GBP/NZD Rate Droops Over Inflation Data but Downside Limited

- Written by: James Skinner

"While annual headline inflation fell sharply, which is helpful for inflation expectations, the details suggest persistence in non-tradables inflation, with associated potential medium-term challenges" - ASB Bank.

Image © Adobe Stock

The Pound to New Zealand Dollar exchange rate drooped further from recent highs in midweek trade after Kiwi inflation converged with Reserve Bank of New Zealand (RBNZ) forecasts and UK inflation underwhelmed the economist consensus though there is reason for thinking GBP/NZD

Inflation fell further than was suggested as likely by the average of economist forecasts for the month of June on Wednesday when dipping from 8.7% to 7.9% in an undershoot of a consensus that had looked for a decline to only 8.2% for last month.

More importantly, the core inflation rate declined from 7.1% to 6.9% when it had been expected unchanged for the month and in what was the first sign of progress toward the 2% Bank of England (BoE) target since January, leaving Sterling swamped in losses but with GBP/NZD the least worst-performing exchange rate.

"A few more surprises to the downside like this and the 104bps priced by year-end will look more like 75bps for the BOE," says Jordan Rochester, a strategist at Nomura.

"I wonder if the downside momentum from goods (transport played a large role, but supply chains are looser I expect broad goods disinflation to come) leads to perhaps the idea of 75bps looking tough in two months’ time? Charts here suggest bigger falls in UK CPI to come perhaps 4% or even 2% with PPI's signal," he adds.

Above: GBP/NZD shown at 15-minute intervals alongside NZD/USD and EUR/NZD.

Financial markets had been looking for the Bank of England Bank Rate to be lifted from 5% in July to 6.25% by year-end ahead of Wednesday's release though the data places inflation on course to match BoE forecasts from May and a question mark over the widely assumed outlook for Bank Rate.

The BoE had suggested inflation would fall back to around 7% by the time data for July is released next month and Wednesday's figures indicated that is no longer such a far-flung prospect but for GBP/NZD, much about midweek price action also reflected the latest Kiwi inflation figures.

"While annual headline inflation fell sharply, which is helpful for inflation expectations, the details suggest persistence in non-tradables inflation, with associated potential medium-term challenges," says Miles Workman, a senior economist at ANZ, while warning that inflation risk remains tilted "firmly to the upside."

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

New Zealand inflation fell from 6.1% to 6% on an annual basis last month in what was an overshoot of the economist consensus for a fall to 5.9% but also an outcome that was slightly below the Reserve Bank of New Zealand forecast for the period, which envisaged a 6.1% annual rate.

Meanwhile, quarter-on-quarter inflation fell from 1.2% to 1.1% to undershoot a consensus that had looked for a decline to 1%, though this too matched the RBNZ forecast.

"The Reserve Bank of New Zealand (RBNZ) lifted the Official Cash Rate (OCR) to 5.5% in May and signalled it has most likely done enough to contain inflation. The RBNZ then held the OCR steady at its July meeting. ASB economists now see the current 5.5% OCR level as the peak for this cycle," says Chris Tennet-Brown, an economist at ASB.

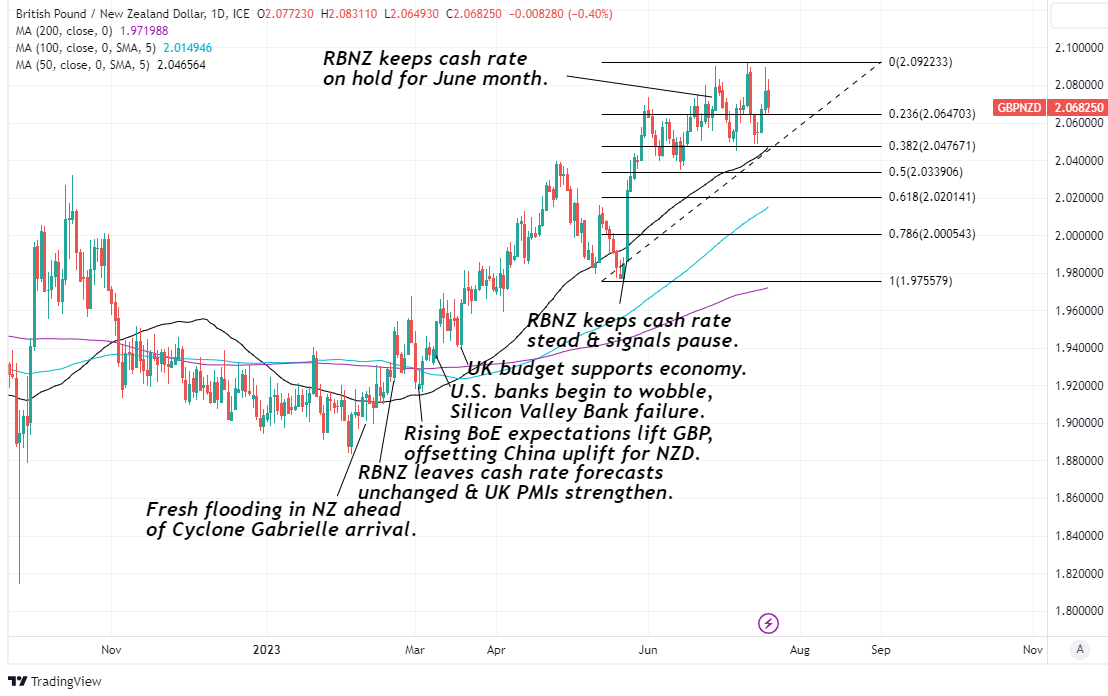

Above: Pound to New Zealand Dollar rate shown at daily intervals with Fibonacci retracements of May rally and selected moving averages indicating possible technical support levels.

"Mortgage rates have been rising, consistent with the Reserve Bank of New Zealand (RBNZ) progressively hiking the Official Cash Rate (OCR) since October 2021. Over 2023, the RBNZ has increased the OCR by another 125 basis points or 1.25%. However, over the same time, floating rates have risen by around half that amount. Shorter-term fixed rates have also lifted, but longer-term fixed rates have fallen," Workman adds.

The potential trouble for Sterling and the Kiwi is that moderating increases in prices of food and energy were among the largest contributors to declines inflation for both the UK and New Zealand in June, while statistical base effects also played a significant role in reducing the reported rates.

This indicates lingering upside risks for inflation in both countries and across both the overall and core measures, given recent rebounds in prices of commodities like crude oil and the tendency for core inflation to follow in the footsteps of overall inflation.

That and the recent resilience of both economies could mean there is a risk of inflation being further obstructed in its return to within the one-to-three percent target band over the coming months, though the extent of any obstruction and its implications for central bank interest rates both remain uncertain.

Meanwhile, the Pound to New Zealand Dollar rate has recently appeared to find technical support near and around the 2.0647 and 2.0476 levels but has struggled in attempts to recover above its early July high of 2.0922, while NZD/USD rallies have been curbed near 0.64 but with the supported near and around 0.62.

Above: NZD/USD shown at daily intervals with Fibonacci retracements of June rally and selected moving averages indicating possible areas of technical support.