GBP/USD Week Ahead Forecast: Hawkish Fed, Cautious BoE Could Weigh

- Written by: James Skinner

- GBP/USD back near 2-year lows, risks further losses

- After U.S. CPI lifts USD & introduces further Fed risk

- Could see Fed signal faster climb toward neutral rate

- Leaves GBP/USD at risk without hawkish BoE offset

Image © Adobe Images

The Pound to Dollar exchange rate would risk further heavy losses in the days ahead without a ‘hawkish’ surprise from the Bank of England (BoE) or a possibly unlikely show of patience from the Federal Reserve (Fed).

Sterling opened the new week trading below 1.23 against the Dollar after slumping heavily on Friday when U.S. inflation figures warned that the path back to the Fed’s 2% target will likely involve a longer and more arduous journey than parts of the market had previously expected.

This is after the main inflation rate leapt by 1% in May and core inflation remained unchanged at 0.6% in month-on-month terms when it had been expected to ease lower to 0.5%, which could have implications for the extent to which the Fed lifts its interest rate this week and in the months ahead

“Inflation is far too high in major developed markets, and central banks need to tighten financial conditions to slow the economy down and lower inflation,” says Zach Pandl, co-head of global foreign exchange strategy at Goldman Sachs.

“At some point financial conditions will tighten enough and/or growth will weaken enough such that the Fed can pause from hiking. But we still seem far from that point, which suggests upside risks to bond yields, ongoing pressure on risky assets, and likely broad US Dollar strength,” Pandl also said on Friday.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of April 05 fall indicating possible areas of technical resistance for Sterling. Shown alongside spread or gap between 02-year GB and U.S. bond yields (orange), S&P 500 (black) and upside down Dollar-Renminbi rate.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of April 05 fall indicating possible areas of technical resistance for Sterling. Shown alongside spread or gap between 02-year GB and U.S. bond yields (orange), S&P 500 (black) and upside down Dollar-Renminbi rate.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Friday’s data triggered a surge in U.S. bond yields that lifted the Dollar and weighed heavily on stock markets across the globe as well as many other currencies, and was likely another watershed moment for Fed policymakers ahead of this Wednesday’s interest rate decision.

“The surge in short-term yields is fuelling a renewed tightening of financial conditions that will likely continue to provide support for the dollar next week with the FOMC meeting on Wednesday in focus,” says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

“Market participants will be watching closely for updated guidance over the path for further tightening. The updated dot plot could signal that the Fed plans to raise rates further above neutral territory in the coming years to combat upside inflation risks,” Halpenny and colleagues said on Friday.

Some Fed policymakers had suggested in recent weeks that they might feel comfortable slowing the pace at which they raise interest rates if the core inflation rate begins to come down convincingly Friday’s data made clear that this point is still some way off.

That in turn suggests the bank may have to do more with its interest rate than many have so far expected in order to return inflation to the 2% target.

“Inflation pressures in the US are likely to remain and the Fed is unlikely to turn materially dovish until rates are much closer to neutral or above in order to get inflation down,” says Jordan Rochester, a strategist at Nomura. “We remain short GBP/USD in spot (target 1.20).”

