Three More Months of Pain for the Pound: Intesa Sanpaolo

- Written by: Gary Howes

Pound Sterling is forecast to endure a period of weakness over the course of the next three months from where it should finally start to stage a meaningful recovery against the Euro and US Dollar.

The sudden slip in the Pound on Thursday, August 3 following the Bank of England’s super-Thursday event has shaken confidence towards Sterling and serves as a reminder that ultimately the exchange rate remains in a protracted downtrend.

We have reported over recent days that technical analysts - who identify trends in the market - are eyeing the next targets for GBP/EUR below the 1.10 level as precursor to yet further declines.

Meanwhile a number of fundamental analysts - those analysts that base their forecasts on economics, politics etc. - also appear to be intent on cutting their forecast targets in an environment of renewed Sterling weakness and ongoing Euro strength.

But it’s not all doom-and-gloom as the bottom is in sight.

Our latest collated forecasts for Sterling identify the next three months as potentially representing the nadir of the the currency.

The mean year-end target amongst the analyst community set at 1.12 in the Pound to Euro exchange rate and 1.28 in the Pound to Dollar exchange rate from where both exchange rates are seen rising.

“If data, and growth data in particular, do not disappoint, Sterling should remain well supported at close to GBP/USD 1.30 and 1.11 against the Euro,” says analyst Asmara Jamaleh, a foreign exchange analyst with Intesa Sanpaolo.

Jamaleh has updated clients with his latest views on Sterling and suggests that although a recovery is some on the horizon it would still be safer for those with an interest in GBP/EUR to prepare for an exchange rate that fluctuates between 1.1494 and 1.0990 over the next three months.

Look for GBP/USD to trade a range of 1.30-1.27.

“Downside risks to the baseline still prevail along all the forecasting horizon, due to uncertainty tied to Brexit,” says Jamaleh and “Risks to Sterling are skewed to the downside not only due to uncertainty over Brexit, but also to the trend of the EUR/USD.”

Jamaleh argues that forecasting the Pound in the one to three month timeframe is the hardest as this is the horizon on which uncertainty over Brexit will be at its highest, as talks with the EU will resume in the week of 28 August.

The programme provides for one-week negotiation rounds every month, whereas the next important EU summits on the Brussels agenda are to be held on 19 October and 14 December.

“Negotiations are unlikely to proceed smoothly, considering that the July round proved fruitless and highlighted the two sides’ strongly divergent views especially on the prickliest issue, namely the exit bill,” says Jamaleh.

By contrast, some progress was made on the front of the rights of EU citizens living in the United Kingdom and vice versa.

“The critical aspect lies not only in the difficulty in reaching an agreement on these themes, but also in the fact that success on this front is a preliminary, necessary condition, to start negotiations on the key issue at stake, i.e. the new framework of trade relations between the United Kingdom and the EU,” says Jamaleh.

Looking at the forecasts, GBP/USD is seen at 1.30 in one month, 1.27 in three months, 1.32 in six months and 1.33 in one year’s time.

The GBP/EUR is seen at 1.11 in one month, 1.0989 in three months, 1.1236 in six months and 1.1236 in twelve months.

So the dip has further to run ahead of a slow recovery.

Is the fall in value of Sterling impacting your international payments? Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Why the Euro Could Cool Down

The Euro / Dollar exchange rate has been move in an impressive uptrend for much of 2017 and has certainly put the Pound under pressure as EUR/GBP has tracked the headline rate higher.

As noted by Jamaleh noted, what EUR/USD does is also important for EUR/GBP and GBP/USD.

Further strength in this particular exchange rate could prove problematic for Sterling against the Euro but would see GBP/USD potentially enjoy further strength.

But it is therefore worth questioning just how long the Dollar will continue to struggle.

The Dollar’s day’s as top-dog do look to be over but there is also the sense that markets risk getting too negative on the currency - after all, the US Federal Reserve is in the midst of a cycle of interest rate rises and it does appear markets might have lost sight of this.

