Pound Sterling to Return to May Highs this Summer as Euro Struggles: Capital Economics Forecast

- Written by: James Skinner

© pawopa3336, Adobe Stock

- GBP to claw back earlier gains from EUR by end-September.

- As ECB gears up for fresh bond-buying program, hurting EUR.

- GBPUSD to remain depressed as the Brexit saga drags on.

- No deal Brexit risk, go-slow UK economy weigh on GBPUSD.

The Pound is set to recover all of its recent losses to the Euro over the summer months, according to forecasts from Capital Economics, although the Pound-to-Euro exchange rate increase is expected to be more a function of weakness in the European single currency rather than a universal recovery by the British unit.

Pound Sterling slumped steeply against the Euro throughout the months of May and June Prime Minister Theresa May announced her resignation, which has paved the way for a leadership election that looks likely to put a Brexit-backing Boris Johnson in 10 Downing Street, in turn raising expectations for a 'no deal' Brexit on October 31.

Johnson has told colleagues and party members he intends to attempt to negotiate changes to the EU withdrawal agreement brought back from Brussels by Prime Minister Theresa May, with a view to having the so-called Northern Irish backstop stripped out of it.

"Despite the narrowing in the gap between 2-year government bond yields in the US and the UK to around 100bps, which would normally put upward pressure on Sterling in relation to the Dollar, the Pound has come under renewed pressure falling to $1.27. It has also weakened against the Euro," says Paul Dales, chief UK economist at Capital Economics, in a note to clients. "This is mainly because investors have become more concerned about a no deal Brexit."

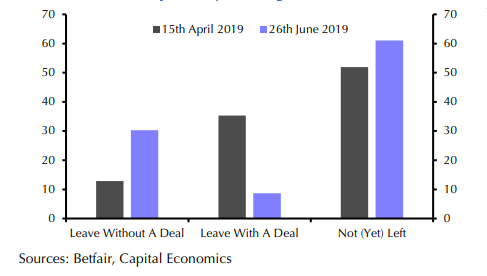

Above: Capital Economics graph of Brexit probabilities.

Parliament has rejected the new EU treaty three times in 2019, with many of the 'noe' votes on the government's benches in the House of Commons being the result of objections to the contentious provision, which is said by both UK and EU officials to be necessary for the sake of the Good Friday Agreement.

Without the 'backstop', the UK and EU would each face seeing their 'single market' compromised, which is something the EU appears unwilling to countenance.

The EU says it will not renegotiate the agreement containing the provision and that it won't agree to an extension of the Article 50 negotiating window beyond October 31, unless something in the UK changes. Some politicians say a further extension would require another EU referendum or a general election.

However, Johnson has claimed on the campaign trail that he'll take the UK out of the EU whatever the weather on October 31. In other words, if the EU doesn't agree to the changes he's pushing for, then a 'no deal' Brexit could then become his default stance. Economists and analysts say that would highly damaging for Pound Sterling.

"Betting markets are currently pricing in about a 30% chance of a 'no deal', compared with just 15% at the start of May," Dales writes. "Admittedly, investors’ demand for put options to protect themselves against further falls in the Pound is still relatively low by recent standards. But this is probably because the Pound has already fallen a long way. Given likely weak growth in the UK economy this year, we doubt that the Pound will recover much any time soon."

Above: Pound-to-Dollar rate at daily intervals alongside Pound-to-Euro rate (orange line, left axis).

Dales says the Pound is unlikely to recover by much anytime soon, even if a future Prime Minister Boris Johnson is in fact succesful in securing parliamentary votes for any kind of agreement that sees the UK exit the EU in an orderly manner.

This downbeat view is evidenced by Capital Economics' forecast for the Pound-to-Dollar rate to average its current level of 1.26 until the end of September. However, the London-based consultancy forecasts a near-5% increase in the Pound-to-Euro rate during the same time period.

This discrepancy is a result of the mire the Eurozone economy and European Central Bank (ECB) now find themselves in, following a year of trade conflict between the U.S. and China that has transcended continental boundaries and hurt the mighty Eurozone manufacturing sector.

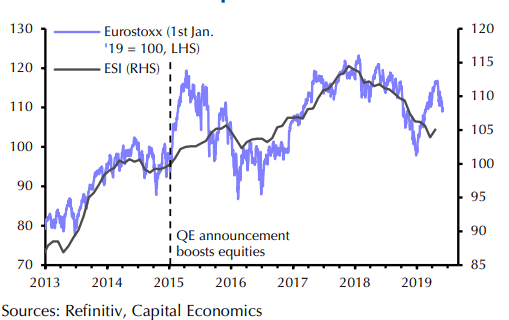

"Hopes that the slowdown in the euro-zone economy which began last year would prove to be a soft patch, driven by temporary factors, have now been dashed. Although first-quarter GDP growth was stronger than expected, most of the surveys and early hard data for Q2 have been disappointing," says Andrew Kenningham, chief European economist at Capital Economics. "Macroeconomic data have consistently undershot expectations since the start of 2018."

Above: Capital Economics graph showing Eurozone economic sentiment and Eurostoxx index.

Eurozone economic growth picked up from 0.2% to 0.4% in first-quarter of 2019 but surveys have since suggested strongly that the economy turned lower again at the start of the second quarter. Official data for the three months to the end of June won't be available until mid-August.

