Dollar Surges on Trifecta of Concerning U.S. Economic Data

- Written by: Sam Coventry

Credit : ILO/Apex Image. Source.

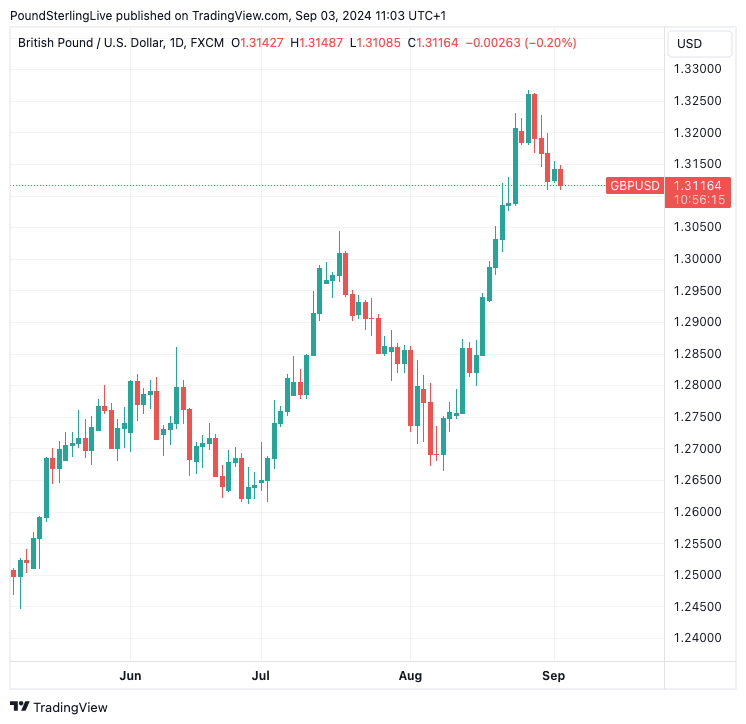

The Pound to Dollar exchange rate (GBP/USD) selloff gathered pace following the release of economic data that suggested the U.S. was entering a recession.

The Dollar was higher and stocks lower in a classic risk-off move after a survey of U.S. manufacturers showed the sector was slowing and price pressures were once again rising, creating a potential stagflationary macroeconomic setup.

"This morning has seen a trifecta of weak economic data. Aug. PMI & ISM manufacturing both came out even weaker than expected, while July construction spending unexpectedly fell. It's becoming clear the economy is entering a recession just as inflation is poised to turn higher," says Peter Schiff at Euro Pacific Asset Management.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

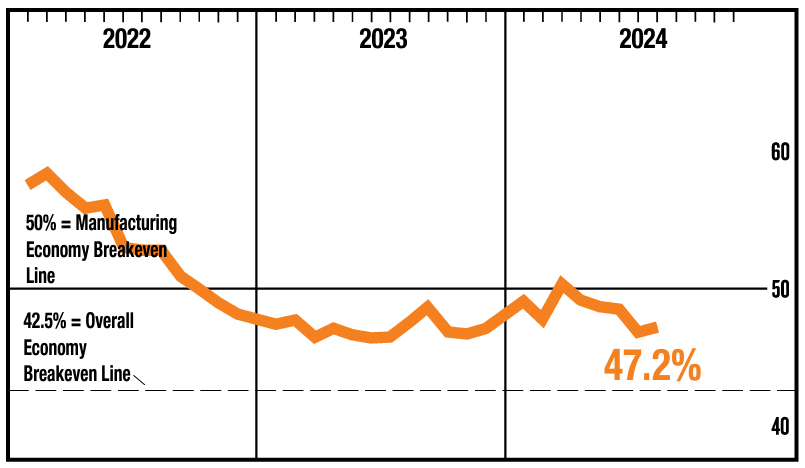

ISM's headline manufacturing PMI read at 47.2% in August, below expectations for 47.5. Anything below 50 signals contraction.