The Upside Risks for Sterling

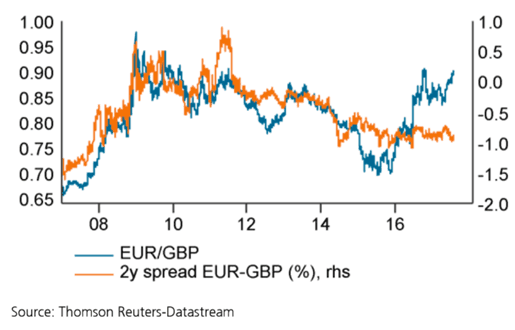

In favour of a stronger Pound, is the fact that the EUR/GBP exchange rate has risen well above the yield difference between the UK and Eurozone:

Note that such divergence typically gives way - the question arising is whether the yield differential goes higher to meet the exchange rate, or whether the exchange rate comes down.

A lot would need to happen for Eurozone yields to rise high enough to justify a move in spreads while a massive drop in UK yields also looks unlikely.

We are not convinced the Bank of England will turn negative enough for such an outcome; an indefinite hold of rates at current levels or another rate cut would be required to raise the spread.

Therefore if the yield differential looks unlikely to give, surely the exchange rate must move?

As Jamaleh notes, if data, and growth data in particular, do not disappoint, Sterling should remain well supported at close to GBP/USD 1.30 and 1.11 against the Euro.

Could data be where the Pound finds salvation?

Watch next week’s wage, employment and inflation data for clues.

We need wages to start rising, employment to continue falling and core inflation to rise for the Pound to give an upside surprise.

Bank of England Still in Play

The tenor of data will directly feed into policy moves at the Bank of England which in turn moves the exchange rate.

After the August Bank of England meeting meeting the market has pushed back by a quarter the expected timing of then initial rate hike.

At present, based on bank rate futures contracts, there is a probability of (just) over 50% of the first hiking coming in 2Q 2018, which increases to 65% in 4Q 2018.

“However, expectations for this year are also affecting the trend of the Pound,” notes Jamaleh.

After the August meeting, the probability of a rate hike already at the end of this year dropped from 42% to 32%, and was higher than 50% between the end of June and the beginning of July, i.e. after news broke that at the June meeting three BoE Board members out of eight had voted in favour of an immediate hike.

Only two members of the Committee voted for a rate rise in August but the opinion of these members an immediate hike would simply represent a removal of the additional stimulus injected in August last year – when rates were cut from 0.50% to 0.25% on the outcome of the Brexit referendum.

This argument could well be accepted by other members in the future: the UK could raise rates, defend the value of the Pound and therefore contain the overshooting of inflation, while still keeping monetary conditions markedly accommodative.

“A very similar argument had been used by Haldane – who has hitherto voted to keep stable rates – in a speech delivered in June, in which he explained that this could prompt him to change his stance and vote for a hike towards the end of the year, barring negative developments in terms of data releases and on the Brexit front,” says Jamaleh.

The analyst adds that while chances of an initial lending rate hike this year are slim, he believes the BoE will keep its options open, if two conditions should simultaneously fall into place: a favourable evolution of Brexit talks, and no disappointments from growth data.

Rhys Herbert, Senior Economist, Commercial Banking at Lloyds Bank notes that it might not take a lot to shift the MPC in a pro-Sterling direction.

The MPC lowered modestly its GDP forecasts for this year and next and made a

more substantial reduction in its forecast for wage growth in 2018.

“However, it still expects wage growth to pick up and inflation to remain above target throughout its two-year forecast horizon. What this actually means is that the debate about UK monetary policy is still finely balanced,” says Herbert.

Indeed, comments from BoE Deputy Governor Broadbent the day after the announcement suggested that it may not take much to sway him towards raising interest rates

This echoes the comments made by Haldane who has already indicated he may soon vote for an increase; “the rate-setting set committee could still be persuaded to hike rates late this year or early next,” says Herbert.