Pound / Dollar Week Ahead Forecast: Defensive ahead of BoE and Fed

- Written by: Gary Howes

- GBP/USD retreats from last week's highs

- Technical studies shows 1.3852 as major resistance

- Bank of England to prove a key test for GBP

- But USD could yet wag GBP/USD

- Watch Fed meeting due on Weds

Image © Adobe Images

- GBP/USD reference rates at publication:

Spot: 1.3658 - High street bank rates (indicative band): 1.3280-1.3376

- Payment specialist rates (indicative band): 1.3535-1.3590

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

Pound Sterling has retraced from the peaks of its October rally against the Dollar and further losses are possible over coming days, particularly if the Bank of England disappoints markets by shying away from raising interest rates.

The Pound to Dollar exchange rate (GBP/USD) rose to a high of 1.3833 in the first half of the previous week before retreating sharply again on Friday, with a decent portion of that move being due to U.S. Dollar strength.

With this in mind, keep an eye on Wednesday's pivotal meeting of the Federal Reserve where it is expected an announcement will be made detailing the ending of its quantitative easing programme.

The Dollar surged in value in the final day of the week in response to some disappointing U.S. economic data, serving a reminder of just how crucial the Greenback is to not just GBP/USD but the broader FX market.

Technical studies suggest the balance of risks in the near-term (the period covering the next few days) are pointed lower.

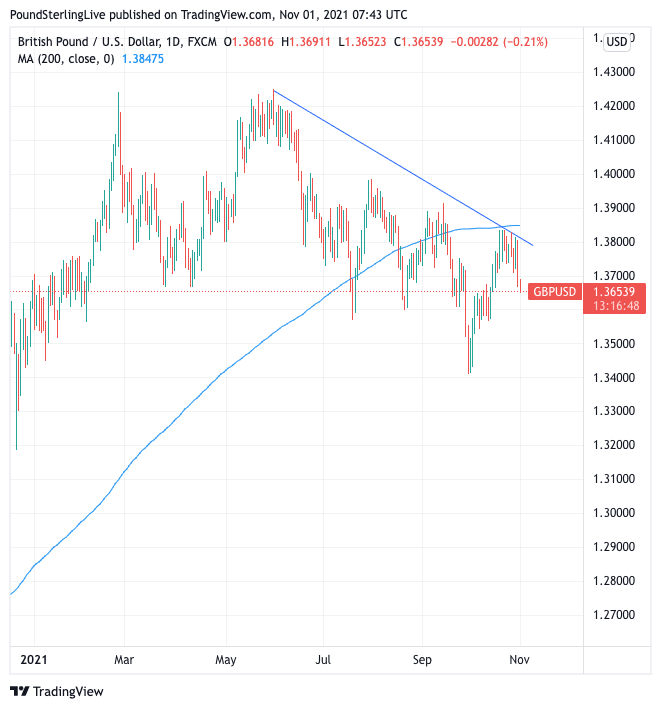

"GBP/USD spent last week consolidating below the 200-day ma at 1.3852. The market has failed here for now and even though the move lower appears to be corrective the market is on the defensive. Below the market we have 1.3569, the 12th October low ahead of the 1.3411 recent low," says Karen Jones, Team Head of FICC Technical Analysis Research at Commerzbank.

Above: GBP/USD daily chart showing influence of 200-day moving average. Also shown is downtrend line in place since May.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

Jones says a move above the 200 day moving average should see further gains to 1.3914, which is the mid-September high.

"Resistance at 1.3914 guards the more important 1.3984/1.4018 medium term pivot," says Jones.

Below the current market levels lies support at 1.3569, the 12th October low which falls ahead of the 1.3411 recent low.

"Dips are finding support at the 55-day ma 1.3716," says Jones.

Technical considerations will likely remain dominant through the first portion of the coming week and the potential for any substantive moves would likely only come in the wake of the Federal Reserve decision (Wednesday 18:00 GMT) and Bank of England policy decision, due Thursday mid-day.

The Bank could raise interest rates by 15 basis points, a decision that has been anticipated by investors for much of the past month according to money market pricing.

