Dollar in Demand as Yields Rumble Again

Image © Adobe Images

- GBP/USD spot rate at publication: 1.3939

- Bank transfer rates (indicative guide): 1.3550-1.3647

- Transfer specialist rates (indicative): 1.3789-1.3839

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

An unexpected rise in the yield paid on U.S. ten-year bonds has hit market sentiment ahead of the weekend.

The Dollar was bid and stock markets fell as the headline U.S. ten-year Treasury note yielded 1.588%, a 2.94% rise on where it opened the day.

Rising yields in the U.S. have been a major source of strength for the Dollar in 2021 as foreign investors send capital into the U.S. to take advantage of the return they offer, thereby driving currency appreciation.

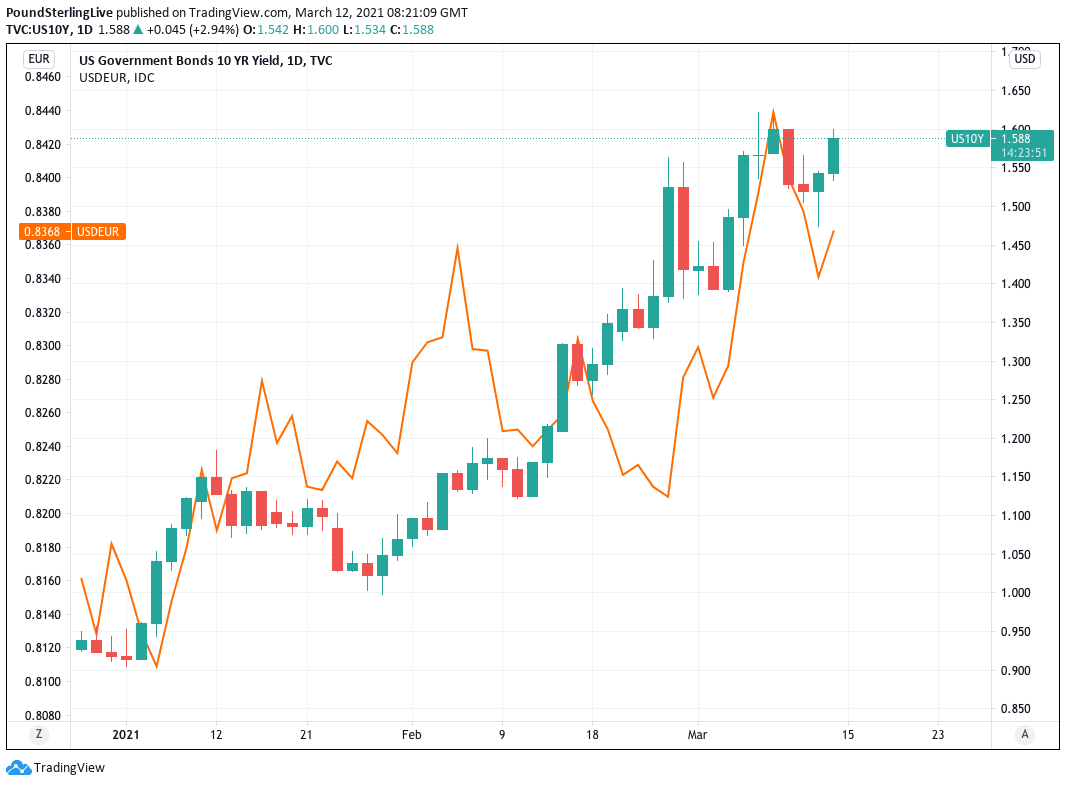

The below chart showing the rise in ten-year yields and the Dollar-vs-Euro rate attests to this:

Above: USD/EUR (left, orange) rises alongside U.S. ten-year yields (right, candles).

"We retain the view that upside risks for back-end UST yields," says Terence Wu, Treasury Research & Strategist at OCBC Bank. "UST yields moving onto a yet higher plane further consolidates the potential for a firmer USD in the medium term."

In the current environment, should yields keep rising then the Dollar will likely remain supported and stock markets under pressure.

"We're all bond traders these days, given how the fortunes of other asset classes are, at present, intrinsically linked with how government bonds – mainly Treasuries – trade on any given day. If yields rise, stocks generally face headwinds, and the dollar catches a bid," says Michael Brown, Senior Market Analyst at CaxtonFX.

The Euro-to-Dollar exchange rate is down 0.30% at 1.1945, the Pound-to-Dollar exchange rate is down a quarter of a percent at 1.3953.

Some financial commentators are questioning whether the spike in yields seen ahead of the weekend is a blip, noting that the ten-year briefly retreated below 1.50% this week as investors expressed relief at an unremarkable mid-week release of inflation data.

In addition, some well subscribed bond auctions out of the U.S. this week helped quell the rise in bonds.

"The 10Y and 30Y Treasury auctions were negotiated earlier this week without much fanfare, perhaps suggesting that the market is getting more comfortable with a higher UST yield environment," says Wu.

But was the dip in yields seen over recent days merely a retracement?

U.S. investors have sold bonds heavily of late as they anticipate greater inflation levels in the future owing to the reopening of the U.S. and global economy, a development that will only be stoked by the significant stimulus programme that will soon come into force in the U.S.

As investors dump bonds they demand that a higher yield is paid on the bonds they do buy in order to compensate for future inflation.

Rising yields in turn raise the cost of finance more broadly in the economy and act as a headwind to growth, hence the decline in stocks.

All eyes will now be on next week's Federal Reserve decision and whether policy makers will act in order to try and quell the rise in yields.

The Fed could make adjustments to its quantitative easing programme that sees it buys bonds to keep yields lower, however this will be a hard decision to sell if inflation is in fact expected to push materially higher in coming months.

While no change in policy is likely to be announced in March investors nevertheless fear that inflation will become a problem over coming months to the extent that it pushes the Fed into raising interest rates sooner than had been anticipated at the start of the year.

"Investors fear that the economy may be so strong that the Fed will have no choice but to tighten policy earlier than expected," says Matthew Hornbach, Global Head of Macro Strategy at Morgan Stanley.

Market prices imply the Fed will raise interest rates in January 2023, but the Federal Reserve's own guidance from December 2020 shows this to not be the case.

A revision of forecasts next week will therefore be crucial - will the Fed signal higher rates are indeed coming?

If so, the Dollar and bond yields could ride yet higher.

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |