Canadian Dollar Underperformance Keeps Sterling in Contention for 2021's Top Spot

- Written by: James Skinner

- Lacklustre Loonie lifts GBP/CAD back into black for 2021

- Elevating GBP back to top spot among major currencies

- Election uncertainty possible culprit for underperformance

Image © Bank of Canada

- GBP/CAD reference rates at publication:

- Spot: 1.7394

- Bank transfer rates (indicative guide): 1.6784-1.6907

- Money transfer specialist rates (indicative): 1.7240-1.7300

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-to-Canadian Dollar rate rose above its breakeven level for 2021 in the penultimate session of the week, placing Sterling back in the top spot among the most frequently traded major currencies for the year owing to a nascent lacklustre performance by the Loonie.

Canada’s Dollar trailed other commodity currencies on Thursday including the Norwegian Krone, another oil-linked and equity-sensitive currency, as well as the Australian and New Zealand Dollars in continuation of a week-long trend toward underperformance.

The Pound-to-Canadian Dollar rate advanced back above 1.7380 on the interbank market throughout the Thursday session, its breakeven point for 2021 and a level above which Sterling becomes the best performing major currency in the G10 segment for the year.

“We do not expect the election to have much bearing on CAD which will be influenced more by BoC rate hike timing; the Fed’s timing on QE tapering; external market conditions in general and crude oil prices,” says Lee Hardman, a currency analyst at MUFG, who forecasts a GBP/CAD decline to 1.7150 by the end of September in response to an anticipated pick up in Canadian exchange rates.

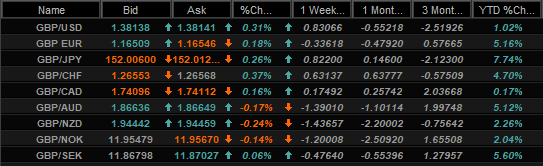

Above: Pound Sterling Vs G10 counterparts. Interbank exchange rate quotes and performances over various horizons. Source: Netdania Markets.

The Loonie’s nascent lag behind other comparable currencies is symptomatic of an emerging underperformance that predates Tuesday’s poorer-than-expected GDP data and so could have to do with mounting uncertainty about the outcome of the general election now looming in Canada.

“To say that federal Liberals are nervous might be an understatement, as Trudeau is trailing his main rival in popular support and is at risk of losing his government altogether,” Warren Lovely, chief rates and public sector strategist at National Bank of Canada Financial Markets.

“None of the major parties contesting the federal election are looking to make quick progress on the federal deficit,” Lovely adds.

It’s normal for currencies to trade at some modicum of a discount ahead of elections as a ‘risk premium’ is priced into them and other financial assets in order to reflect the resulting uncertainty about future government policies and the likely path of the economy.

The discount says at least as much about the increasingly uncertain nature of the election outcome in light of large shifts in opinion polls, as it does the policies of the incumbent Prime Minister Justin Trudeau and his challengers in the election.

![]()

Source: National Bank of Canada Financial Markets.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

While it’s possible that uncertainty relating to the September 20 election explains the Canadian Dollar’s lacklustre performance coming into September, many analysts both local and international are sceptical that it could have more than just a fleeting impact on the Loonie.

Furthermore, and once into the new week, market attention will turn quickly to the September policy announcement from the Bank of Canada scheduled for 15:00 on Wednesday, which will see policymakers weighing the possible implications of recent signs of a softening economic recovery against the risks of a longer-than-anticipated period of above-target inflation rate when determining any changes to the BoC’s policy outlook.

“We expect that the statement will show no major concerns on the impact of rising Covid cases on the Canadian economy given the vaccine penetration in the country. If the BoC does downplay the rise in Covid cases and the weakness in GDP as we expect, it would reinforce our view that the next reduction in the pace of asset purchases will likely come at the October meeting,” says Pablo Villanueva, an economist at UBS.

The BoC is in the process of winding down what was on some measures the most aggressive, crisis-inspired quantitative easing programme in the world and the currency market will be keen next Wednesday to hear of whether and when that process is likely to continue.

Above: Canadian Dollar Vs USD and shown at daily intervals, alongside NOK/USD, AUD/USD and NZD/USD.

{wbamp-hide start}

{wbamp-hide end}{wbamp-show start}{wbamp-show end}

Last time out the BoC reduced its weekly bond purchases from C$3BN per week to C$2BN in the third downward adjustment since November, leaving it on course to potentially end the programme around year-end or early in the New Year if the pace of tapering seen so far is sustained.

“The interest rate market is pricing in the start of the rate hiking cycle in the second half of 2022. This is already reflected in the Canadian dollar,” Georgette Boele, a senior FX strategist at ABN Amro.

The bank already cut its projection for Canada’s 2021 economic recovery last month, to 6% from 6.5% previously, and revised up its inflation forecasts right the way along the forecast horizon while saying nothing to encourage or discourage market speculation about a possible 2022 interest rate rise.

With investors anticipating the BoC will lift its interest rate around the middle of next year, many of them will hope the BoC stays its previously charted course and the Canadian Dollar itself could be vulnerable if the bank expresses concern about recent developments in the economic recovery.

The latter would be supportive of the Pound-to-Canadian Dollar rate.

Above: Pound-to-Canadian Dollar rate shown at daily intervals with 200-day moving average.