Pound Sterling Recovers Against Euro, Supported By Bond Yield Divergence

- Written by: Gary Howes

Image © Adobe Images

The British Pound recovered ground against the Euro, Dollar and other major currencies following the sharp drops experienced on Monday, underscoring ongoing yield support for the UK currency.

The recovery confirms what we suspected, namely that tactical and flow considerations drove the moves, particularly given February's status as a traditionally weak month for the Pound.

The Pound remains fundamentally supported by UK bond yields that have recovered faster than elsewhere (excluding the U.S.) in 2024, as markets faded expectations for the start time and degree of interest rate cuts to come from the Bank of England.

The Pound to Euro exchange rate has returned to above the 1.17 level at the time of writing and trades above its major moving averages, confirming broader momentum studies to be supportive.

"GBP continued its winning streak into the first month of the year, outperforming most of G10, except for USD, on the back of the UK’s 2Y swap rate rising by more than most other G10 economies," says Daria Parkhomenko, an analyst at RBC Capital Markets.

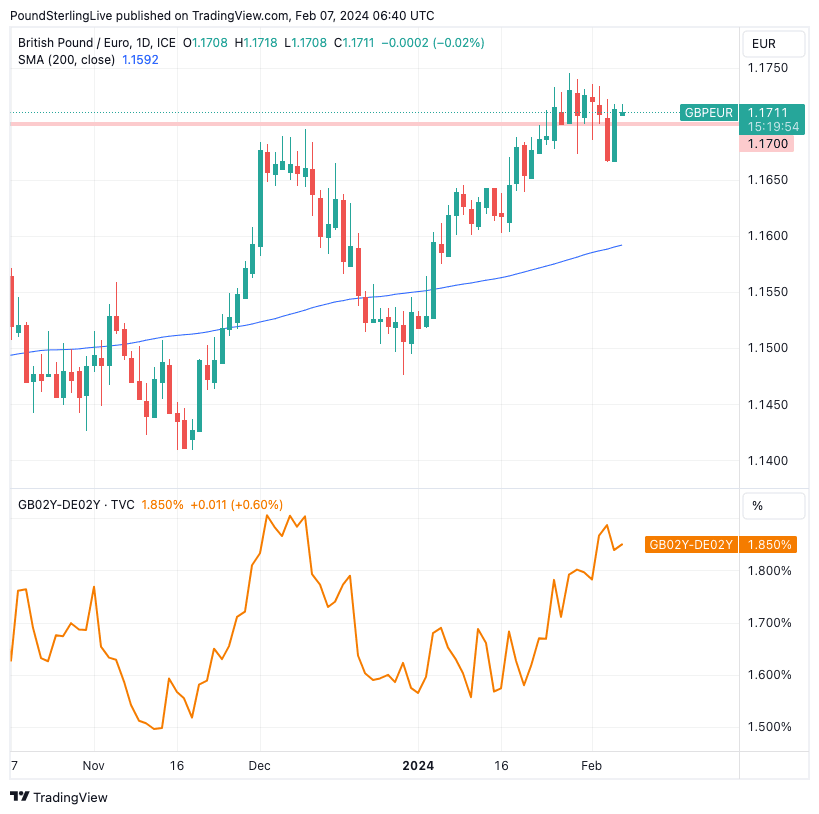

Above: GBP/EUR and the differential between the UK and German two-year government bond (lower panel). Track GBP/EUR with your own custom rate alerts. Set Up Here

The above chart shows Pound-Euro and the differential between the UK and German two-year government bond: as can be seen, 2024 has seen the differential widen, which has boosted Pound Sterling.

This speaks of divergence in expectations for Eurozone and UK monetary policy, with the market indicating it sees the European Central Bank cutting interest rates before the Bank of England.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Underscoring this view is the belief that Eurozone inflation will return to the 2.0% target quicker than that in the UK. By contrast, the Bank of England reckons UK inflation will fall back to 2.0% as early as April but will rise back to 3.0% by year-end.

The lift in UK bond yields relative to its German counterpart reflects this expectation, underpinning the Pound-Euro exchange rate in the process.

The Bank of England signalled on February 01 that while the next move in interest rates would likely be a cut, it was still too soon to consider such a move.

"Following the shift in the MPC’s rhetoric, our economists now expect the BoE to start cutting rates in August and lower the policy rate by a total of 100bps to 4.25% by the of 2024. Although the magnitude is similar to market pricing -97bps by year-end, this would still mean the BoE will start cutting rates later than the Fed and the ECB (RBC expects both to start in June)," says Parkhomenko.

"The BoE’s more gradual shift to rate cuts than peers removes a reason to sell GBP," adds the analyst.

Despite the setup in Pound-Euro remaining supportive, it is still difficult to see a break above the 1.1750 highs transpiring in the near future; we note this has not been achieved since 2021. For this to happen, we would need to see further upside surprises in UK data, while the Eurozone and German economies must continue to disappoint.

With peak Eurozone pessimism near, it is difficult to see this happening.

"Although GBP may further benefit from decent carry in the near-term, we don’t yet see a catalyst to drive an outright GBP-bullish view on a longer-run horizon," says Parkhomenko.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes