The Outlook for the Australian Dollar: Short Term Weak; Medium-Term Controversial

Most currencies will not be able to avoid a certain amount of weakness after the next meeting of the Federal Reserve on Wednesday, June 13.

There is now an almost 100% chance the Fed will increase interest rates, lifting the US base rate to 1.25% - currencies thrive on higher interest rates as they attract more capital, and so whilst a 0.25% rise is already priced in, most analysts still see scope for further USD gains after the announcement.

For AUD/USD the most important factor will be whether the Fed hints at more cuts or whether it takes its foot off the pedal.

Analysts seem mixed on this point, with the consensus appearing to reflect cautious optimism whilst a few, such as Société Générale’s Juckes adopt a more negative outlook, and see this as the beginning of the end for the Dollar – Juckes recently put out a note forecasting EUR/USD 1.20 by the end of the year, based as much on Dollar weakness as Euro strength.

Analysts of the Aussie Dollar, however, generally agree on a negative short-term trajectory for AUD as US and Aussie rate spreads narrow – Aussie rates remain stuck at 1.50%.

“We expect AUD/USD to decline further through 2017 on skinnier rate differentials and a weaker terms of trade profile,” said JP Morgan’s Meera Chandan and co.

Even Aussie bull Royce Mendes and team at CIBC economics are short-term bearish:

“As a result, beyond some near-term downside softness as US-Aussie rates spreads compress further, we expect AUD strength over the medium run.”

Whilst it is hard to argue rates will not narrow, what is more difficult is to assess the trajectory of growth.

J.P Morgan are naysayers pointing out how household earnings and consumption remain too poor to generate substantial growth.

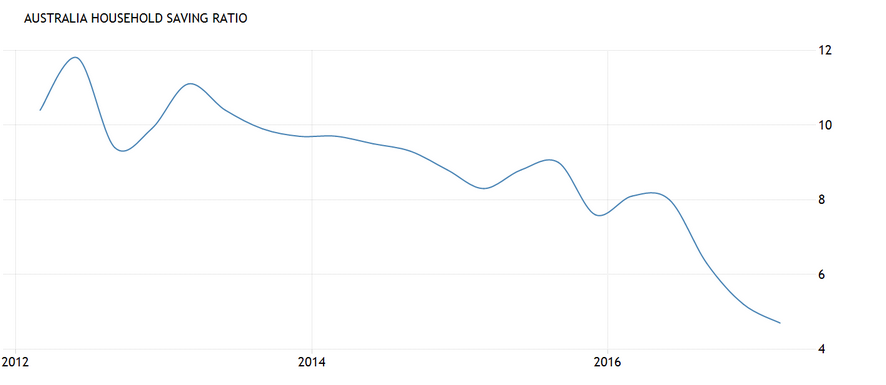

“Consumption growth is decelerating and the household savings rate is declining further. For the RBA, this makes the journey towards 3% growth even harder, especially given that expectations for 2Q growth are not especially optimistic.”

It is on this point that they part ways with more bullish CIBC.

“The rebound in household incomes, tied to healthy consumption, favours the view that monetary policy has reached a trough,” says the more optimistic Mendes.

Whilst this reflects the RBA’s upbeat 3.0% growth forecast for the year, the data is mixed, at best.

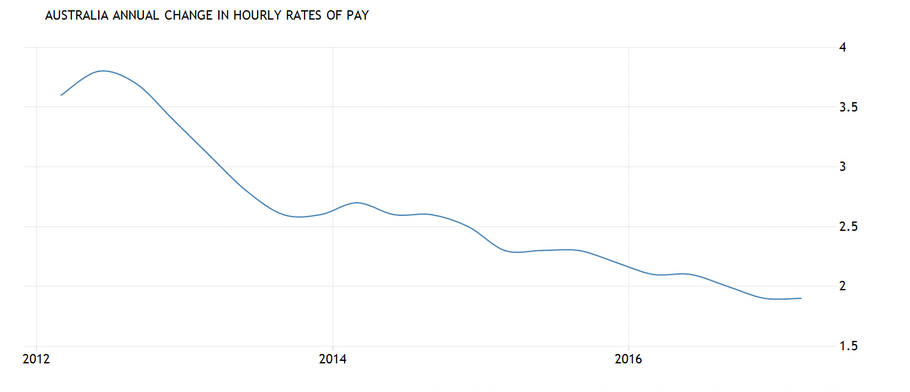

Wages remain soft, rising by a historically languid 1.6% in the last two quarters.

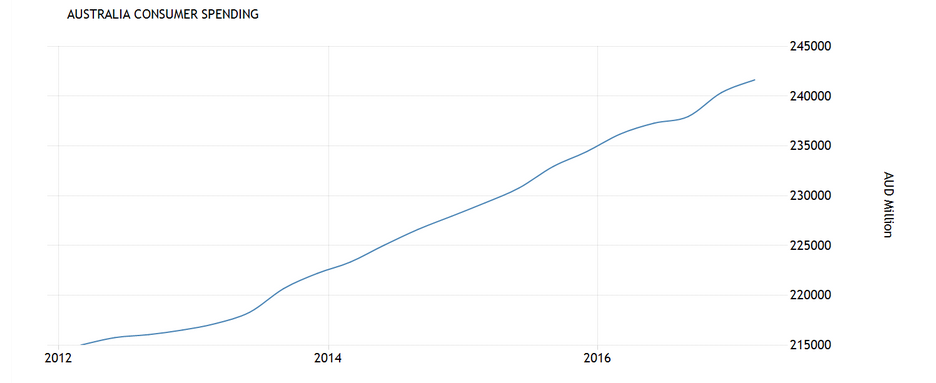

At the same time Consumer Spending does appear to be quite robust as it continues rising at about the same pace as before showing trenchant spending.

