Rising 'QE 2' Expectations Hammer Pound Sterling against the Euro and Dollar

- GBP in relentless selloff

- Bank of England tipped to restart quantitative easing

- BoE's Bailey promises prompt action to deal with crisis

Image © lazyllama, Adobe Stock

- Spot rates at time of writing: GBP/EUR: 1.0808, -1.75% | GBP/USD: 1.1852, -2.15%

- Bank transfer rates (indicative): GBP/EUR: 1.0520-1.0596 | GBP/USD: 1.1537-1.1620

- Specialist money transfer rates (indicative): GBP/EUR 1.0650-1.0701 | GBP/USD: 1.1650-1.1745 >> More details

The British Pound has suffered substantial losses in value against the Dollar, Euro and the majority of the world's major currencies amidst rising expectations that the Bank of England will introduce a fresh batch of quantitative easing to support the UK financial system in the near-future.

Analysts at Bank of America Merrill Lynch have told clients that Sterling is particularly vulnerable to quantitative easing, noting the currency fell substantially after the Bank of England first introduced quantitative easing in 2008 and we therefore expect some of the weakness seen in the currency of late is very likely tied to rising expections for so-called quantitative easing 2.

Quantitative easing involves the printing of money by a central bank which is then used to purchase financial assets such as debt issued by corporates and the government. The rising demand placed on these assets in turn lowers the yield those assets pay, which makes them less desirable to foreign investors who might have bought them in the past to earn a return.

Expectations for the Bank of England to engage in a new round of quantitative easing grew at the start of the week after the new Governor Andrew Bailey pledged "prompt action again" in order to try and shore up the UK economy and financial system in the face of the coronavirus outbreak.

The comments made by the Governor on Monday are being seen as a sign that the Bank could cut interest rates and deliver a fresh round of quantitative easing by March the 26 at the latest. "We now expect the BoE to cut Bank Rate to 0.10% at its policy meeting next week (if not before), and to announce a QE program somewhere in the range of £50-75bn, including some corporate bond purchases," says James Rossiter, Head of Global Macro Strategy at TD Securities in London.

The move could well provide markets with a shot of confidence, however from a foreign exchange market perspective, such actions could well prompt significant bouts of weakness in the Pound.

In anticipation of fresh action from the Bank, the Pound-to-Euro exchange has taken a hammering, falling to a new February low of 1.0933, which is 1.54% lower than where it opened the week.

We wrote on Monday that the downside pressures on Sterling could well see the currency match the Euro in terms of valuation, after surpassing the all-time low of 1.02 reached in late 2008, the last time global markets crashed and the world entered a deep recession.

The Pound-to-Dollar exchange rate is meanwhile taking an absolute beating at the time of this article's update in early afternoon London time; the pair has fallen to a new low of 1.2030, which is a 1.49% decline on Sunday's low. The exchange rate now actually looks poised to break below the lows it hit following the Brexit vote.

The Pound Suffers when Quantitative Easing is Unleashed

Expectations of another interest rate cut and additional stimulus measures at the Bank of England have risen amidst the ongoing meltdown in global markets as investors anticipate a significant slump in global economic activity.

But, interest rates at the Bank of England are already close to their rock-bottom level, known as the 'lower bound' in central banking language. The view is beyond this point further interest rate cuts achieve very little and in some cases could actually become damaging to the financial system as bank profitability plummets.

This suggests quantitative easing might be the only viable tool left available to the Bank of England to help stimulate a rapidly slowing economy.

"We expect the BoE to cut interest rates 15bp to their effective lower bound probably before their 26 March meeting, or otherwise at that meeting. With 10y yields 20-30bp above that lower bound, and the government potentially needing a much larger fiscal expansion, there may now be some point in gilt QE," says Robert Wood, UK Economist, Bank of America Merrill Lynch.

Gilt QE refers to the purchase of UK government debt - known as gilts - via the Bank of England's quantitative easing programme.

This is where the Bank creates money to buy government bonds, in doing so they inject cheap money into the economy which provides support in times of economic slowdowns and financial stresses.

Following the programme of quantitative easing announced in August 2016, purchases of government bonds now totals £435 billion.

Kamal Sharma, FX Strategist at Bank Bank of America Merrill Lynch says another round of quantitative easing at the Bank of England would present significant downside pressures on the value of the Pound.

