GBP/NZD Week Ahead Forecast: "Whippy"

- Written by: Gary Howes

- GBPNZD uptrend remains intact

- But near-term price action is choppy

- NZ labour market in focus Wednesday

- GBP in focus Thursday on Bank of England decision

Image © Adobe Stock

The Pound to New Zealand Dollar exchange rate (GBPNZD) starts the new week on the defensive but there is a high likelihood that losses will be recouped over the coming days.

The exchange rate is proving notably volatile, but within a tight range, which raises the odds we will continue to see price action restricted to between the 2023 highs near 2.0910 and recent lows near 2.0500.

"Price action has been whippy, and it's been buffeted by global news," says David Croy, a strategist at ANZ.

That said, the broader trend in GBPNZD does still appear to be higher and should the Bank of England this week deliver a 'hawkish' 50 basis point interest rate hike, accompanied by relatively unchanged guidance, a potential break to new 2023 highs could be in prospect.

"GBP still in its multi-month upward trend channel; that may be a threat to this cross," says Croy.

Above: GBPNZD maintains a tight range, albeit within the context of a medium-term uptrend.

The Bank of England could however opt to raise interest rates by 'only' 25bp on Thursday, in a slowdown from June's surprise 50bp hike, citing June's below-consensus inflation report.

The recent Federal Reserve and European Central Bank decisions were on the soft side with both central banks not committing to further hikes, potentially offering the Bank of England the option to signal it too could be approaching the end of its hiking cycle.

Such guidance would result in Pound Sterling weakness, prompting a retreat in the GBPNZD exchange rate towards its June-July lows.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

Ongoing market dynamics do however suggest any weakness in GBPNZD will be limited, given the slowdown in the New Zealand economy and the Reserve Bank of New Zealand's (RBNZ) confirmation that it has likely ended its interest rate-raising cycle.

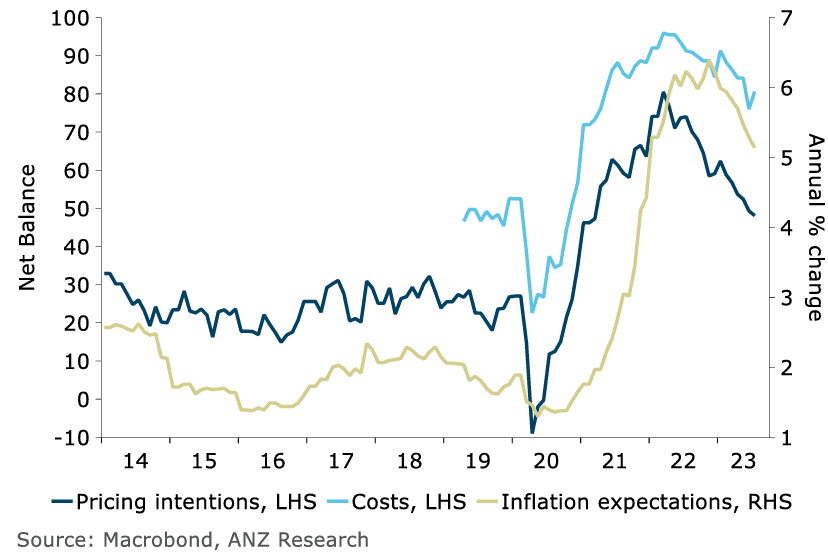

ANZ's New Zealand Business Outlook for July - released on Monday - reported confidence has ticked up slightly from suppressed levels in July, confirming the domestic economy was evolving in line with RBNZ expectations.

However, the proportion of firms expecting to raise wages increased, hinting at ongoing domestic inflationary pressures, even as firms' expectations for price dynamics remain pointed lower.

Wage and labour dynamics are in focus later this week when the official labour market data are released on Wednesday.

"NZ labour market data on Wednesday is this week’s local highlight. We expect employment is still north of its maximum sustainable level, but with the slowing economy and stronger population growth increasingly freeing up capacity," says Nathaniel Keall, an economist at ASB.

Above: NZ business inflation expectations as per the ANZBO report for July.

Consensus expects the unemployment rate to have risen from 3.4% to 3.5% while the labour cost index is expected to have fallen to 4.4% from 4.5% year-on-year in the second quarter.

This would hint at falling domestic inflationary pressures and any reading below this could prompt NZ Dollar weakness, but a beat on expectations would potentially have the opposite effect.

"This week the focus returns to domestic factors, with the release of Q2 labour market data. While we’re forecasting a small lift in unemployment, we also expect wage growth to be robust and that is one of the things that might keep the RBNZ on edge, underscoring that the RBNZ may need to hike again," says Croy.

The headline employment change is expected at 0.6% q/q in the second quarter, down on 0.8% in the first quarter, hinting at easing labour market conditions that would justify the RBNZ's pause.

Although the labour market statistics form this week's highlight for the NZ Dollar, it will likely be global drivers that will have the broader impact.

Last week we saw the New Zealand Dollar take cues from both U.S. and Chinese data releases and would expect the same over the coming days as global investor sentiment is a key driver of this currency.

The U.S. labour market report out Friday is of particular interest with a strong report likely to boost the U.S. Dollar and weigh on sentiment, which could undermine the Kiwi if market bets for further Fed hikes rise.

But, more generally, sentiment remains broadly buoyant with investors betting the U.S. economy is likely to avoid a 'hard landing' scenario whereby the economy falls into recession owing to interest rate rises at the Federal Reserve.

Ongoing firm activity data, falling inflation and expectations that the Fed is close to ending its rate hiking cycle all underscore this optimistic theme and can keep the NZD supported over the coming days.

The Kiwi was up against the majority of its peers after the Fed last week confirmed a further rate hike in September was not a done deal, instead preferring to base its next decision on the flavour of incoming data.

The outcome was consistent with an improved investor sentiment linked to expectations that the interest rate hiking cycle in the U.S. has come to an end; a sentiment which tends to support the New Zealand Dollar.

With this in mind, investors will remain alert to any negative data surprises that would upend this trend, and mid-month U.S. inflation figures due mid-month will therefore be closely watched.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes