Sharp Falls in Inflation Dents Pound Sterling's Advance against Euro and Dollar

- Written by: Gary Howes

- GBP/EUR @ 1.1259, down 0.70%

- GBP/USD @ 1.2064, down 0.91%

- UK inflation falls faster than expected

- Headline CPI at 10.1% in Jan vs. 10.5% in Dec

- Core CPI at -0.9% vs. 0.5% in Dec

- Weighs on UK bond yields

- As investors 'price out' extent of further rate hikes at BoE

Image © Adobe Images

Consumers and policymakers at the Bank of England will breathe a sigh of relief on receiving today's inflation numbers that showed some sharp falls in the rate of price increases in January.

Borrowing costs and the British Pound meanwhile fell after it was reported UK headline CPI inflation declined to 10.1% year-on-year in January (markets were primed for 10.3%), from 10.5% in December.

The headline figure was driven lower by a sharp -0.6% month-on-month reading in January said the ONS, which was more than the -0.4% the market was looking for and December's 0.4% growth.

The declines weighed on UK bond yields as investors 'priced out' the extent of further rate hikes that were likely to come from the Bank of England.

This repricing mechanically weighed on the Pound to Euro exchange rate (GBP/EUR) which was lower by a third of a percent at 1.1308 and the Pound to Dollar exchange rate (GBP/USD) which was lower by half a percent at 1.2111.

Above: CPI inflation with core inflation (green line). Source: ONS.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

But it was the fall in core inflation that will have convinced the market that the Bank will be resting a little easier following today's release. After all, this is the inflation that best represents domestic inflationary developments as it strips out external variables such as energy and food.

Core inflation fell a sizeable 0.9% month-on-month in January, which was far more than the -0.5% the market was expecting and represents a sharp decline from the 0.5% growth seen in December.

Core inflation was down to 5.8% in the year to January from 6.3% in December, exceeding the consensus expectation for a 6.2% reading.

Analysts at MUFG Bank see this data as potentially bringing back the idea of a pause at the Bank of England.

"The BoE’s own forecasts estimated a Q1 2023 annual inflation rate of 9.73% and with the base effects very favourable from February through April, there is certainly a good chance of the BoE’s own projection being too high," says Derek Halpenny, Head of Research for Global Markets EMEA at MUFG.

Above: GBP/EUR (top) and GBP/USD at 5-minute intervals. Consider setting a free FX rate alert here to better time your payment requirements.

The decline in GBP/EUR spot to 1.13 takes the typical bank rate for international payments to around 1.1070, competitive cash and holiday money rates to around 1.1156 and competitive transfer provider rates to around 1.1266.

For GBP/USD, the typical bank rate for international payments is seen at approximately 1.1848, competitive cash and holiday money rates to around 1.1986 and competitive transfer provider rates to around 1.2050.

The decline in Sterling's value reflects the market's expectation for less Bank of England intervention over the coming months as inflation falls back to the 2.0% target.

"We continue to expect the headline rate to fall to about 2% by the end of this year," says Samuel Tombs, Chief U.K. Economist at Pantheon Macroeconomics.

Yet faster-than-expected declines in inflation are good for the UK consumer and therefore support the outlook for UK economic growth, which is widely expected to contract in 2023.

This recalibration would limit the downside for Pound exchange rates over the medium term.

The expected sharp falls in inflation will follow a fall in wholesale prices, says Tombs.

Pantheon Economics expects CPI inflation rates for electricity and natural gas will slump to about -10% by the end of the year, from their 65% and 129% rates in January.

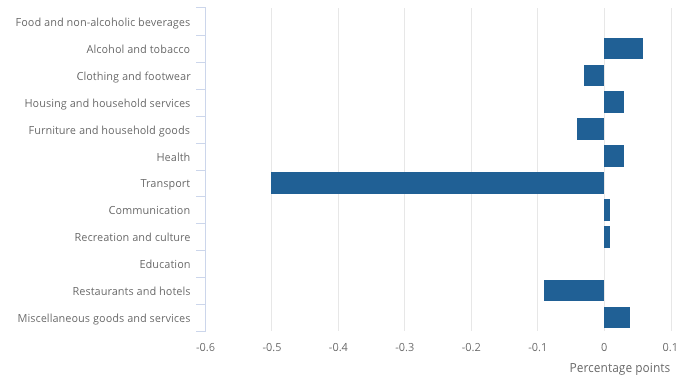

Above: The drivers of inflation and disinflation. Source: ONS.

However, Rhys Herbert, an economist at Lloyds Bank, says although inflation will fall sharply further this year, "it seems unlikely to drop back to the Bank of England’s 2% target until the second half of 2024."

Differences in opinion amongst economists as to how fast inflation will fall will keep alive uncertainty as to the outlook for UK interest rates.

"The cocktail of a tight labour market and inflation failing to cool off quickly will remain a cause of concern for Bank of England policymakers, which may mean the Bank’s aggressive strategy stays in place," says Richard Carter, head of fixed interest research at Quilter Cheviot.

The Bank is widely tipped to hike by 25 basis points in March, before hitting the pause button.

Money markets meanwhile show investors are anticipating a cut to interest rates towards the latter part of the year.

Should inflation continue to decelerate the likelihood of those rate cuts will increase, potentially pressuring Sterling.

But, if UK growth expectations were to improve the Pound could find itself better supported.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes