Bailey Trips Pound Sterling as he Signals the Hiking Season is Drawing to a Close

- Written by: Gary Howes

- GBP retreats on Bank of England Governor's speech

- Bailey 50/50 on need for further rate hikes

- Says decision rests on March data releases

- Denies GBP support from bond yield channel

- As ECB and Fed remain clear of need for further hikes

Above: File image of Andrew Bailey. Image: OeNB/Gruber. Sourced: Flickr: Reproduced under Creative Comments licensing conditions 2.0.

A sobering start to March for the British Pound served as a timely reminder that the politics surrounding Brexit is a minor issue for the currency and the economy and interest rate expectations are sat in the driver's seat.

The Pound is a laggard as March gets underway courtesy of comments from the Bank of England's Governor Andrew Bailey that poured cold water on investors' expectations for where interest rates in the UK are going.

Bailey indicated the prospect of a further rate hike is close to 50/50 and entirely dependent on data to be released ahead of the March 23 interest rate decision.

"It would be a brave person who put much faith in Andrew Bailey’s comments about UK interest rates, but his view that rates might not need to keep rising has put the FTSE 100 on top among global indices while seeing the pound drop back against the dollar and fall more dramatically against the euro," says Chris Beauchamp, chief market analyst at IG.

In a speech to the Brunswick Group's Cost of Living Conference, Bailey said "I would caution against suggesting either that we are done with increasing Bank Rate, or that we will inevitably need to do more."

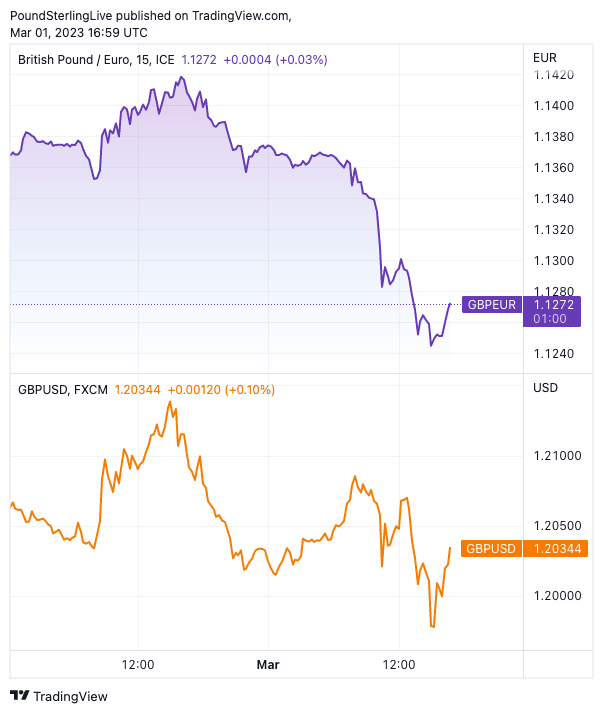

Above: GBP/EUR (top) and GBP/USD at 15 minute intervals showing the Pound's loss of altitude as March gets underway. Consider setting a free FX rate alert here to better time your payment requirements.)

He notes the economy is evolving as expected with inflation coming in slightly weaker and wages slightly stronger, "though I would emphasise ‘slightly’ in both cases". He then laid the prospect of a further hike in March firmly at the feet of the next labour market and inflation statistical releases:

"The incoming data will add to the overall picture of the economy and the outlook for inflation, and that will inform our policy decisions."

This is a central bank governor that is wavering between hiking again and squatting on current levels in Bank Rate.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

The ambiguity is at distinct odds with market expectations for the number of hikes that are yet as money market pricing reveals investors are priced for Bank Rate to peak at 4.75%.

This implies at least three further 25 basis point hikes before the current cycle is done.

Therefore, if the Bank is done with the hiking cycle, or delivers just one more hike, investors will be required to recalibrate expectations significantly.

Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics, says Andrew Bailey's speech challenges the consensus view that the MPC will hike by 25bp at each of its next three meetings.

A repricing lower of expectations could in turn prompt UK bond yields to underperform those in other locations, most notably the Eurozone, which has implications for the UK currency.

"Price action in gilts markedly diverged from that of USTs and Bunds as markets pared policy rate expectations for the BoE. The front end in the UK outperformed as the curve twist-steepened. Amid a decline in front-end UK real yields, GBP weakened on a broad basis," says Martin Tobias, Strategist at Morgan Stanley.

While the Bank of England is coy about the need for further rate hikes the European Central Bank is clear in its determination to keep pushing rates higher.

ECB rate hike expectations have risen again following this week's French, Spanish and German inflation readings that surprised to the upside as well as comments from ECB Governing Council member and head of the Bundesbank, Joachim Nagel, that further "significant" tightening may be needed beyond March and there were risks of an early slowdown in the rate hiking cycle.

Above: Germany's two-year bond yields have surged to levels last seen in 2008.

"In particular, GBP weakened against EUR amid comments from ECB Governing Council Member Nagel, who argued further “significant” rate steps may be needed beyond March and for a steeper pace of balance sheet reduction from July," says Tobias.

The developments in bond markets mean Eurozone bond yields have surged from their post-financial crisis lows and have closed the gap with UK yields.

This deprives the Pound of a source of support against the Euro it has relied on for years. "The narrowing of UK-EU rate differentials have contributed to the decline of GBP/EUR from €1.14 towards €1.12 this week," says George Vessey, FX and Macro Strategist at Convera.

The Pound to Euro exchange rate fell by nearly a percent to 1.1267 following the German inflation data and a rise in German bond yields to levels last seen in 2008.

The Federal Reserve's aggressive interest rate hiking cycle could meanwhile last longer than investors had previously expected.

The U.S. economy remains in robust form, meaning the peak in the Fed's interest rate hike cycle has been pushed back to a later date, offering the Dollar support and thwarting the GBP/USD's advance.

"Dollar sentiment received a shot in the arm in February when it appreciated nearly 3% against a basket of currencies and posted its first rise in five months. Hot data has been the dollar’s ticket higher as it led markets to price in U.S. interest rates peaking at higher levels around 5.4%, from about 4.6% currently, later this year," says Joe Manimbo, Senior Currency Analyst at Convera.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes