British Pound Lags Behind at Year-end as U.S. Dollar Retains Top Spot

- Written by: James Skinner

Image © Adobe Stock

Pound Sterling ebbed further in the final session of a tumultuous year, leaving it trailing behind a majority of major currencies for 2022 while the U.S. Dollar and the Swiss Franc both remained top dogs for the period.

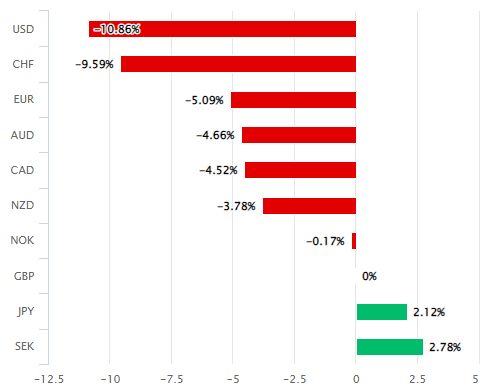

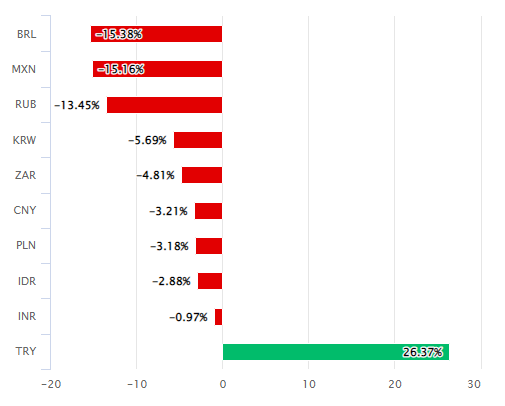

Sterling was holding intraday gains over the Dollar, Swiss Franc, Dollar-bloc currencies and South African Rand on Friday but continued to carry steep losses for the year against all but four currencies in the G20 grouping with only the Turkish Lira, Swedish Krona, and Japanese Yen faring worse.

"The Swiss franc has been eating away at the Dollar’s G10 lead in recent months but couldn’t quite overtake it. The US Dollar has run out of steam as the market has refused to price in the rate path the FOMC wants it to and is the weakest of the G10 currencies in Q4," says Kit Juckes, chief FX strategist at Societe Generale.

"The dollar has been helped by Fed tightening, a terms of trade shock from higher energy prices, insulation from the impact of both China’s zero-covid policy and Russia’s invasion of Ukraine, but as the year has drawn to a close, none of those factors is quite the driver it was in mid-2022," Juckes adds.

Above: Pound Sterling performance against G10 and G20 currencies for 2022. Source: Pound Sterling Live. If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.

Many factors have driven the Pound lower this year but it had been an outperformer among major currencies until shortly after the Russian military first crossed into Ukraine on February 24.

Since then symptoms of the war in Ukraine had added further to the losses sustained by the Pound including rising inflation, a deepening trade deficit, and a widening current account deficit.

However, analysts also say Sterling's poor condition is the result of the Bank of England (BoE) being too slow and cautious in raising Bank Rate to offset rising inflation at a time when other central banks have moved much faster.

"The rates market isn’t buying hawkish Fed rhetoric, isn’t put off (too much) by Covid infection levels in China, is hopeful that lower spot energy prices will persist for a while and most of all, is buying into the notion of a soft landing for the US and indeed most of the global economy," Juckes says on Friday.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of late September recovery indicating possible areas of technical support for Sterling while featured alongside GBP/EUR and GBP/CHF.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of late September recovery indicating possible areas of technical support for Sterling while featured alongside GBP/EUR and GBP/CHF.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

"The more you believe in China’s reopening, the more you may want to buy the Australian dollar. The more you want to believe in falling bond yields, the more you may want to buy the Japanese yen," Juckes adds.

One important question for next year is about how far and fast the economy can be expected to deteriorate with inflation at a double-digit percentage and interest rates being on course for a return to pre-2008 kinds of levels.

Already, the increase in the Bank Rate has been larger than anything seen since the 1980s and the period leading into what was a brutal recession, and the BoE's latest forecasts suggest a rerun of that kind of economic scenario is most likely for next year.

"GBP/USD has been far more tame and well contained within a range between 1.2100 and 1.2000," says Brad Bechtel, head of global FX at Jefferies.

"A move through 103.50 in DXY might just be enough to drag GBP/USD off the lows and back through 1.2100, but I get the impression we'll end up below 1.2000 pretty quick in this pair and EUR/GBP will be off to the races to the upside," he warns in a Friday market commentary.