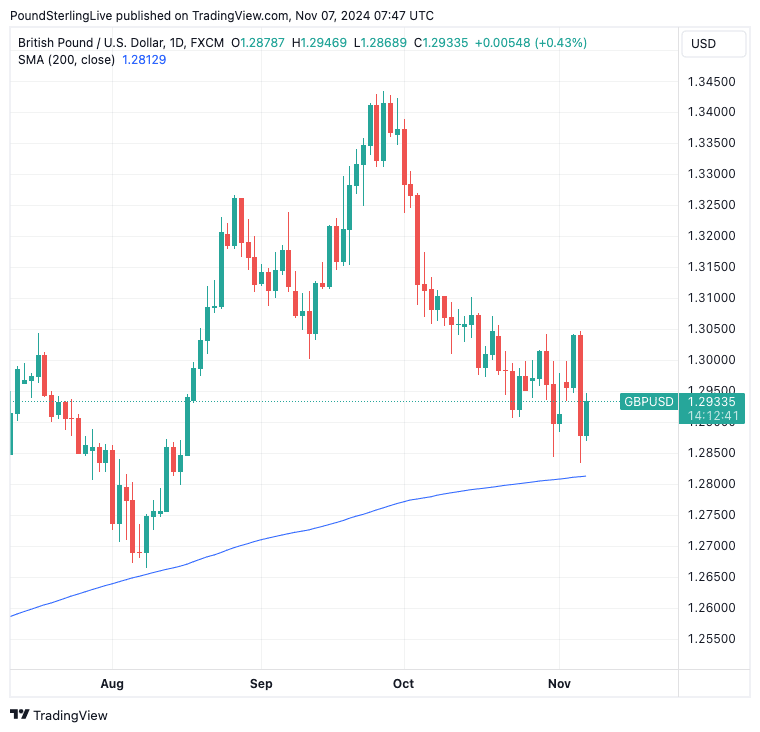

GBP/USD Recovering Post-election Result Losses

- Written by: Gary Howes

Above: Bank of England Governor Andrew Bailey delivers a post-MPC press conference in November. Image courtesy of the Bank of England, reproduced under CC licensing conditions.

Pound Sterling is stabilising against the Dollar, with the worst post-election predictions failing to materialise. Traders now have the Bank of England and Federal Reserve to contend with.

Another busy day awaits Dollar traders, with the Bank of England and Federal Reserve both likely to cut interest rates and address recent political developments.

The Pound to Dollar exchange rate (GBP/USD) slumped by 1.25% on the day it was announced Donald Trump had won the Presidential election and his Republican Party was 90% likely to take full control of Congress.

As the impact of the outcome - which markets weren't quite prepared for (a red sweep had an approximate 30% probability) - is digested, the losses have faded.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

At the time of writing Thursday, GBP/USD is back above 1.29 at 1.2935. The stabilisation means key support lines around 1.2813 have been defended, and a bigger post-election rout might have been avoided.

The market was swift to react to Trump's strong showing, but the lack of follow through confirms markets are entering a new phase.

"In reflection of the huge range of uncertainties, the USD’s rally is already showing signs of fatigue," says Jane Foley, Senior FX Strategist at Rabobank. "Overall, it is to too early to draw strong conclusions on the impact of Trump’s policies and this is resulting in a reluctance by investors to extend the USD's rally for the time being."

🎯 GBP/USD year-ahead forecast: Consensus targets from our survey of over 30 investment bank projections. Request your copy.

We know what Trump wants to do, but we don't know what he will do. He is notoriously unpredictable, a trait that he uses to his advantage on the global stage.

Economists observe Trump will want to negotiate on matters of trade, which means the worst-case scenarios that he threatened during the campaign might yet be avoided. These include a 60% tariff on all Chinese goods.

Markets will be alert to developments regarding the new administration and its prospective policies in the coming days, so we wouldn't say the dollar's ascent has ended just yet as it will be sensitive to headlines.

The next question for the Pound is how does the Bank of England react to recent events?

Interest rates will be cut by 25 basis points, as has been expected for some time. However, the Bank will need to decide whether to cut them again in December.

