GBP/NZD Week Ahead Forecast: Heavily Overbought

- Written by: Gary Howes

Image © Adobe Images

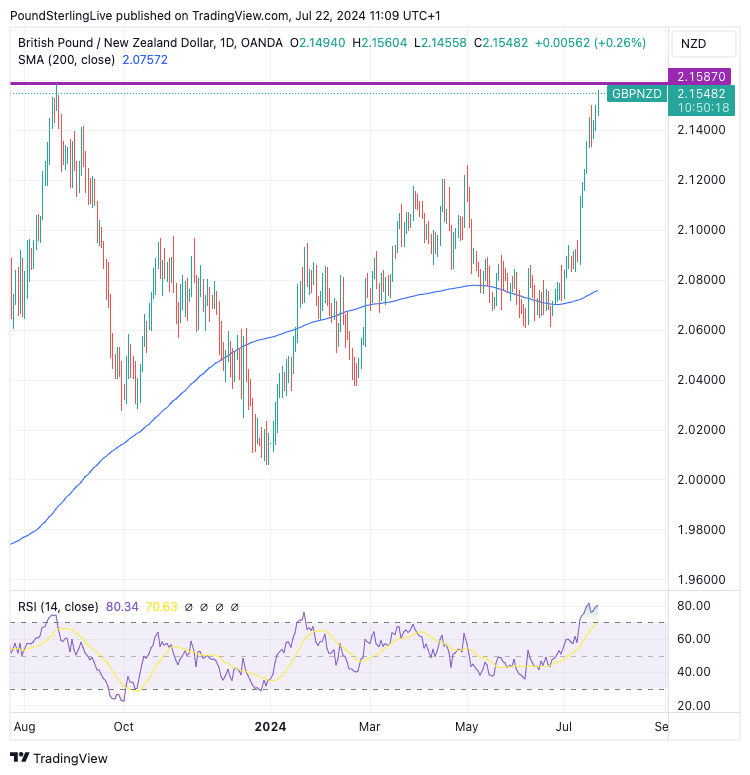

The Pound to New Zealand Dollar is on course to break the 2023 high at 2.1587, but warning lights are flashing that this is a very overbought exchange rate.

The GBP/MZD rally is strong; it is now testing its highest level in nearly a year and trading well above its major moving averages.

These moving averages are also pointed higher, confirming momentum is firm and advocating for further upside.

We forecast that a test above the August 2023 high at 2.1587 is a distinct possibility. (Note that GBP/NZD is trading well ahead of the 2024-2025 median forecast of over 30 of the world's investment banks).

However, the daily RSI is at 80.55 and is considered extremely overbought (see lower panel in below). Unusually, the RSI has been overbought for 12 days now. This serves as a reminder that overbought conditions are no automatic trigger for a correction.

Track GBP/NZD with your custom alerts; find out more here

Yet, we wonder how long this overbought momentum can be sustained; even a consolidation at current levels will be enough to let some heat out of the market.

The approach of 2023 high at 2.1587 could also represent a major resistance area that triggers some profit-taking in the pair, in view of the overbought conditions.

Given the stretched nature of the market, any pullbacks could be quite sudden and deep.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

So, those with GBP/NZD requirements are urged to be nimble.

Global sentiment has a strong hold on NZD, with recent declines aligning with a broader stock market selloff.

This was exacerbated on Monday by a surprise interest rate cut at the Bank of China (PBoC), which analysts say could be an admission that the economy continues to face headwinds.

The PBoC unexpectedly cut interest rates 10 basis points to 1.70%. "The PBoC cut may be the start of 2H easing to help the economy get to 5% growth, as the 3rd plenum reiterated the pledge to hit the 2024 target," says Wei Yao, Head of Research Asia Pacific at Société Générale.

For now, markets view cuts as a sign of weakness and concern over China's prospects, which will weigh on China-linked assets such as NZD and AUD. In fact, AUD is leading the losses at the start of the week, which is understandable given it is the most vulnerable of the G10 currencies to Chinese sentiment.

Keep in mind that the overall settings that underpin a multi-month rally in stock markets still remain intact. This is especially the case given the Federal Reserve now looks likely to enter a rate cutting cycle in September.

When the rally resumes, the NZD might find itself better supported.

"Barring major surprises, we still believe investors should stay the course and not make major changes to their portfolios," says Carsten Menke, Head of Next Generation Research at Julius Baer.