UK GDP Growth Forecasts Upgraded at Standard Chartered

- Written by: Gary Howes

Image © Pound Sterling Live

A major UK-based bank has upgraded its UK growth forecasts following the sizeable revisions recently announced by the ONS and the economy's resilient performance in the first half of 2023.

Standard Chartered says a lower terminal rate at the Bank of England than was previously expected should also ameliorate growth headwinds in 2024.

"We previously anticipated a three-quarter recession beginning in Q4 this year, but that was predicated on the Bank of England taking the base rate to 5.75%. A terminal rate of just 5.25% (now our base case, supported by this week’s inflation and labour-market data) could be sufficient to avoid the onset of a technical recession," says Christopher Graham, an economist at Standard Chartered.

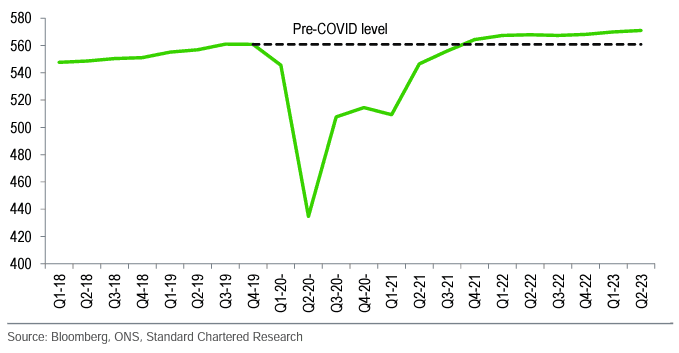

Above: UK real GDP, £BN. Image courtesy of Standard Chartered.

The Bank of England opted to maintain interest rates at 5.25% in September, and subsequent data has revealed wage increases are starting to decline and inflation is printing at levels below the Bank of England's forecasts released in August.

Standard Chartered nevertheless still expects UK GDP growth to stall through to mid-next year, as the lagged effects of previous monetary tightening continue to filter through to the real economy, and the government holds off from providing any fiscal support.

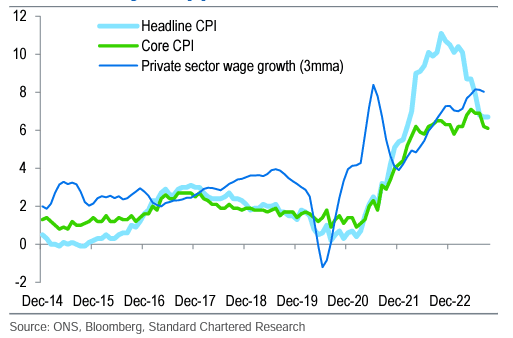

Above: UK CPI and wages, % y/y. Standard Chartered says the Bank of England has ended its rate hiking cycle as the key data heads in the right direction.

Economists at Standard Chartered expect the UK to record negative growth in the third quarter of 2023, with another potential negative quarter falling at some point in 2024.

"However, we think overall growth in 2024 is now likely to be flat (-0.4% previously)," says Graham.

Following the resilience seen in the first half of 2024 Standard Chartered raises its 2023 full-year growth forecast to 0.4% from 0.2% previously.

"A lower terminal rate feeds through to less of an impact on economic activity over the coming quarters. Moreover, with real wage growth turning positive and the labour market still tight by historic standards (notwithstanding recent signs of softening), consumer-spending tailwinds could be slightly stronger than previously envisaged," says Graham.