

“For now, the dollar has lost momentum, the DXY 200-day average at 91.5 bears watching and so too does 1.20 for EUR/USD. Neither the ECB nor the European economy is doing anything to support the euro,” Juckes adds in a Friday note.

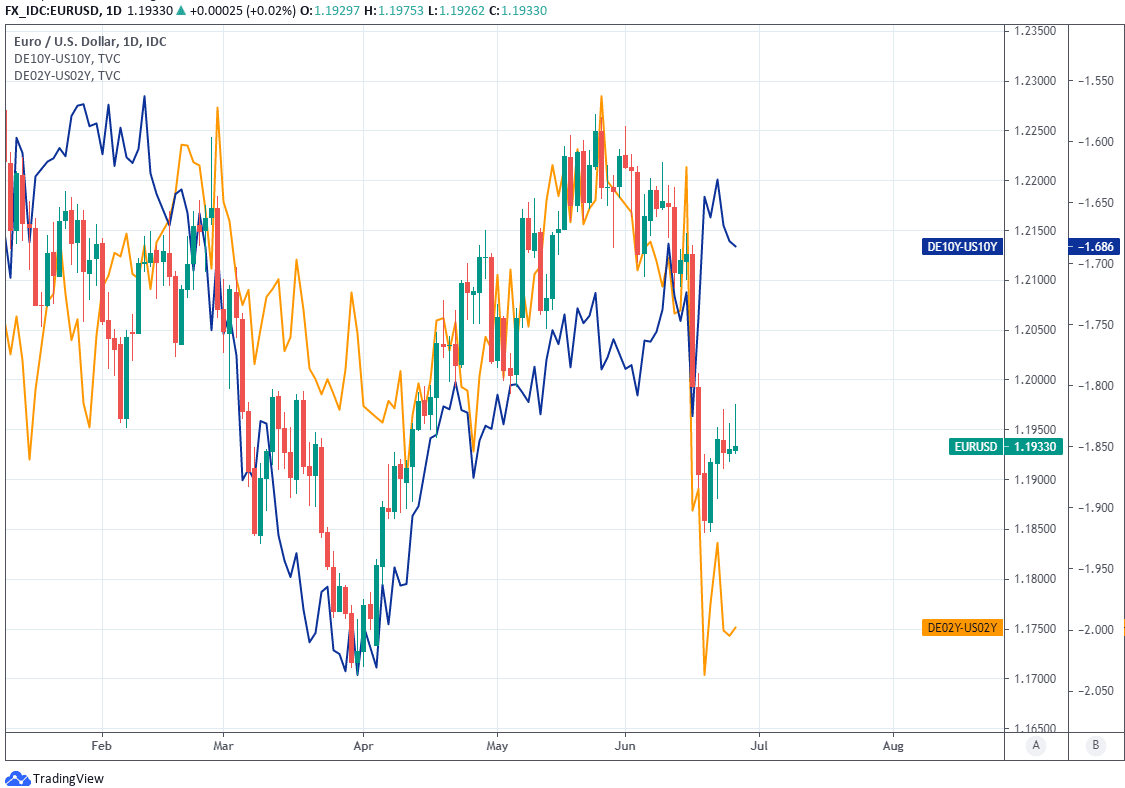

Above: Euro-to-Dollar rate shown at daily intervals with 02-year & 10-year German-U.S. bond yield differentials.

Chairman Powell told Congress last week the Fed “will not raise interest rates preemptively because we think employment is too high or because we fear the possible onset of inflation,” and that recent increases in inflation, to more than five percent over recent months, have been driven mainly by one-off changes in sectors that are reopening from earlier closures: The bank's idea is that these increases will likely prove “transitory.”

“Bill Dudley, ex New York Fed President, suggested yesterday that the views of Jay Powell, Richard Clarida and John Williams are the ones that matter at the Fed. Williams was on the tapes yesterday saying he doesn't see a case to raise rates any time soon, while James Bullard was the latest to suggest rates should rise by the end of 2022,” Societe Generale’s Juckes says.

There's a range of reasons why the Fed's monetary support for the U.S. economy could be prolonged including the bank's relatively new pursuit of a “broadly inclusive” definition of maximum sustainable employment when working to that side of its mandate, which is an outcome that has not typically if-ever been delivered by past policy cycles and one which could necessitate an extended period of support from the Fed.

Above: Euro-Dollar rate shown at weekly intervals with U.S. Dollar Index.

And to the extent that these or the words of Fed officials give markets cause to doubt new assumptions about borrowing costs, they could undermine the fragile foundations on which the Dollar’s comeback is built and potentially offer further support to the single currency around the recently recovered 1.19 level.

However, and even in the event of a Euro-Dollar recovery, the single currency may find itself with only limited scope to rise given that European Central Bank monetary policy continues to bar its path higher; The ECB's Pandemic Emergency Purchase Programme of government bond purchases is a weight around the Euro's ankles.

It's also why even if the Dollar weakens afresh upon any market realisation that a normalisation of Fed monetary policy could still be some time away, any Euro-Dollar rate recovery would be a somewhat stifled affair.

“We expect the ECB is still a long way from easing monetary policy support. And in the meantime, relative FOMC and ECB asset purchases will remain a headwind to EUR,” says Kim Mundy, a strategist at Commonwealth Bank of Australia.

“Indeed, we expect the FOMC to start tapering its asset purchase program in October. In contrast, we expect the ECB’s asset purchase program to continue well into 2022,” Mundy adds in a Friday research note.