"With Brexit having already compromised the UK's external trade position, the reintroduction of QE and the inevitable slide in UK yields will place further strains on the funding of the deficit," says Sharma.

The UK runs a sizeable and persistent current account deficit that ultimately stems from the country importing more than it exports. A sizeable portion of Sterling's longer-term valuation has therefore relied on the steady inflow of investment from foreigners who seek to take advantage of the UK's attractive investment climate.

However, this reliance on investor flows can become a source of weakness for Sterling when global investor sentiment is compromised, as is the case with the coronavirus outbreak.

Sunak announcement could have some bearing on #GBP - but given the scale of the momentum pushing against Sterling I doubt it will offer any fundamental re-evaluation of the currency's short-term direction. https://t.co/FD1La6Tf3Z

— Pound Sterling Live (@thepoundlive) March 17, 2020

Furthermore this demand by foreigners for UK assets can also fade if the returns on UK assets declines, this is where quantitative easing has an impact on the currency.

Quantitative easing at the Bank of England has the effect of making UK government debt - known as gilts - increasingly unattractive, as the yield paid on that debt is diminished.

This in turn has the effect of severely denting the kind of foreign investor demand the Pound depends on.

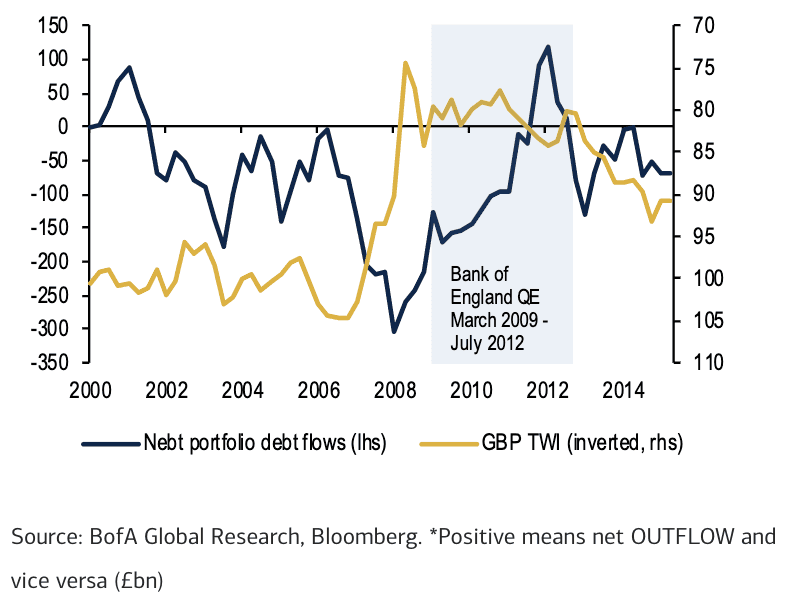

"Net portfolio turned precipitously through 2009 as it became clear that the Bank of England would start buying government debt. As a result, net portfolio debt flows posted outflows for the first time since 2001 (on a 4qtr rolling sum basis)," says Sharma.

"Though the move in GBP was well underway even for QE, it remained under pressure throughout that period. Resumption of QE therefore adds considerable downside risks to our GBP profile," says Sharma.

The commencement of another round of quantitative easing at the Bank of England would come in tandem with similar announcements made at other global central banks.

Over the weekend the U.S. Federal Reserve announced it would slash rates to what they considered to be the 'lower bound' at 0%-0.25%, but in addition there would be a fresh round of quantitative easing.

It also said it will buy at least $500 billion of Treasuries and $200 bn of agency mortgage-backed securities, without specifying a monthly quantum although if last week's announcement is anything to go by, that could be around $60bn

In response to the moves at the Fed, Bailey said in an interview given to the BBC:

"You saw some pretty big dislocations in financial markets last week, in particular in dollar financial markets which of course are global by nature.

"So the fact that the Fed, with the other central banks have extended swap lines so we can we can provide essentially three-month dollar money. Dollar money is a step forward.

"We're going to see how that how that works its way through the markets today in the coming days to see what the effect it has, but I would emphasise that this is strong coordination among central banks".

We would therefore not be surprised if the Bank of England followed in the footsteps of the Fed and announced further interest rate cuts and quantitative easing measures over coming days, certainly by March 26 at the latest.