The new economic forecasts, which the Bank uses to guide market expectations, will provide some answers.

There will be some degree of uncertainty as to whether last week's budget decisions have been fully incorporated into the forecasts. In particular, we know growth will likely rise near term as the government's borrowing and spending spree juices the economy.

This will give reason for the Bank to strike a tone of caution, which can underpin the Pound.

The Office for Budget Responsibility released its forecasts alongside the budget last week, and these should offer some guidelines for what to expect from the Bank.

The OBR raised its inflation expectations, which, if repeated by the Bank, would amount to a 'hawkish' development for the Pound. It also raised growth projections for next year, although forecasts for the medium-term (through to 2029) were downgraded.

The tone of the Bank's guidance and Governor Bailey's post-decision interview will also be important for the Pound.

Expect Bailey to field questions about rising borrowing costs following the budget and Donald Trump's victory yesterday.

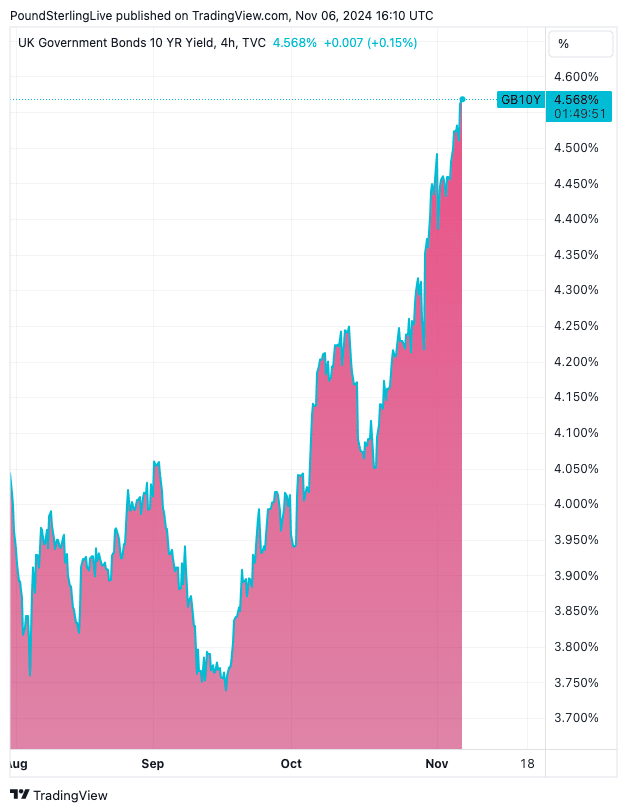

Above: UK ten-year bond yields have surged.

The Bank will have to be particularly cautious in this febrile environment, and loose lips could see the Pound punished.

The Federal Reserve will cut interest rates by 25 basis points, but again, the more pertinent question for markets is what happens in December and in 2025.

Already, we have seen expectations for a December rate cut recede, while a number of investment banks have cut their forecasts for the amount of easing to follow in 2025.

This is because they think a Trump administration offers inflationary policies, including tariffs and tax cuts.

With inflation still above the 2.0% target, the Fed must proceed cautiously.

According to the CME FedWatch Tool, the probability of a 25-basis-point rate cut in January, assuming a half-point cut this year, has declined from 69% a month ago to 32% today.

Economists at Nomura now expect just one Fed cut in 2025, with policy on hold until the realised inflation shock from tariffs has passed.

"We expect Trump to follow through on his campaign proposals to raise tariffs, leading to a significant near-term boost to inflation and modestly lower growth," says David Seif, an economist at Nomura. "We expect some additional easing in 2026 but have raised our terminal rate forecast to 3.625% from 3.125%."

Wells Fargo economists say they are reassessing their forecasts for the Federal Reserve's base rate in the wake of the election.

"The FOMC's reaction function likely would be more hawkish in response to higher inflation from tax cuts than from tariffs. Tighter monetary policy is an effective method for slowing demand growth, but it cannot do much to combat inflationary pressure from a supply shock such as tariffs," says Wells Fargo economist Jay Bryson.