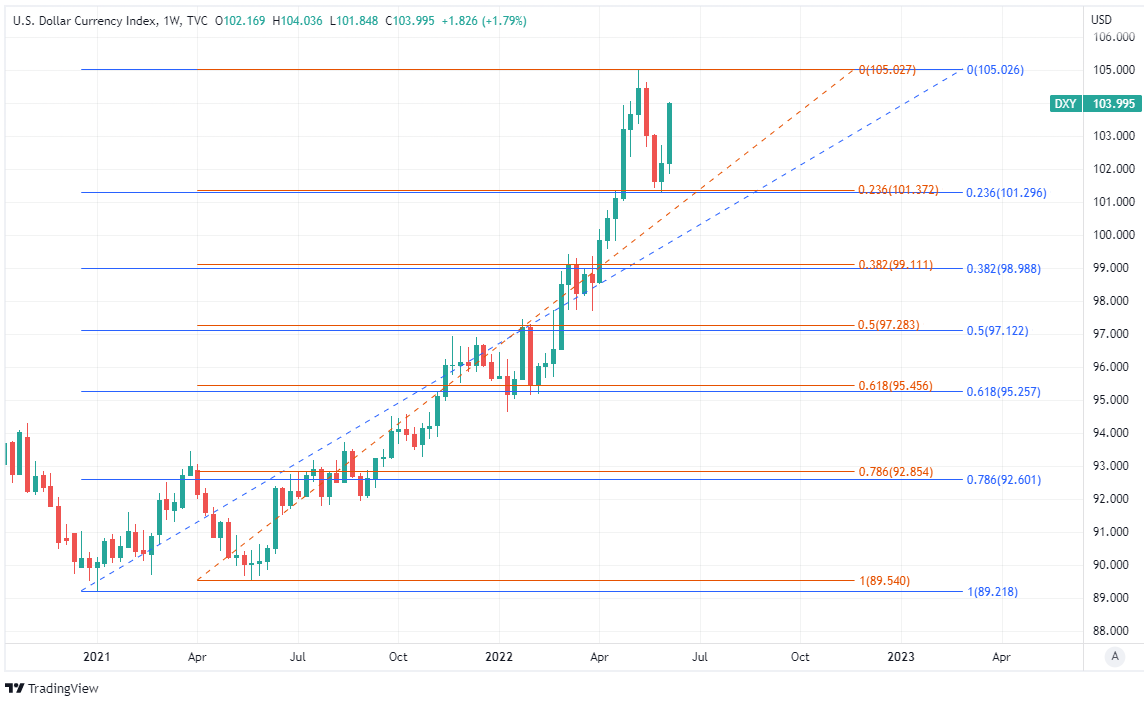

Above: U.S. Dollar Index shown at weekly intervals with Fibonacci retracements January and June 2021 uptrends indicating medium and long-term areas of technical support. Click image for closer inspection.

Above: U.S. Dollar Index shown at weekly intervals with Fibonacci retracements January and June 2021 uptrends indicating medium and long-term areas of technical support. Click image for closer inspection.

Last month's inflation developments could ultimately see the Fed continue lifting interest rates in larger than usual increments of 50 basis points throughout the remainder of the year, which would take the Fed Funds rate up to 3% or more.

“We think the FOMC now has good reason to surprise markets by hiking more aggressively than expected in June. Accordingly, we change our forecast to call for a 75bp hike,” says Jonathan Millar, deputy chief U.S. economist at Barclays.

This would be a significant risk for the Pound to Dollar rate in the week ahead and especially if the Bank of England continues warn on Thursday, as it did in May, that cost-of-living pressures would likely mean that it raises Bank Rate by less than markets currently expect for this year.

Much likely depends for Sterling on how the BoE interprets recent developments relating to UK inflation including the results of its own Inflation Attitudes Survey released on Friday, which showed expectations for inflation in the year ahead reaching a new record of 4.6% among the public in May.

“The BoE will need to incorporate the impact from more fiscal support from the government’s measures to ease households energy bills. Looser fiscal policy could reinforce inflation concerns and prompt more hawkish policy guidance. The likelihood of a larger 50bps hike has increased since 3 MPC members voted for it at the last meeting in May,” MUFG’s Halpenny said on Friday.

Above: Pound to Dollar rate shown at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of medium-term technical support for Sterling and resistance for the Dollar.

Above: Pound to Dollar rate shown at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of medium-term technical support for Sterling and resistance for the Dollar.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

All of this helps to explain why UK employment data will be scrutinised closely by the market on Tuesday as this could potentially impact the BoE’s policy stance if it confirms that UK wage packets continued to grow at a high single digit percentage pace of more than 7% in April.

Further strong pay growth could be interpreted by the BoE as an inflation risk and an argument for a faster increase in Bank Rate, especially in light of last Friday’s inflation attitudes survey, which showed households’ expectations for inflation in the year ahead reaching a new record high of 4.6% in May.

Most economists and analysts doubt the BoE will lift the Bank Rate by the same kind of 0.5% measure being taken at the Fed, however, and instead almost universally favour a smaller increase from 1% to 1.25%, which would likely leave the Pound-Dollar rate at risk of further losses this week.

“A panicky 50bp hike is neither likely at this meeting nor at those in the foreseeable future,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics, who sees Bank Rate rising only as far as 1.5% in 2022.

“The MPC has no more reason now than a month ago to be anxious about the medium-term outlook for domestically-generated inflation, which is its primary focus. Year-over-year growth in private-sector wages of 4.8% in March matched its forecast,” Tombs also said on Friday.