The lack of income coupled with high spending has resulted in a steep fall in savings which are now at new mega-lows.

The need to spend is also fuelling debt which continues to rise to levels which concern the RBA.

Was Q1 Growth Really that Bad?

Much of the debate around growth which dominates forecasts for the Australian Dollar has revolved around how bad growth was in Q1.

GDP rose 0.3%, which was lower the 1.1% of the previous quarter but not as bad as the -0.4% of Q3, and above consensus expectations of 0.2%.

As Mendes points out the country’s track record is strong:

“Although the rate of growth decelerated sharply in Q1, in part due to base effects, the economy has now avoided recession for 103 straight quarters.”

The stumble in Q1 was due to temporary distorters.

J P Morgan, are neutral, reiterating the Reserve Bank’s line, which explains the poor Q1 result on the weather, and sticks to its 3% story.

“The RBA continues to keep the faith in the 3% growth story for Australia. In its most recent communication, the RBA acknowledged the likely softness in 1Q GDP, but refrained from reading too much into a weak print,” they said, adding:

“As long as the RBA can attribute quarter-to-quarter volatility in GDP outcomes to unusual weather (higher than is usual rainfall in Eastern Australia in 1Q, Cyclone Debbie in 2Q), RBA neutrality is likely to persist for sometime yet. This suggests that domestic monetary policy is unlikely to provide much near term support for a lower AUD.”

The Outlook for Trade

A key determinant for the Aussie Dollar is the outlook for exports since strong demand for Australia’s exports has always been a key factor in currency supply and demand.

The data does not look good in Q1 on trade, but it will pick up, say CIBC.

“While net trade subtracted 0.7-ppts from Q1, the 0.3% QoQ advance was not as weak as some had feared. Furthermore, trade is set to become supportive, pointing to better growth ahead,” said Mendes.

Falling Iron Ore prices and vulnerability to a slowdown in China are central to J P Morgan’s less faltering assessment.

Chandan quotes the bank’s own commodity analysts who say iron ore prices are set to fall further, “Our resource analysts now expect iron ore to average USD67/t in 2017 (down from USD73/t prior), with a 4Q target of USD62/t,” she notes.

AUD does, however, continue to be supported by increasing demand for Aussie bonds.

The outlook for global growth is probably key in terms of assessing the trade growth potential, and here views diverge – although few talk about a negative outlook for global growth, and if anything, there seems a bias towards expecting the reflationary trend which started in late 2016 to continuing lifting global growth in the medium-term.

This may well offset any fragility in the Chinese market and support the AUD, from a trade perspective.

Cut, Standstill or Rise

There is a wide variation of opinions on the topic of what the RBA will do with interest rates.

The previously cut rates several times which have now reached record lows – have they done enough?

The overheating housing market was one reason not to expect further cuts as it was thought this would exacerbate things, however, since then the market has cooled, with the RBA stating in their June statement that house prices had cooled in Sydeny and Brisbane, the epicentres of the bubble.

Analysts at UBS also recently called a top:

"While the historical trigger for a housing downturn (of RBA hikes) is missing, mortgage rates are rising, and sentiment of home buying collapsed to a [near] record low," wrote Scott Haslem, George Tharenou and Jim Xu from UBS.

A top in housing appears to be a sign that interest rates might be about to start rising, thus exacerbating the housing downturn, but it could also be argued that the market might weather a cut better than previously expected.

J P Morgan think they will either cut them or remain unchanged, whilst CIBC expect a rate rise in early 2018.

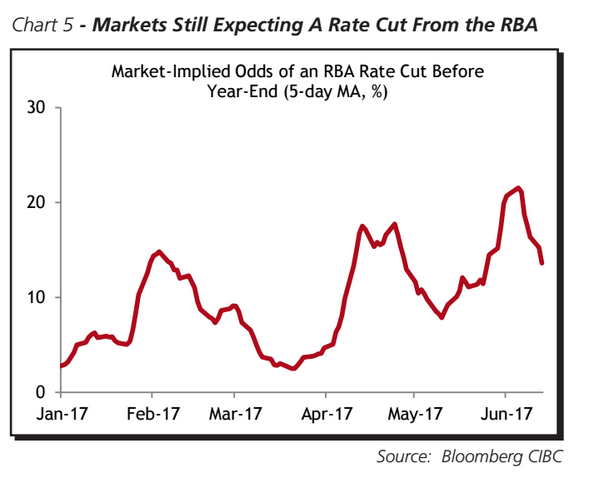

Markets, meanwhile, are still pricing in a greater chance of a rate cut, although this has fallen.

The key to the AUD and significantly AUD/USD may well be whether the macroeconomists are right about global growth, and whether the Dollar has in fact reached the summit of its third major rally in recent history.