Pound Sterling Relief as PMIs Beat Expectations

- Written by: Gary Howes

Image © Adobe Images

The British Pound extended gains against the Dollar and closed a deficit against the Euro after survey data showed the UK economy outperformed expectations in January.

S&P Global's Services PMI rose to 51.2 from 51.1 in January, defying expectations for a decline to 50.6. The Manufacturing PMI rose from 47 to 48.2, beating the consensus forecast of 47.1.

The Composite PMI, which merges the data to give a reading that better represents the wider economy, edged higher to 50.9 from 50.4, again beating estimates (50).

These data represent a welcome break from the seemingly endless slew of downbeat UK economic releases we have become accustomed to since mid-2024. This relief is reflected in higher GBP conversions:

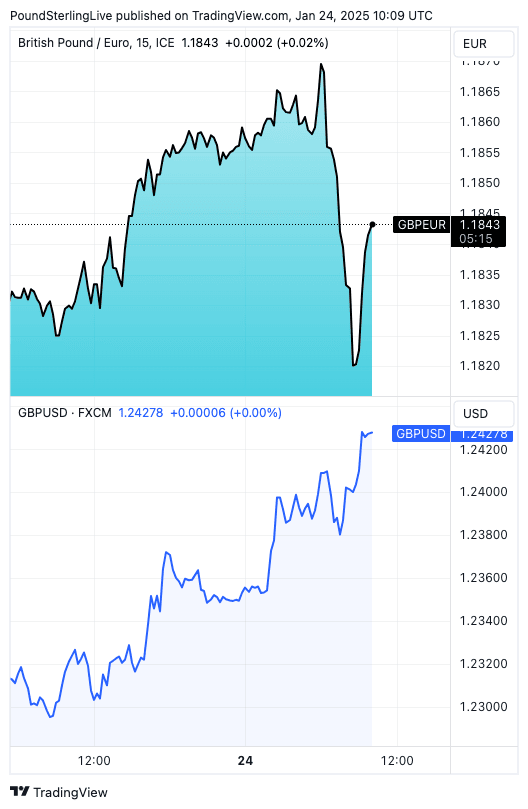

A multi-day recovery in the Pound to Dollar exchange rate accelerated to 1.2435 (+0.68%), and the Pound to Euro exchange rate recovered to 1.1839, having earlier fallen to 1.1815 following the release of the German PMI report that showed Europe's largest economy might have finally turned a corner.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

The PMI survey is by no means signalling the all-clear, as the important 'new work' component fell at its fastest rate since October 2023. Furthermore, employment levels decreased for a fourth consecutive month, with businesses blaming rising cost pressures.

These cost pressures will mount in April when taxes on employment are raised and minimum wage increases lift wage demands across the board.

Also, input price inflation increased, hinting at rising headline inflation rates in the coming months.

Above: GBP/EUR (top) and GBP/USD price action on Jan 24.

For the Bank of England, these data will do little to delay another interest rate cut in early February. What they will do, however, is ensure the Bank remains cautious about signalling it wants to accelerate the pace it cuts interest rates.

The market expects a similar outcome, which is why UK bond yields are higher, as is the Pound.

🎯 GBP/EUR year-ahead forecast: Consensus targets from our survey of over 30 investment bank projections. 📩 Request your copy.

Although the headlines present some relief, the underlying fundamentals remain soft.

Elias Hilmer, Assistant Economist at Capital Economics, says these data are still consistent with GDP stagnating at the start of Q1 after the economy lost all momentum at the end of last year.

"This suggests the risks to our forecast for GDP to grow by 0.4% q/q lie to the downside," he explains. "Today’s data release won’t alleviate the Bank’s concerns about the weakness of activity."

The Bank is expected to cut by 25 basis points in February, with the market anticipating just two more hikes in 2025.

Expectations for the future of UK interest rates remain the main driver of GBP behaviour, with the bout of recent weakness reflecting a rise in expectations for an acceleration in the pace of cuts.

This pricing can extend from here owing to signs of stagnation, which suggests periods of GBP strength might prove short-lived.