EUR/USD Could Hit 1.02 as Trade Deficit Bites

- Written by: Gary Howes

- Deteriorating trade dynamics to weigh on EUR

- As Germany reports a trade deficit

- USD should ultimately mean revert lower says Lombard Odier

- But not quite yet

- Meaning EUR/USD can go lower still

Image © Adobe Stock

The Eurozone's newly minted trade deficit with the rest of the world is one reason to anticipate further underperformance in the Euro, according to currency analysts.

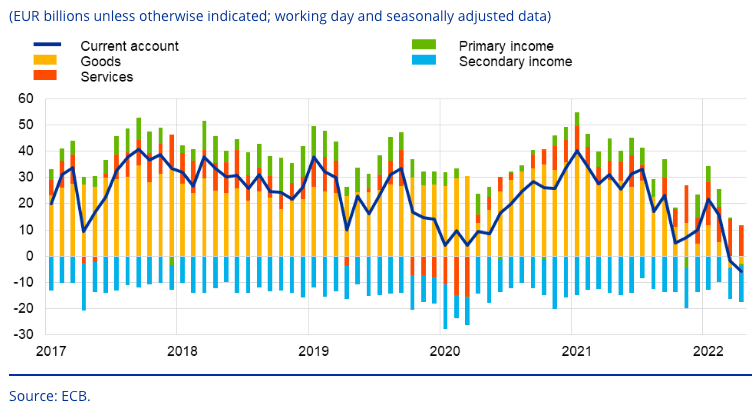

"The weakness in the Eurozone's balance of payments is real, with the current account - a previous surplus item - moving to a deficit in March for the first time since 2012," says Kiran Kowshik, FX Strategist, Lombard Odier.

Germany on Monday posted its first monthly trade deficit in goods for more than 30 years, the cost of energy imports soared and trade with Russia and China was disrupted.

The deterioration in Germany's trade deficit is contributing to a deterioration in the broader Eurozone's current account: the bloc recorded another current account deficit in April of €5.8BN.

This represents an increase of €1.6BN in the deficit on a month earlier and compares to the €31.1BN surplus printed a year earlier.

The deterioration in the Eurozone's trade dynamics is "one of the strongest bearish EUR arguments out there," says Viraj Patel, Macro Strategist at Vanda Research. "This is a structurally different macro environment for EUR. The 'twin surplus' of the '00s has turned into a 'twin deficit' post-Covid."

Above: Euro area current account balance.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes

In simple terms the deficit means Germany and the bloc are net importers, which creates a fundamental drag on the Euro.

The deficit comes amidst soaring energy costs and falling demand for the Eurozone's manufactured goods as the global economy slows.

"While we recognise the hawkish pivot of the European Central Bank, we do not assume that portfolio inflows are resuming fast or hard enough to plug the gap from he current account deficit," says Kowshik.

Kowshik and his colleagues at Lombard Odier have released their mid-year foreign exchange forecasts that show the Euro is likely to extend lower against the Dollar, although a fall to parity is unlikely.

Key to this expectation is the European Central Bank's slow exit from negative interest rates.

"While the more hawkish ECB will likely take the deposit rate into positive territory, it will remain a relative central bank laggard on the policy normalisation road. This leaves the picture for the EUR weak, in contrast to the period before 2013," says Kowshik.

The ECB is expected to raise interest rates 25 basis points later this month and follow this historic hike with another in September.

However, whether it will hike further beyond September rests with the degree of slowdown in Eurozone growth and inflation over coming months.

Lombard Odier meanwhile notes the degree of U.S. Dollar strength currently being witnessed is unprecedented in the past twenty years, and a simple mean reversion argument would suggest the dollar will peak and roll over.

"However, historically, the USD has performed strongly in the presence of three factors: global inflation over 5% year-on-year, global growth slowing, and central banks tightening policy. This last occurred in the 1980s," says Kowshik.

"Given the current global macroeconomic landscape of weak growth and elevated inflation, long U.S. Dollar exposures make sense in a portfolio context says Lombard Odier.

Lombard Odier maintain a 12-month forecast target of 1.02 U.S. Dollars vs the Euro.

Compare EUR to USD Exchange Rates

Find out how much you could save on your euro to US dollar transfer

Potential saving vs high street banks:

$2,750.00

Free • No obligation • Takes 2 minutes