Pound sees Scope for Further Gains against Euro and Dollar in Wake of Bank of England say Analysts

- Written by: Gary Howes

- GBP/USD upside remains favoured by analysts

- But GBP/EUR seen settling near current levels

- Markets 50-50 on a May rate hike

- April 18 labour market data is next hurdle

- April 19 inflation figures pose key risk

Image © Adobe Images

Pound Sterling held up relatively well in the wake of the Bank of England's latest interest rate hike and some analysts see the potential for gains ahead.

The Bank raised interest rates by 25 basis points, as expected, and said further rate hikes were conditional on incoming data, which echoes the message spelt out in February.

The biggest downside risk to the Pound was a scenario where the Bank raised interest rates but signalled it was now ready to pause, an outcome which would have inevitably prompted markets to aggressively bet on interest rate cuts later in the year.

This repricing was avoided by the Bank's decision to repeat February's guidance and Pound exchange rates were relatively well supported as a result.

A steady Pound made for a sharp contrast to previous policy decisions that were met with concerted selling pressure and provides a platform for further advances.

"Pound crosses rose across the board," says Fawad Razaqzada, analyst at City Index, in a comment following the Bank's decision.

The UK currency is now one of 2023's top performers and it entered Bank decision day with some wind in its sails.

"Sterling had also held its own better than some of the other currencies impacted by the troubles in the banking sector thanks to the perception that the UK’s financial services are better insulated from the crisis," says Razaqzada

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

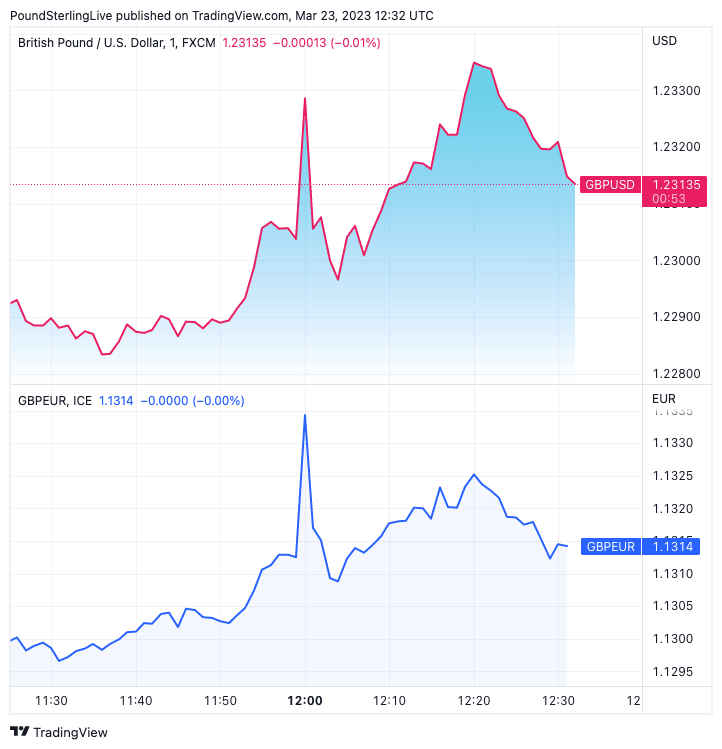

The Pound to Euro exchange rate is nevertheless lacking direction around 1.13 as the Bank of England's guidance was never going to be enough to match the European Central Bank's current guidance for at least another 50bp of hikes by mid-year.

The Pound to Dollar exchange rate is however looking more constructive at 1.2324 with markets sensing a series of rate cuts coming out of the U.S. by the second half of 2023 as something that might weigh on the Dollar.

"Given the broader weakening of the dollar after the FOMC we see scope for further gains in GBP/USD over the short-term," says Derek Halpenny, Head of Research, Global Markets EMEA at MUFG Bank Ltd, in a review of the BoE's decision.

Halpenny adds the Pound is becoming less volatile and this "could allow for the recent trend stronger to be sustained going forward."

Markets 50-50 on Whether the Bank Will Hike Again

With regards to the Pound's performance over the coming week, much depends on whether the Bank hikes again.

The rule of thumb is that further rate hikes will support UK bond yields and the Pound.

But, a pause could mean interest rates rise faster in the Eurozone and U.S., in turn supporting the Euro and Dollar relative to the Pound.

Above: GBP went higher in the wake of the Bank decision. Consider setting a free FX rate alert here to better time your payment requirements.

"Given that the BoE is likely to complete its tightening cycle before its peers (ECB, Fed), we maintain a Neutral GBP outlook," says David Alexander Meier, Economic Researcher at Julius Baer.

Following Thursday's announcement, markets were pricing in a further 31bp of Bank Rate increase by August, with a quarter-point hike expected by June.

This implies a near 50-50 split in odds for another hike to come in May.

Analysts are also Split: "Overkill" or an "Underlying Inflation Problem"?

This market split is reflected in the analyst community with the research notes and commentary landing on Pound Sterling Live's editorial desk revealing a clear split between those economists expecting another hike and those expecting a pause.

"We see an underlying inflation problem and still expect a final 25 basis point rate hike at the next meeting in May," says Bernd Weidensteiner

Senior Economist at Commerzbank.

"In one word: Overkill," is the assessment of the Bank's decision to hike coming from Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics.

"We see a strong case for expecting 4.25% to be the peak for Bank Rate. A plethora of indicators point to an imminent sharp fall in inflation," he adds.

Two Key Data Events for the Pound Now Loom

Which camp wins out will ultimately depend on how the incoming data prints as this will inform the next steps to be taken by the Bank of England and ECB.

Therefore, the Pound could enter a period of stable trade against the likes of the Euro as markets await April's run of data releases.

Key for GBP trade in the coming weeks will be the April 18 labour market report, where wage pressures will be watched closely.

Any pick up in unemployment or faster-than-expected retreat in wage increases would potentially see markets price out another hike.

The Pound could struggle under such a scenario.

The April 19 inflation release will then be the next release of consequence.

Markets will be particularly interested in inflation dynamics in the services sector.

The Bank on Thursday highlighted that services CPI inflation was 6.6% in February, which was 0.1% weaker than they had forecast in their February Monetary Policy Report.

"This has been one of the key indicators that core members have identified in recent communications as central to their thinking on the inflationary dynamics, with weaker-than-expected numbers implying faster-than-expected progress," says Nick Rees, FX Market Analyst at Monex Europe.

The market would likely lower expectations for another rate hike if headline inflation or a combination of services and core inflation come in below expectations.

This could set the Pound back in mid-April.

However, the Pound remains a currency that is trading with a more confident tone of late suggesting downside risks posed by the ending of the Bank's hiking cycle are greatly reduced when compared to previous months.

The 2023 lows against the Euro and Dollar are therefore likely to remain untouched.

On the upside, there is greater scope for gains against the Dollar than the Euro until such a time markets start becoming more convinced the ECB is approaching the end of its cycle.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks