Navarro's Truth Hurts: Germany is Gaining an Unfair Advantage from a Chronically Undervalued Euro

Foreign exchange markets have been rocked by politics once more.

The speed with which Donald Trump has sought to deliver on his campaign promises has come as a surprise to the established geopolitical order, and as we know, surprises are what move currencies.

The President has certainly delivered on many of his campaign promises - but there is one glaring ommission - labelling China a currency manipulator.

We believe there is good reason why he hasn’t - simply because China is no longer a currency manipulator.

Research shows that if anything, the Yuan is perhaps the most expensive currencies out there at present which in turn suggests China is actually losing valuable GDP growth as a result of its good being more expensive on the global marketplace than its economic fundamentals justify.

But that does not mean the words "currency manipulator" won’t pass through Trump's lips.

There is reason to believe that they might yet; and it could be that his target will be traditional ally Germany.

The warning shots for such an unprecedented call were fired by Donald Trump’s trade adviser Peter Navarro when he told the FT that the Euro “grossly undervalued".

The adviser said on Tuesday, January 31 the Euro was an “implicit Deutsche Mark" that gave Germany a competitive advantage over its trade partners.

Navarro's gripe is that Germany is gaining undue benefit from a currency that is too low. This matters for an administration that is keen to reverse the United States' decline in exporting ability.

Indeed, data from the Ifo Institute shows that net imports from Germany account for half of the United States current account deficit.

"The comments from Donald Trump’s team will irk Angela Merkel’s Germany. The truth hurts. It’s well understood that the Euro is weaker than the Deutsche Mark and stronger than the Spanish Peseta or Greek Drachma would have been, which tilts trade in favour of the more industrious Germany," says Jasper Lawler, a currency analyst at CMC Markets in London.

Germany is Having its Cake and Eating it

Navarro - an economics professor in another life - has spelled out a simple truth; that the Euro gives Germany a competitive advantage in global trade.

Could you imagine how much stronger the Euro would be were the likes of Greece, Spain and other peripheral states not in the Eurozone?

The Euro would be significantly higher were no sovereign debt crises and seemingly unlimited printing of Euros at the European Central Bank, aimed at keeping the Eurozone’s weaker members afloat?

Of course, it would be wrong to say that the desire to have these anchors on the currency are an intentional strategy, but the situation does help the mighty German economy which would otherwise command a stronger currency which would in turn dampen global demand for its exports.

The benefits derived from the weaker currency ensure it can pump exports into the global economy at discounted prices.

That is why Germany is able to enjoy the current account surplus it does - it exports more than it imports.

A recent report out this week has shown just how much the German economy is enjoying its weak currency as its current account surplus is expected to have hit a new record of $297 billion in 2016, overtaking that of China again to become the world's largest, the Munich-based Ifo economic institute said on Monday.

In 2015 the current account surplus stood at $271 billion.

This would be equivalent to 8.6% of total output, which means it would once again breach the European Commission's recommended upper threshold of 6 percent.

The Ifo, who compiled the report, went so far as branding Germany as the capital export world champion in 2016 with the USA branded the capital import champion.

This confirms a heavy bias in favour of Germany in USA-German trade relations, and Trump will take notice.

Germany Can be Called a Currency Manipulator

Indeed, by current rules, set out by the Obama administration, Germany could be called a currency manipulator.

Every year, the US Treasury Department conducts reviews in April and October to determine which country on the monitoring list will be named.

Analysts at Bank of America Merrill Lynch Global Research have looked into the matter and reported that China fails to meet 2 out of the 3 conditions named below, even though it is on the watch list together with 5 other economies - Japan, Germany, South Korea, Taiwan and Switzerland.

The three rules to being labelled a currency manipulator are:

- Bilateral trade surplus against the US above US$20bn.

- Current account surplus exceeds 3% of its GDP.

- Official FX purchases exceed 2% of its GDP.

The Euro is Undervalued

Another question markets will want answered is whether the Euro is undervalued?

By many studies, yes it is.

But there is one benchmark that matters more than others.

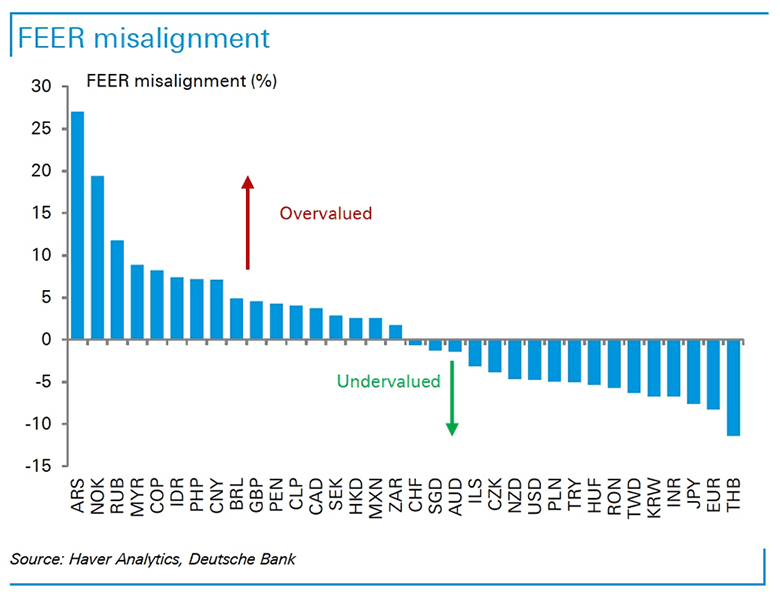

According to research by Deutsche Bank, in December the Euro was the world’s most undervalued major currency based on a FEER study.

FEER stands for Fundamental Equilibrium Exchange Rates (FEERs) - this is the exchange rate needed to ensure that the current account balance converges to a sustainable level over the medium term.

This is therefore a very relevant study when trying to gauge just how much a country is benefiting from an undervalued currency.

Note in the above that a lot of those countries that we mentioned could be branded guilty of currency manipulation under the existing US framework score low on the FEER gauge.

Trump apparently has the ammunition he needs to blast Germany on this front.

FEER is not the only way of gauging a currency's fair valuation though, there are others.

And unfortuantely for Germany, on all fronts the Euro comes in as being undervalued.

The above represents the findings of Deutsche Bank's work on currency value, using a number of analytical models.

When you put them all together, we can see the Euro is notably undervalued.

However, what about the Yen? This is an incredibly cheap currency and unlike Germany, Japanese officials have direct control over their monetary policy.

We would not be surprised if this front isn't also opened up by Trump.

But it’s Not Germany’s Fault

As I mentioned above, Germany cannot be said to be guilty of currency manipulation as the currency’s value is in fact a rather nice bonus stemming from European unity.

Chancellor Merkel has responded to Navarro’s claims accordingly:

“We won’t exercise any influence over the European Central Bank, so I can’t and I don’t want to change the situation as it is now,” Merkel said in Stockholm Tuesday after meeting with Swedish Prime Minister Stefan Lofven.

“Beyond that, we strive to trade on the global market with competitive products in fair trade with all others,” said the Chancellor.

Regardless of Merkel's protestations, it looks like Germany, and the Eurozone, might have an orange-tanned headache coming their way.