GBP/USD Week Ahead Forecast: Rebound Could Extend to 1.2662

- Written by: James Skinner

- GBP/USD rebound could extend as far as 1.2662

- UK economic figures balm for BoE policy outlook

- China story & RMB rebound also aiding GBP/USD

- But Fed policy still poses risk as PCE data looms

Image © Adobe Images

The Pound to Dollar rate has recovered sharply from two-year lows following a favourable turn in UK economic data and a rebound by a heavily sold Chinese Renminbi, which could potentially lift it further this week and may even prompt a test of technical resistance up near 1.2662 on the charts.

Pound Sterling opened the new week close to 1.25 after climbing from barely more than 1.22 last week and following a cacophony of supportive domestic and international developments including more favourable UK economic data and a softening of the U.S. Dollar.

Stronger-than-expected first quarter wage growth in the UK, strong April retail sales figures and a tentative ebb lower in all-important U.S. government bond yields have each either engineered or otherwise supported a favourable turn higher in the spread or gap between U.S. and UK yields.

But the rebound in the Pound-Dollar rate may also have been helped by the sharp bounce in Renminbi exchange rates given the extent to which both currencies were impacted in April when the Chinese currency slumped in response to the now-easing ‘lockdown’ in the world’s largest port city, Shanghai.

“Some support measures for the Chinese economy and some stability in the Chinese renminbi have helped usher in a period of consolidation in FX markets. This may well last into next week, although we would consider this a pause not a reversal in the dollar's bull trend,” says Chris Turner, global head of markets and regional head of research for UK & CEE at ING.

