Australian Dollar’s Uptrend Tipped to Continue

Despite recent set-backs, the Australian Dollar's broad uptrend should ultimately remain in place.

Strategists at Nomura say weakness in the Australian Dollar represents a buying opportunity while the view is supported by economists at ANZ Bank who reckon the Reserve Bank of Australia will raise interest rate twice in 2018.

Currencies tend to appreciate on the promise of higher interest rates in the future as they offer foreign investors higher returns on their capital.

Yet in the short-term the outlook doesn’t look that great for the Aussie – the governor of the RBA was dispiriting in a recent speech where he appeared to pour cold water on any expectations for higher rates and placing the RBA aloof from the ‘herd’ of central banks pushing for higher rates and tighter policies.

But there are other near-term weights holding the Aussie down.

Nomura’s Peter Dragicevich notes the overstretched positioning in the currency futures markets.

This shows that a large number of funds are now holding large bets that the Aussie will rise, but that the market it overextended in favour of a rise, actually suggesting a greater chance the opposite will happen and the currency will revert back.

Dragicevich also mentions major trading partner China’s credit rating downgrade as a potential softener and the Fed’s hawkish stand at the last FOMC – all these factors are combining to weaken the currency in the short-term.

“In our view, this perfect storm is generating a short-term positioning adjustment in the AUD, but we do not think the broader trend has changed,” said the analyst.

“We think that dips in AUD/USD down towards 0.78-0.79 should remain supported,” added Dragicevich.

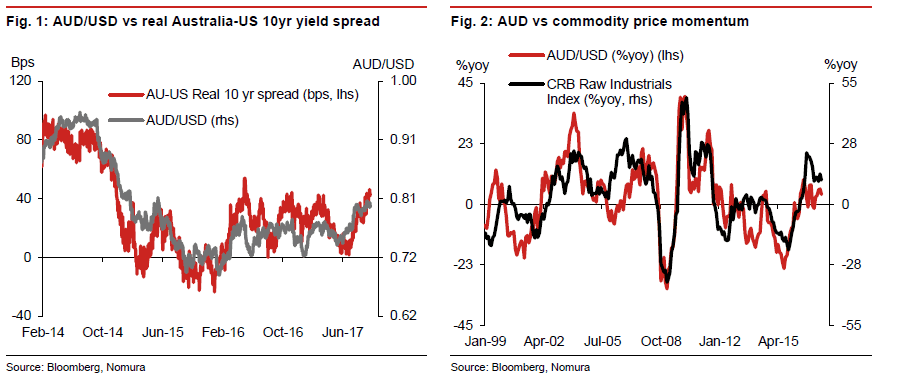

The 0.78-9 level is suggested by the signal from the current level in of the difference between the real Australian 10-year government bond yield over the US 10-year yield, since yields which reflect differences in countries interest rates are the main driving force behind currency valuations.

The “prevailing market sentiment” is that the RBA will begin turning the rate cycle higher in the new year and this should also support the Aussie as long as the fundamental backdrop improves.

Longer-term, the argument for the RBA raising rates - at least modestly - appears to be gaining momentum which is expected to provide support going forward.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

RBA to Raise Rates 0.50% in 2018

David Plank, economist with ANZ, thinks the RBA will raise interest rates twice in 2018 eyeing the high level of household debt in Australia. It is believed the moves will help discourage further borrowing and encourage saving.

A 0.50% rate rise will be tame enough to ensure endebted consumers are not pushed too hard on repayments.

To some extent this is the opposite of what others have been saying about the RBA, which they always thought was unlikely to raise rates specifically out of a fear of drowning borrowers by making repayments more difficult to honour.

Through analysing the statements of key RBA players, Plank comes to the conclusion that the central bank actually sees more of a risk of keeping interest rates low and allowing more cheap borrowing, which would store up risks for the future, than by raising them, which would disincentivize lending.

Plank says the current ‘neutral’ central bank lending rate is negative by which he means the official cash rate of 1.5% minus inflation, which is running at slightly over 2.0% depending on what gauge is used.

“Several problems spring to mind. First, we think a negative real cash rate will encourage a continued build-up in household debt. We don’t think macroprudential policy will be able to counter the impact of continued low rates. Indeed, one of the reasons we have revised up growth for 2018 is that we think the housing market (both construction activity and prices) is proving more resilient than we expected,” said Plank.

Further Plank sees an argument for the central bank overextending rates higher so as to build in a safety buffer in case the economy takes a dip in the future and policy rates have to be cut again.

In evidencing his view that the RBA is more likely to raise rates to stifle lending rather than cut them to ease the burden of existing debts, Plank notes the following:

“The Governor was more explicit in July when he said, in the context of leveraged household balance sheets, “that seeking a more rapid pick-up in inflation through yet further monetary stimulus was likely to add to the medium-term risks.””

Assistant Governor, Luci Ellis, also appears to back up the governor's view:

Elli said in a speech on 20 September that if “inflation remains low despite reasonable growth” then, “policy still needs to remain appropriately expansionary while avoiding further build-up of leverage and financial risk.”

Plank notes that the phrase “appropriately expansionary” means a higher rate than currently in place as it is effectively a negative cash rate.

“If growth is around trend and core inflation is close to 2% then we don’t think a negative cash rate is the appropriate policy setting. We think the RBA is moving in a direction consistent with our expectation of rate hikes in 2018,” says Plank.

The pace of rates may be cautious and slow, however, given the downside risks from imposing too much medicine on a highly indebted populace, too quickly:

"As a consequence, we think the tightening cycle, when it comes, will be very cautious,"says Plank.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.