Faced with surging inflation members of the Bank's Monetary Policy Committee (MPC) have spoken about the need to raise rates in order to ensure inflation expectations amongst businesses and consumers do not start running higher.

The decision to raise rates would therefore be in keeping with the Bank's key role of guarding price stability in the economy.

It is however worth bearing in mind that the odds of a November hike have fallen over the duration of the last week while the odds of a December rise have increased, according to money market pricing:

The repricing in favour of a December rate hike over recent days might go some way in explaining why the Pound-Dollar exchange rate has lost some upside momentum.

"The probability of a November hike, which jumped to 100% following the hawkish turn by the BoE early this month and tough remarks by BoE Governor Andrey Bailey and other MPC members, has now converged with the probability of a move in December," says Roberto Mialich, a foreign exchange strategist at UniCredit.

Above: "A BOE RATE HIKE EITHER IN NOVEMBER OR DECEMBER IS EQUALLY PRICED INTO THE UK OIS CURVE" - UniCredit.

Waiting for December will be preferred by some members of the MPC as they will have received the full suite of official labour market data since the ending of the government's furlough scheme in September.

This will give policy makers a clue as to just how robust the labour market is and also suggests the November labour market report (due Nov. 16) could perhaps be the single most important event in the remainder of the year for Sterling.

A better than expected labour market report could give the MPC the cover required to move on rates in December, while a softer than expected outcome could provide enough hesitation to push any rate hike in 2022.

If the Bank forgoes a November rate rise the Pound could initially fall, but losses might prove shallow if the Bank offers guidance to suggest a December hike is likely - provided the November labour market report is strong.

Such guidance "could reduce the risk of some disappointment regarding the GBP," says Mialich.

But foreign exchange analysts at Goldman Sachs have told clients they are 'bearish' on the Pound's prospects in the near-term as the Bank of England will disappoint.

"The 'rubber meets the road' for the Bank of England, and markets have set a high bar for the MPC to deliver, essentially fully pricing a 15bp hike for this meeting and close to 60bp cumulatively through February," says Zach Pandl, an economist with Goldman Sachs.

The Wall Street bank says it will prove difficult for the Bank of England to significantly over-deliver at this point, and sets up room for disappointment if the MPC guides towards a more "measured" pace.

Such a "measured pace" would be a 15bp hike in November, followed by 25bp in February, which is Goldman Sachs' current expectation.

"This means that the risks are skewed towards GBP downside over the near term," says Pandl.

{wbamp-hide start}

{wbamp-hide end}{wbamp-show start}{wbamp-show end}

For the Dollar, the highlight of the week is the U.S. Federal Reserve announcement on monetary policy, due at 18:00 GMT on Wednesday November 03.

The Fed has signposted for some time now that it stands ready to reduce stimulus now that the economic recovery looks solid and inflation pressures are starting to rise noticeably.

Economists are looking for the Fed to reduce its monthly asset purchases by $15BN starting in November, with $10BN coming from Treasuries and $5BN coming from Mortgage-Backed Securities.

A move to reduce the scale of quantitative easing would be a necessary first step ahead of a 2022 rate rise.

It is arguably the timing of that first rise - and how many can be jammed into 2022 and 2023 - that will have the most impact on the market going forward.

Therefore it is the guidance on future policy as opposed to the actual decision to reduce quantitative easing that will matter for the Dollar midweek.

"A confirmation of market expectations may lead to a relief rally in the dollar, especially against lower yielding currencies such as EUR and JPY. However, any upside in the US dollar from a hawkish shift in the Fed is likely to be temporary," says Simon Harvey, Senior FX Market Analyst at Monex.

He says markets have already priced in a 'taper' that the Fed is still likely to lag other G10 central banks on raising interest rates due to their more tolerable inflation framework.

Recall, the Fed now targets labour market dynamics in addition to inflation, whereas the likes of the Bank of England are explicitly guided to ensure price stability.

"Sustained dollar downside is likely to be visible against currencies where hawkish adjustments to policy have been should the Fed not surprise with a more aggressive outlook for

normalisation," says Harvey.

This week should determine just how far the Bank of England and Fed are likely to diverge, offering the potential for decent volatility in the Pound-Dollar rate.