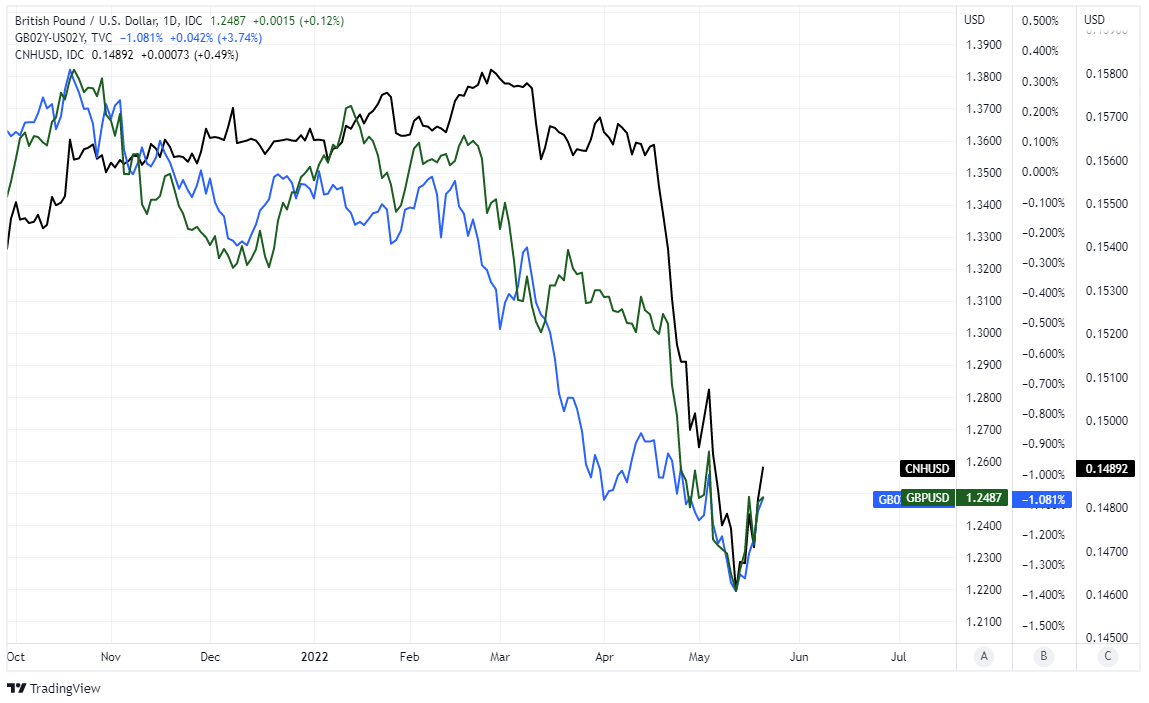

Above: Pound to Dollar rate shown alongside spread - or gap - between 02-year UK and U.S. government bond yields and Renminbi-Dollar rate. Click image for closer inspection.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Shanghai began a phased reopening from 'lockdown' last week, which could see China’s foreign trade and manufacturing activities normalise in June, while the Peoples’ Bank of China (PBoC) cut its mortgage-linked interest rates in order to support the domestic economy.

“The property sector accounts for 30% of the Chinese economy – so yes, this is a big deal and much needed given sagging private sector demand, falling prices and developer defaults. The 1-year LPR was likely left unchanged to not stoke further price pressures, but that’s the next domino to fall if things get worse,” says Bipan Rai, North American head of FX strategy at CIBC Capital Markets

“Much like the EUR, we have GBP/USD consolidating for now and expect sellers to emerge in the 1.2500-1.2650 area,” Rai also said on Friday. (Set your FX rate alert here).

To the extent that this places the Renminbi on a firmer footing in the week ahead, it could also potentially lift the Pound to Dollar rate further given that Sterling has had one of the stronger correlations with the Renminbi during recent months and fell even further than the Chinese currency during the weeks after the April 05 ‘lockdown’ of Shanghai.

For illustrative purposes, the author’s own calculations suggest that if the Renminbi was to retrace a full third of the losses sustained in that period, then Sterling and the Euro would likely reverse up to around half of their own respective declines from the same period.

Any such scenario would see USD/CNH easing lower to 6.67 while GBP/USD and EUR/USD reverse higher toward 1.2662 and 1.0670 respectively, although the rub for all of these currency pairs is that they still face risks associated with Federal Reserve (Fed) interest rate policy.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of February decline and various extensions thereof indicating likely areas of technical resistance for Sterling and support for the Dollar. Shown alongside inverted or upside down Dollar-Renminbi exchange rate and spread - or gap - between 02-year UK and U.S. government bond yields. Click image for closer inspection.

Fed policymakers including Chairman Jerome Powell have indicated repeatedly in May that the bank may be likely to lift the Fed Funds interest rate by a further 50 basis points at each of its next two meetings but did not rule in or out the idea of doing either more or less than that in subsequent months.

U.S. inflation outcomes will be instrumental in determining whether the Fed does eventually need to lift interest rates further than is commonly perceived as likely and this is a large part of why Friday's reading of the Core PCE Price Index for April will be important for the Dollar.

“We expect the April core PCE deflator to be noticeably softer than its CPI counterpart, with the core PCE up a "low" 0.3% (0.250% unrounded) versus a 0.6% gain in the core CPI. A realization of our forecast would pull down the year/year pace from 5.2% in March to 4.8% in April,” says Kevin Cummins, chief U.S. economist at Natwest Markets.

The Core PCE Price Index is the Fed's preferred measure of price pressures and so would do little to help the Dollar if it shows inflation ebbing in both month-on-month and year-on-year terms.

However the Pound-Dollarr ate is also likely to be responsive to remarks made by Bank of England Governor Andrew Bailey when he participates in a panel discussion titled "Monetary policy, policy interaction and inflation in a post-pandemic world with severe geopolitical tensions" at the Oesterreichische [Austrian] National Bank Annual Economic Conference at 17:15 on Monday, which is the domestic highlight of the week ahead for Sterling.

"We expect GBP/USD to lift a little this week if the flash estimates of the UK PMIs continue to show resilience (Tuesday). Both the March and April readings showed services and manufacturing expanded firmly. There is upside resistance for the GBP/USD near 1.2650," says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks