Pound Sterling at Risk of Unravelling into Year-end as Economy Pales

- Written by: James Skinner

"If the 1.15-1.17 range in cable [GBP/USD] does materialize over the very near-term, we would currently view that range as decent short entry point. Our year-end target range for cable is 1.08-1.12," - BMO Capital Markets

Image © Adobe Images

The Pound has reversed all of its post-budget losses but some strategists say it could be likely to unravel again before year-end and have advocated that clients sell Sterling against the Dollar following any recovery back above 1.15, citing scope for it to fall as far back as 1.08 again in the months ahead.

Sterling rose against many currencies during the opening half of the week after the Conservative Party leadership selection process was resolved with a parliamentary coronation of former Chancellor Rishi Sunak as Prime Minister and as risk appetite appeared to improve on international markets.

Dollars were sold widely coming into the Wednesday session while stock indices climbed in global market developments that may have been the result of speculation about Federal Reserve (Fed) interest rates and a recently suspected intervention by the Japanese government to support the Yen.

The rub for the Pound is that none of this improves the gloomy outlook for the UK economy while risk appetite would evaporate promptly if the Fed confirms next Wednesday that its hawkish policy stance remains unchanged.

"We've had to tone down our expectations for the extent of that rally given the strength of the USD and general conditions surrounding risk appetite," says Stephen Gallo, European head of FX strategy at BMO Capital Markets, who had expected Sterling to rally following the Prime Ministerial selection process.

"If the 1.15-1.17 range in cable does materialize over the very near-term, we would currently view that range as decent short entry point. Our year-end target range for cable is 1.08-1.12," Gallo wrote in a Monday research briefing.

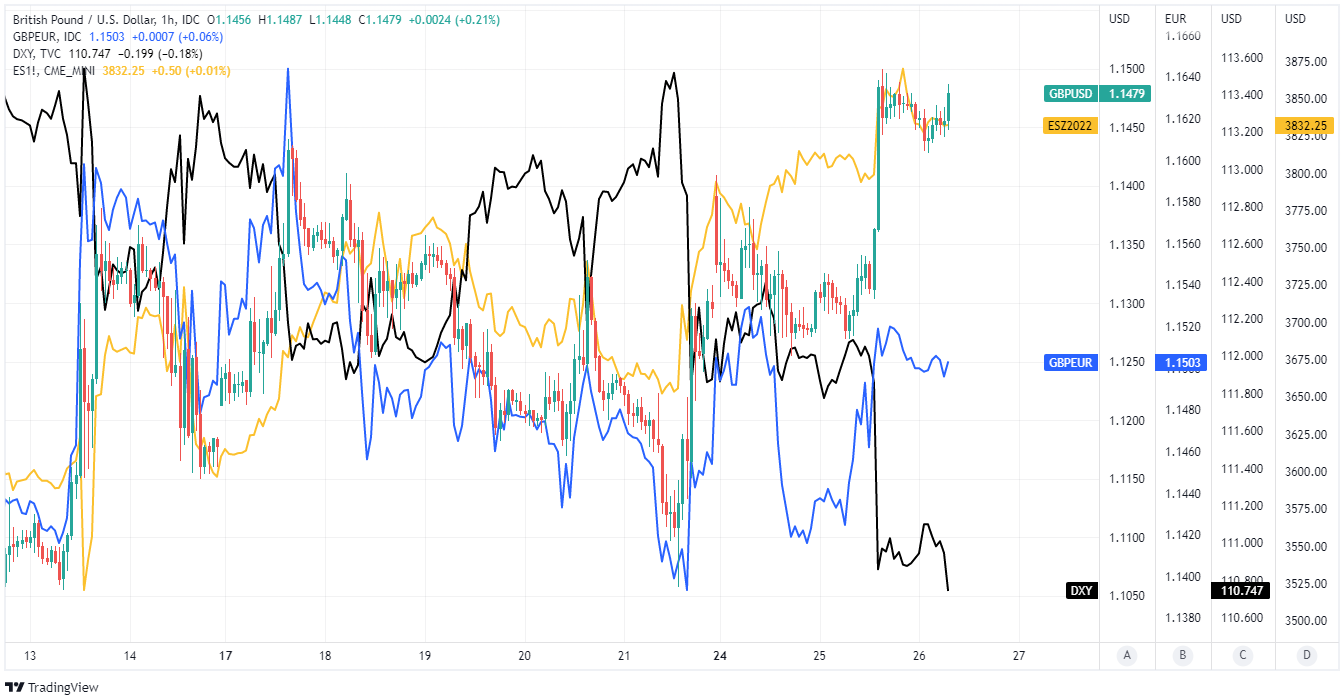

Above: Pound to Dollar rate shown at hourly intervals with Pound to Euro rate, S&P 500 stock index future (yellow) and Dollar Index (black). Click image for closer inspection.

Above: Pound to Dollar rate shown at hourly intervals with Pound to Euro rate, S&P 500 stock index future (yellow) and Dollar Index (black). Click image for closer inspection.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Gallo advocated on Monday that clients sell into any rally that takes the Pound-Dollar rate back up into the 1.15 to 1.17 range and look for a correction lower to play out over the final months of the year, a period in which the extent of the UK economy's ill health is likely to become clear in official statistics.

UK economic ailments could see the Bank of England have difficulty satisfying economist and market expectations for Bank Rate to reach almost four percent by year-end, meaning possible scope for a market disappointment that leaves Sterling especially susceptible to any continued Dollar rally.

"With Jeremy Hunt confirmed reappointed as Chancellor, we judge the political discount to GBP is fading. However, GBP retains a number of headwinds such as a looming recession and a growing current account deficit," says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

This is all after the UK's S&P Global PMI surveys suggested strongly on Monday that recessions in the manufacturing and services sectors deepened during October when the composite barometer of activity in both industries fell to a 21-month low for October

Monday's surveys were the latest in a growing list of indicators suggesting the UK economy is slowing faster than was expected by the BoE and other forecasters with recent retail sales, employment figures and GDP numbers featuring among the others.

Above: Pound to Dollar rate shown at daily intervals with Pound to Euro rate, S&P 500 stock index future (yellow) and Dollar Index (black). Click image for closer inspection.

Above: Pound to Dollar rate shown at daily intervals with Pound to Euro rate, S&P 500 stock index future (yellow) and Dollar Index (black). Click image for closer inspection.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Office for National Statistics data suggested last Friday that spending on the high street fell sharply during a September month for which unemployment claims were previously reported as rising at their fastest pace since the last period of 'lockdown.'

September's deepening downturn on the high street will complicate the economy's ability to rebound from a sharp 0.3% August decline in GDP revealed earlier this month, which itself left the economy with a steep uphill climb ahead to avoid an outright contraction for the third quarter.

However, with inflation also rising back to the double-digit percentages during September, many around the financial markets will still expect the BoE to continue lifting its interest rate aggressively in the months ahead.

"The UK's sovereign credit default swap has now recovered to pre 'fiscal event' levels, while gilt-bund spreads are now back near the 150bp levels seen in early September. The question is therefore whether sterling needs to rally much further.1.1500 is clearly a big level in GBP/USD," says Chris Turner, global head of markets and regional head of research for UK & CEE at ING.

"A break could see the correction extend to 1.1750. But such a correction would more likely be driven by a global re-assessment of risk ($ negative) than a further re-rating of UK prospects. The UK data calendar is light today, with some focus on whether the 31 October medium-term fiscal plan will be delayed a few days. 0.8650-08750 [GBP/EUR: 1.1428 to 1.1560] looks to be the EUR/GBP near-term trading range," Turner said on Wednesday.