Pound Sterling: Barclays, Goldman Sachs Predictions ahead of Bank of England Rate Hike

- Written by: Gary Howes

- GBP firms ahead of Bank of England decision

- Barclays sees prospect of a decline Thursday

- Goldman Sachs sees GBP/EUR remaining supported

Image © Adobe Images

Foreign exchange analysts at Barclays say the British Pound will likely head lower following Thursday's Bank of England update, however Goldman Sachs is more constructive on the UK currency's prospects, particularly against the Euro.

The Bank of England's Monetary Policy Committee is expected to announce another interest rate rise before releasing its latest inflation and economic growth forecasts.

The Pound has firmed against both the Euro and U.S. Dollar through the latter part of July and early August and the currency's big test comes with the size of the hike announced and the shape of those forecasts.

Pound Sterling Live has already noted the largest downside risk to the Pound comes in the form of the Bank underwhelming against market expectations by delivering another 25 basis point hike.

This is because the market is now nearly fully 'priced' for a 50bp hike, based on various comments from MPC members and the June statement that it was now prepared to act "forcefully" in order to get a grip on inflationary impulses.

Marek Raczko, an analyst at Barclays in London, is in agreement.

"A delivery of 50bp could trigger a small knee-jerk rally in the pound, while a 25bp move should see a bigger sell-off," says Raczko.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Barclays expects the Bank to hike 50bp, in line with consensus.

However, "any rally should be short-lived or quickly reverse as we expect the Bank's updated forecasts show stagflationary impulses," says Raczko.

This would be a repeat of the May policy update, where the Bank hiked interest rates but issued a set of forecasts showing inflation would fall back below the 2.0% target over the medium-term while growth would fall into negative by the turn of the year.

The Pound fell in the wake of the May update, and trended lower against most majors over subsequent weeks. The GBP to EUR exchange rate has however been better supported since June's Bank of England update where it said it was prepared to act more "forcefully" on inflation.

It has since rallied back above 1.19 and the GBP to USD exchange rate this week went back to 1.22.

"A likely downward revision in growth forecasts, combined with an upward revision in inflation forecasts, pose risks to the c.150bp additional hikes priced in by year-end," says Raczko.

Barclays expects only one additional 25bp in September, with the bank leaving the terminal rate at 2%.

This would prove a significant undershoot of existing market pricing and poses a significant downside risk to Pound exchange rate levels.

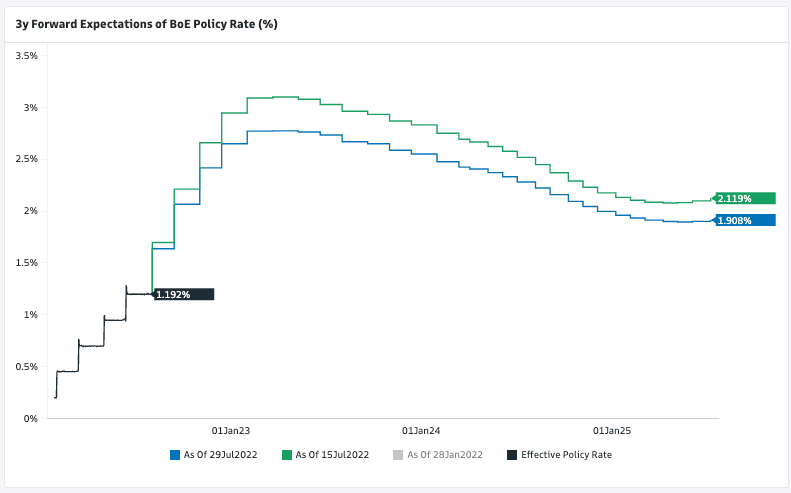

Above: Current expectations for the terminal Bank Rate are between 2.5-3.0%.

"Any mention of stagflation risks or dovish forward guidance on the future hiking path should also weigh on the pound," adds Raczko.

Currency strategists at Goldman Sachs are however more constructive on the Pound's prospects, particularly against the Euro.

They expect the MPC to hike by 50bp in a break "from the more gradual and balanced approach" the taken so far this year that has favoured delivery via 25bp increments.

"The key question for the meeting next week in our view is how policymakers will balance the strong spot wage and inflation data against the gathering storm clouds over the Euro area economy," says Zach Pandl, Co-head of FX Strategy at Goldman Sachs in New York.

"We have argued that the MPC’s more balanced approach to getting inflation lower would lead to Sterling underperformance, and we do not expect a wholesale shift away from this strategy at this meeting," he says.

Nevertheless, the FX strategy team acknowledges a 50bp hike would mark an important change in the Bank's approach, "and the Fed's move back towards a slightly more balanced strategy also makes the BoE less of an outlier to some extent".

"Taken together, and in light of the more negative outlook for the Euro, we see less of a case for Sterling underperformance," says Pandl.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks