Pound-Dollar Slips from Near Three Year Highs as New Brexit Risks Emerge

- Written by: James Skinner

- GBP slides to bottom of barrel on new EU negotiating deadline.

- As Sunday cut-off purports to threaten ratification of Brexit deal.

- GBP, market may underappreciate ratification risks from London.

Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3522

- Bank transfer rate (indicative guide): 1.3149-1.3243

- FX specialist providers (indicative guide): 1.3319-1.3427

- More information on FX specialist rates here

The Pound-Dollar rate ebbed from near three-year highs Friday as another deadline loomed in the Brexit process and fresh risks emerged to the market's resumed notion that a smooth exit from the transition awaits at year-end.

Pound Sterling was bottom of the major currency pile again for a second Friday on the bounce having outperformed through much of the week in anticipation of a UK-EU agreement which would give politicians, the market and wider world an opportunity to close the book that chronicles the Brexit Saga.

"Yesterday’s GBP performance was based on the nailed on certainty of a UK-EU deal being concluded imminently. By late last night that euphoria had leeched away to be replaced by a more jittery feeling. Result? GBP off almost 1% across the board. Where it has opened up this morning. The sense remains however that a deal of some sort will be done and will be announced in the next couple of days," says Humphrey Percy, CEO at SGM Foreign Exchange.

"Substantial progress" has been made in the negotiations, although not enough according to the latest update from Prime Minister Boris Johnson and European Commission chief Ursula von der Leyen, who're said to remain divided over fisheries and whether the EU's eagerly-awaited coronavirus recovery fund should be subject to the same rules around 'state aid' that may otherwise have been agreed between the two parties.

But another deadline now purports to loom over the Pound and wider process, also for a second Sunday on the trot, with Michel Barnier reiterating a European parliament demand for an agreement to be struck by then else its ratification be delayed until the New Year and after the December 31 expiry of the Brexit transition. Limbo in uncharted legal territory awaits in such circumstances and likely, a further retrenchment for a Pound that fell from first place for the week among majors to the third spot on Friday.

Pound Sterling would still have a long journey ahead to make it back to last Friday's levels, in the event that things truly do begin to go awry again.

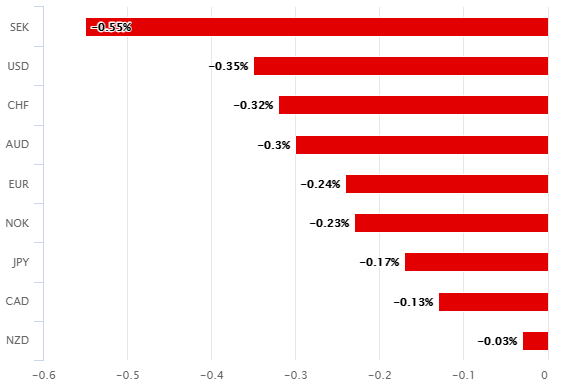

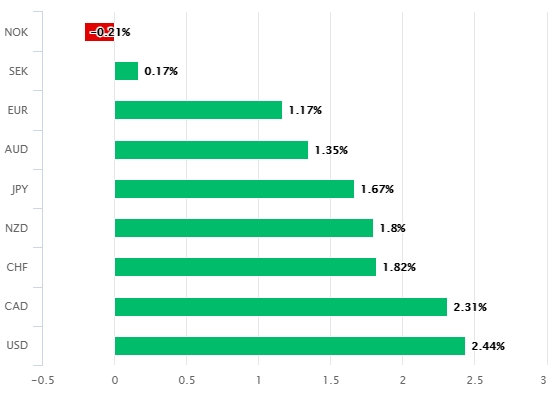

Above: Pound Sterling performance against major counterparts on Friday (left) and for the week (right).

"So far, their madman strategies have worked out reasonably well," says Michael Every, a strategist at Rabobank. "The UK government also believes that time is on their side, so even as the European Parliament stated that this Sunday will be the last possible moment for a deal if negotiators want it to be ratified before year-end, please keep in mind what happened to all the other deadlines. Let’s just hope they’ll get it done this time around."

Last week the two sides were deadlocked over new European demands for a so-called ratchet clause that would compel dynamic UK alignment with the ever-closer union's rules for an ever-expanding 'level playing field' on a range of matters that are said to be relevant for "open and fair competition."

This was after previously being at loggerheads over whether there would be any EU rulebook at all. Only time will tell whether and what compromises have been made, although with Sterling's slide inspired only by a new purported deadline on Friday, the market may be underappreciating the ratification risks that could yet emerge in the London's House of Commons.

"I think there has been a deliberate misunderstanding by the EU and its friends over what Brexit is about and what we need to do in order to achieve a proper Brexit. A proper Brexit is taking back control; it is recreating the sovereignty of the people of the United Kingdom through their Parliament," says John Redwood MP (Wokingham) (Con), speaking during a Tuesday House of Commons debate on the Taxation (Post-transition Period) Bill. "The EU has this idea that they can define and enforce a so called level playing field, though it usually looks more like a playing field that has been carefully prepared for the EU Home team to have an advantage."

Above: Pound-to-Dollar rate shown at daily intervals alongside Pound-to-Euro rate (black line, left axis).

Furthermore, the extent to which the Prime Minister appreciates these ratification risks could have significant bearing on the degree to which Sunday's deadline is overran, and so the performance of the Pound in the short-term.

There are two weeks on the clock before the end of the transition and the more of this time that can be taken up by domestic scrutiny of any agreement, the more likely it may be that ratification risks crystalise in London.

Redwood, who's often described by some as one of the Conservative Party's "hardline" MPs for his having been a stalwart and steward of the multi-decade campaign for UK independence, offers insight on the key faultlines.

"Some seem to think it strange this apparently technical middle order issue has got in the way. They misunderstand just what the EU thinks state aid amounts to, or how far they think the playing field turf extends. The EU has long argued that most policies have a bearing on their single market, and that many policies can therefore be a state aid," Redwood writes in a recent blog post. "Their single market stretches from trade policy to education and training, from employment policy to taxation, from energy to transport, from competition policy to digital policy. The market includes a heavily interventionist agricultural and fishing policy. Their idea of state aid goes well beyond the payment of grants to businesses to help them be more competitive. It encompasses taxes, both the lower variety to boost something and the higher variety to stop something or keep it out. It includes wages and minimum wage policy, social support, route licencing, farm subsidies, product specifications and much else. So when the EU says it needs to lock us in to prevent the UK gaining any competitive advantage from choosing better policies, it does so knowing that means wide ranging powers to limit the ability of the UK to govern itself."