Pound-Dollar Week Ahead Forecast: 1.3675-to-1.40 Range Prevails in Data Heavy Week

- Written by: James Skinner

- GBP/USD facing resistance at 1.40, support at 1.3675-1.37

- June’s inflation and job data eyed in UK after May GDP miss

- Fed testimony key for USD, Chinese data keeps RMB in focus

- Fed’s ambiguity constrains USD, global economy risks support

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3913

- Bank transfers (indicative guide): 1.3520-1.3620

- Money transfer specialist rates (indicative): 1.3780-1.3800

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-to-Dollar exchange rate enters the new week in the higher end of its likely range and could be volatile over the coming days as the market digests commentary from the Federal Reserve (Fed) while processing economic data from the UK, U.S. and other major economies.

Sterling enters the new week around 1.39 and near the higher end of a likely 1.3675-to-1.40 range after overlooking softer-than-expected May GDP data ahead of the weekend when widespread declines in Dollar exchange rates were the dominant feature of price action.

Those came after the People’s Bank of China (PBoC) injected stimulus into the world’s second largest economy with a large cut the required reserve ratio for all domestic banks, enabling them to draw down on regulatory capital worth an estimated RMB 1trillion (£112billion) in order to support lending to companies of all shapes and sizes.

This was a surprisingly aggressive move according to some economists and may say something about the likely outcome of this week’s Chinese GDP data, which comes alongside other data for the month of June and is a potential volatility risk.

However, and before then Wednesday’s testimony to Congress from Fed Chairman Jerome Powell and a host of UK and U.S. economic figures dominate the agenda for Sterling and the Dollar.

“Fed Chairman Powell delivers his semi-annual monetary policy testimony before Congress on Wednesday (afternoon) and Thursday (morning). Markets will be looking for any information around tapering,” says John Briggs, global head of desk strategy at Natwest Markets.

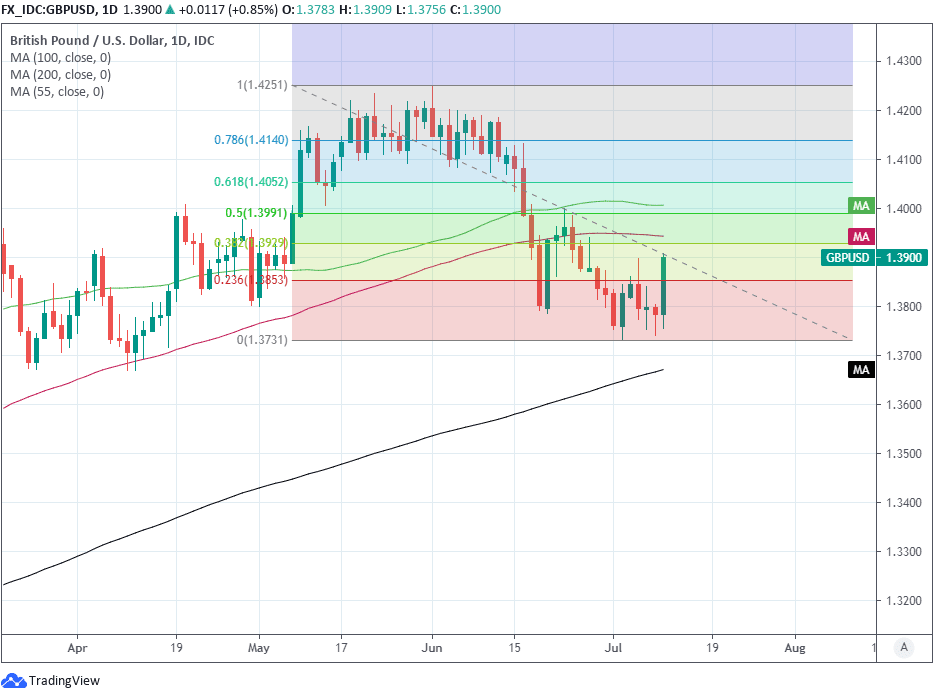

Above: Pound-Dollar rate shown at daily intervals: Benefits from a thicket of Fibonacci support levels located between 1.3675 and 1.3713, in addition to GBP’s 200-day moving-average at 1.3672.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

“We still don’t know what exactly will constitute “substantial further progress”, and we didn't learn more on what specifically is meant by “advanced notice” before any decisions on taper are made. As we have been flagging, we may get a little more insight from the Chair,” Natwest’s Briggs says.

Tuesday and Wednesday’s inflation data from the U.S. and UK could potentially lend support to the Dollar and Sterling in the wake of their release if the figures show price pressures rising further above the respective target levels of the Federal Reserve and Bank of England (BoE).

{wbamp-hide start}

{wbamp-hide end}{wbamp-show start}{wbamp-show end}

However, any such support may be fleeting and especially in the case of Pound Sterling given how both central banks see these elevated inflation rates are the result of temporary factors that are likely to fade fairly promptly and in any case by next year.

“The Fed's hawkish pivot in June is central to our bullish USD view. The Fed is on track to announce tapering at an upcoming meeting, and we continue to think the September meeting is most likely with tapering starting at the turn of the year,” says Michalis Rousakis, a strategist at BofA Global Research, who forecasts a Pound-Dollar rate decline to 1.35 by the end of September.

Above: Pound-Dollar rate shown at daily intervals. Faces a thicket of technical resistances overhead including 38.2% and 50% Fibonacci retracements of April’s corrective turn lower at 1.3929 and 1.3999 respectively, as well as 100-day moving average at 1.3944 and 55-day average at 1.4007.

Most important for Sterling and the Dollar are any remarks made by Fed Chairman Powell in Congress from 17:00 this Wednesday relating to the timing of any decision by the bank to begin winding down its $120bn per month quantitative easing programme, and the outlook for interest rates.

Many in the market have been looking for the Fed to announce a decision to begin cutting back its bond purchases from New Year, with the process likely beginning in January, although the danger is that the bank takes longer than that to make the decision.

The Dollar and all other currencies will pay close attention to the testimony for clues, with signs that the Fed is indeed becoming more confident that it’s safe to begin paring back its extraordinary support for the economy being likely to prove supportive of the greenback and a weight on Sterling.

“SMEs in China are currently under notable pressure amid subdued household consumption and rising raw material costs,” says Qu Hongbin, chief China economist at HSBC. “Considering that SMEs account for around 85% of total employment in China, SMEs’ cost pressures may easily cause higher unemployment rates, which would further dampen the already sluggish household consumption growth.”

Above: U.S. Dollar Index shown at 15-minute intervals, alongside GBP/USD, GBP/EUR and EUR/USD.

U.S. retail sales for the month of June will provide further insight into the pace of the American economic recovery at the end of the second quarter when released at 13:30 on Friday, and would be useful for investors seeking to gauge the likely timing of any possible policy changes from the Fed over the coming months although second quarter GDP data from China will garner the lion’s share of market attention in the early hours of Thursday.

“The sequential slowdown might not be obvious in the year-over-year growth rates, which would drop regardless after the hugely favourable base effects in Q1. Even the quarter-on-quarter figures might not show it,” says Freya Beamish, chief Asia economist at Pantheon Macroeconomics.

“The June activity data, however, will go some way toward revealing the extent of damage from the restrictions imposed to prevent the spread of variants. In any case, survey and near-real-time data have already raised alarm bells. Similarly, money and credit growth have slowed sharply, which, under normal circumstances would be a clear signal of a looming slowdown,” Beamish adds.

Consensus anticipates an annualised 8% increase in GDP for last quarter, which is ahead of the government’s 6% growth target for 2021 and relates to a period in which coronavirus containment measures and official interventions aimed at addressing “financial stability” risks weighed on activity.

The danger is that either the GDP data itself, or retail sales and industrial production figures relating to only the month of June which are out at the same time, reveal exactly why it was that the PBoC acted so decisively last Friday when pumping stimulus into China’s economy.

"This gives me a sense of unease. Are banks under stress? If this is the case, it implies there could be more bad loans," says Iris Pang, chief economist for Greater China at ING. “Let me be plain, this RRR cut is not a positive signal. Volatility in the market could well increase."

Any adverse data would risk weakness in the Renminbi, which could potentially incite volatility if-not outright weakness elsewhere given that many currencies are positively correlated with the Chinese one.

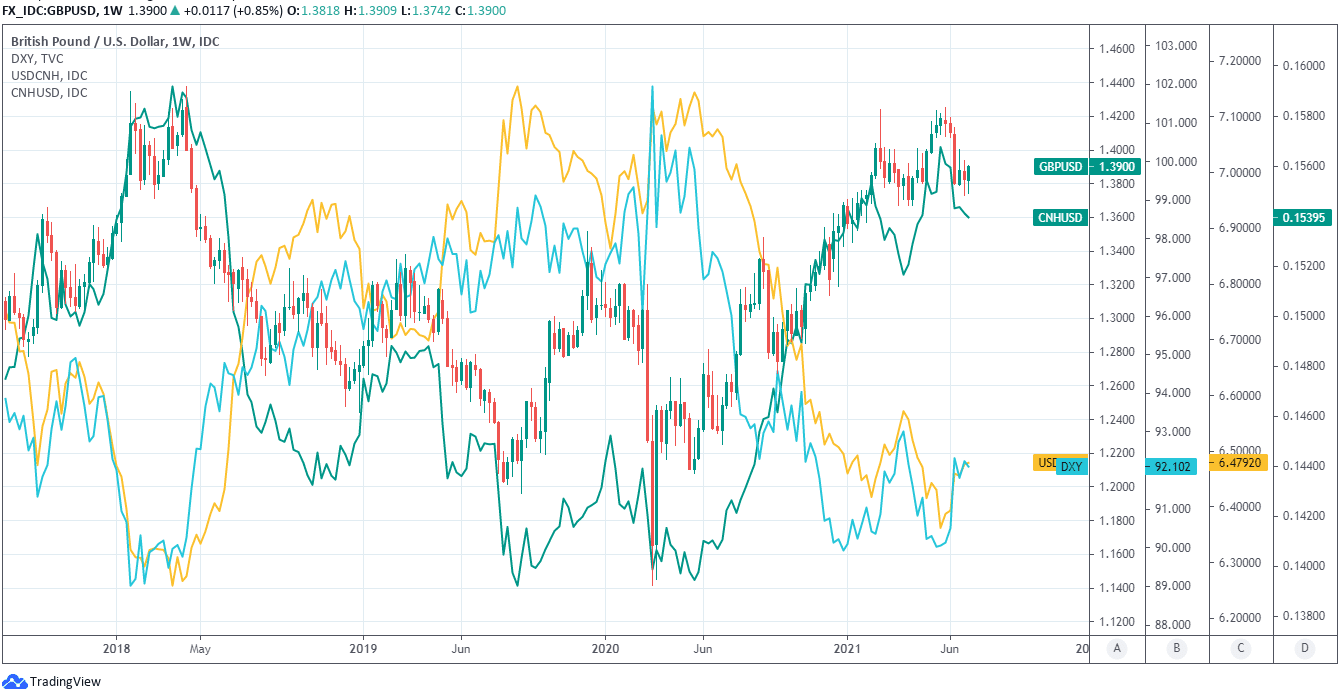

Above: Pound-Dollar rate at weekly intervals with U.S. Dollar Index, China-US exchange rate and U.S.-China exchange rate.