The prices paid component of the report was worrying, coming in at 54, which was well above 52.5 expected and July's 52.9. It suggests manufacturers are once again seeing inflationary pressures grow, which will raise fears the Federal Reserve can only deliver a limited amount of interest rate cuts.

The playbook says when data undershoots the odds of a Fed rate cut should rise, which is supportive of stocks and negative for the Dollar. But, this assumes inflation is falling too. When we throw rising inflation into a softening economy, alarm bells ring.

This explains why the Dollar rose, pushing GBP/USD to 1.03090 in the minutes following the release. The EUR/USD is down 0.20% at the time of writing at 1.1050.

S&P Global's PMI was also released alongside that from ISM, and it confirmed the sector is under pressure with a 47.9 print. The forward-looking new orders index of the report showed the situation was likely to deteriorate further, coming in at 44.6, down from 47.4 in July.

🎯 GBP/USD year-ahead forecast: Consensus targets from our survey of over 30 investment bank projections. Request your copy.

There was another poor data release in the form of construction spending which slumped with a -0.3% month-on-month print in July, well below the 0% expected. "The high interest rate environment continues to put downward pressure on construction spending," says Charlie Dougherty, Senior Economist at Wells Fargo. "Lower interest rates should eventually help bring about a turnaround."

The U.S. economy is slowing, but the market is worried the Fed will be constrained in any attempt to fix it with rate cuts for fear of boosting inflation just when it thought it was on the cusp of victory.

Above: The pullback in GBP/USD has further to run.

GBP/USD is now 1.12% off its August 27 peak of 1.3266 at 1.3116, with our Week Ahead Forecast noting that any disappointments in the data could extend the losses to 1.29 over the duration of September.

Ahead of the all-important U.S. labour market report, dollar trade will eye the ISM manufacturing PMI due on Tuesday, and the ISM services PMI on Thursday. Both will tell us how the U.S. economy fared in August.

"Currency volatility should pick up today as US markets re-open after the long Labour Day weekend and data releases take over. The big event of the day is the ISM manufacturing index in the US. Remember this has been in contraction territory (i.e. below 50) every month since October 2022, excluding a short-lived rebound in March this year," says Francesco Pesole, FX Strategist at ING Bank.

"The slack in the manufacturing sector has been priced in for a while, and we'll probably need to see a rather soft number to trigger recession alarms and drive the dollar materially lower," adds Pesole.

The Pound is 2024's best-performing major currency, driven primarily by robust domestic economic data and returning confidence in the UK economic outlook. This has lowered the need for the Bank of England to lower interest rates quickly, offering pound support via elevated interest rates relative to elsewhere.

“Resilient domestic demand, an economy that is performing better than expected and hopes for an improvement in relations with the European Union under a Labour government, along with Sterling’s undeniably attractive valuation, continue to buoy the British currency," says Enrique Díaz-Alvarez, Chief Economist at Ebury.

However, signs of doubt about the outlook could begin to creep in. We report today that UK business leaders turned more cautious in August as the new government signalled a raft of unsavoury policy measures that included reforms to workers' rights and taxes that would target investment.

The Institute of Directors survey of UK business leaders revealed the sharpest decline in business investment intentions since the beginning of the pandemic lockdowns. Headcount expectations also dropped 14 points, from +24 to +10 – this was likewise the sharpest fall since the first pandemic lockdown.

"The newsflow in recent weeks on employment rights and Autumn tax rises has dented confidence in the environment for business in the UK," says Anna Leach, Chief Economist at the Institute of Directors.

"Structural issues and fiscal headwinds suggest that the best of the recovery is over," says David Alexander Meier, an analyst at Julius Baer, in a monthly forecast update on the British Pound's prospects.

Should other surveys due later this month hint at fading sentiment, we would expect markets to price in weaker official data releases in the coming months, which would suggest the Bank of England needs to lend more support via weaker interest rates, in turn weighing on the Pound.