The early 2019 performance came hard on the heels of a disappointing 2018 year where GDP growth declined from 2.3% to 1.8%. Growth fell by half in the latter part of the year, with third quarter GDP growth declining from 0.4% to 0.1% and then coming in at only 0.2% in the final quarter.

As a result ECB officials have grown increasingly fearful that they will not be able to meet the inflation target of "close to but below 2%" at any point over the next five years after market expectations for consumer price pressures up ahead fell to a new post-2015 low.

"With the euro-zone and global economies continuing to disappoint, and inflation expectations having plummeted, ECB President Mario Draghi has made it clear that the Governing Council intends to loosen monetary policy again before long," Kenningham says. "In retrospect, the ECB’s decision to end QE last year looks like a mistake."

ECB President Mario Draghi said in June the bank will embark upon fresh interest rate cuts and another bond buying program if the inflation outlook does not improve. Since then financial markets have bet the ECB's deposit rate, which is the negative one of its three main interest rates, will be cut to a new record low in September.

However, what's gotten less attention by the market is the statement on bond buying, or quantitative easing, presumably because investors have long thought the ECB had already acquired about as much of the entire European bond market as it could prudently manage to buy.

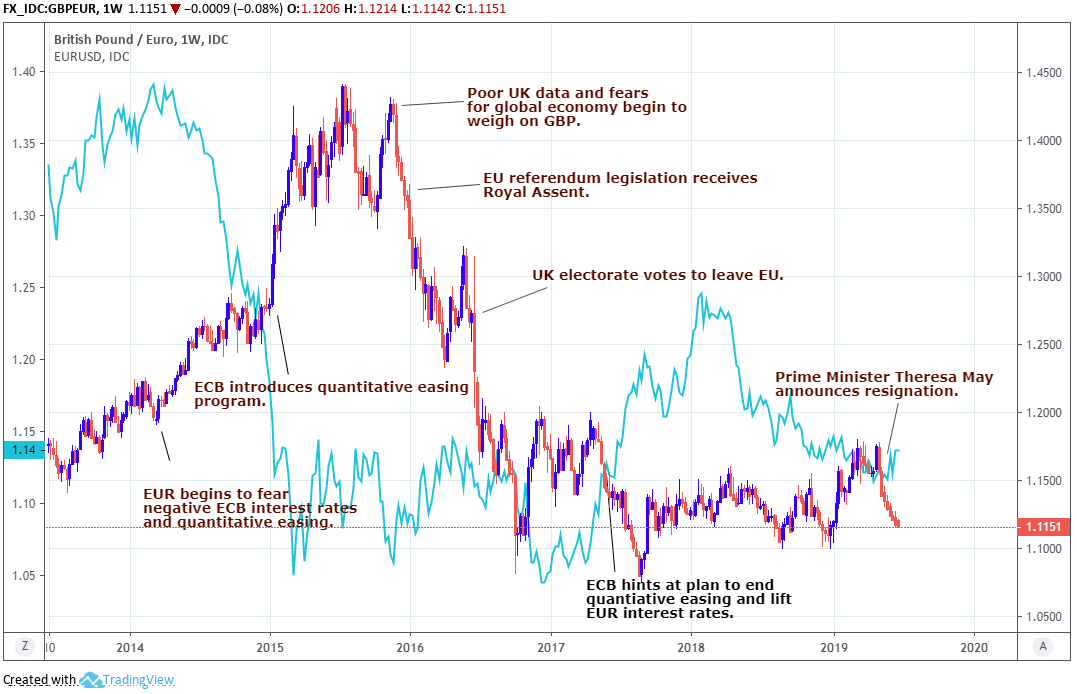

Above: Pound-to-Euro rate & Euro-to-Dollar rate (blue line, left axis). Annotated for 2015-2019 period.

QE saw the ECB buy European bonds en masse to incentivise borrowing by forcing down bond yields, which are market interest rates, between January 2015 and December 2018. The idea was that this would lift inflation toward the target of "close to but below 2%" by stimulating faster economic growth.

However, it's debatable whether the policy ever worked at all. Core inflation, which ignores volatile energy items because of their distorting impact on domestic inflation, was just 0.8% in June 2019 and only 20 basis points above the 0.6% rate that prevailed in January 2015 when the ECB first announced its controversial initiative.

"Given the limited scope to use forward guidance and interest rate cuts, the ECB is likely to resort to the most powerful tool in its toolkit: quantitative easing. We now think Mr Draghi will announce in October that the ECB will resume its net asset purchases, though the purchases themselves may begin in November," Kenningham forecasts.

Quantitative easing has the same effect on a currency as traditional interest rate cuts do, in that it lowers borrowings costs for governments, companies and consumers by forcing down the yields on their existing bond market debt.

Capital flows, which drive exchange rates, tend to move in the direction of the most advantageous or improving returns. A threat of lower yields normally sees investors driven out of and deterred away from a currency and vice versa.

Capital Economics forecasts the Pound-to-Euro rate will rise from 1.1150 Friday to average 1.17 throughout the final half of the year and in 2020. However, the Pound-to-Dollar rate is expected to average only its Friday level of 1.26 in the third quarter before rising substantially in 2020, to average 1.35 for the year.

The difference between forecasts for the two British exchange rates is explained by Capital Economics's projection for the Euro, particularly the Euro-to-Dollar rate, which is seen falling from near 1.14 Friday to average just 1.0769 during the summer months and into year-end.

Above: Pound-to-Dollar rate shown at weekly intervals.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement