Gold Puts a Shine on the Swiss Franc: Bank of America

- Written by: Gary Howes

- Yen and Franc part ways

- Franc supported by Swiss trade surplus

- As gold prices soar

- Boosts export earnings for Swiss refineries

Image © Adobe Stock

The Swiss Franc would be lower were it not for Switzerland's persistent current account surplus, which could have a lot to do with the country's gold refining capabilities according to Bank of America.

The Franc's ongoing resilience has come into acute focus amongst investors as the Japanese Yen takes a battering.

The Swiss Franc shares many fundamental similarities with the Yen and is therefore proving a surprise as it refuses to follow the Japanese unit lower.

Both are considered 'safe haven' currencies and both belong to central banks with ultra-low interest rate settings and a stubborn unwillingness to change course away from negative interest rate policy.

"The one currency that should ostensibly have tracked JPY dynamics is the CHF," says Kamal Sharma, FX Strategist at Bank of America in London.

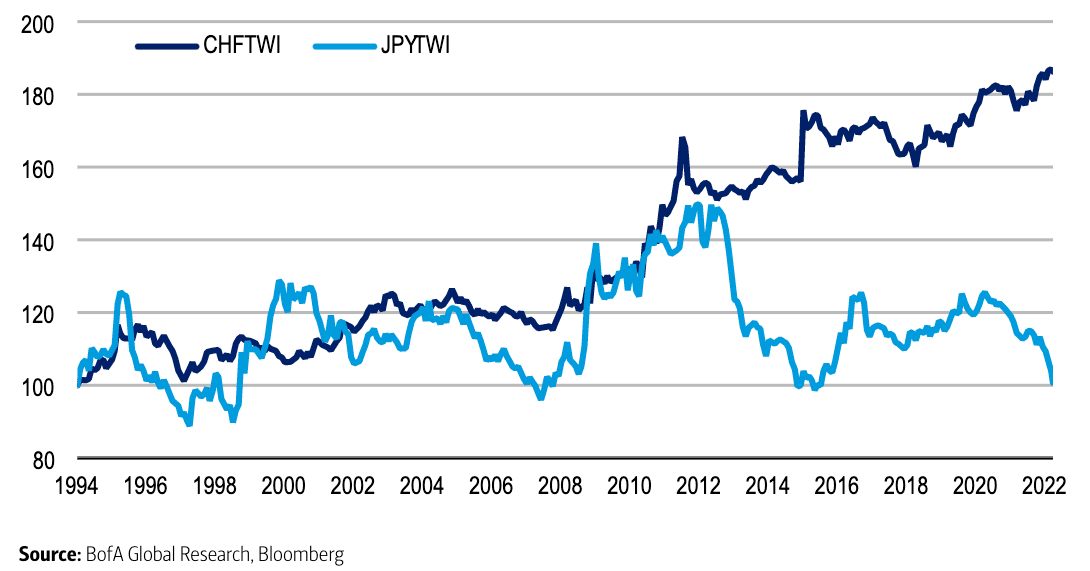

Above: The CHF and JPY part ways. "CHF versus JPY Nominal TWI performance Feb 1994 = 100 JPY and CHF performance has decoupled since 2012" - Bank of America.

Foreign exchange markets are currently highly reactive to shifts in relative central bank policy and the Bank of Japan's unwillingness to budge to a tighter policy has triggered a significant Yen selloff.

The Dollar has meanwhile continued to appreciate in value as markets bet on a rapid succession of rate hikes at the Federal Reserve over the course of 2022.

So what is propping up the Franc in an environment that should be fundamentally more hostile, and can it last?

Sharma says the sizeable global terms of trade shock which has exposed Japan's reliance on energy imports has not made a similar dent on Switzerland due in large part to its more favourable trade mix, which is skewed towards services and chemicals.

The war in Ukraine has pushed energy prices sharply higher, exposing the currencies of energy importing nations to weakness.

But Karma says Switzerland, by virtue of its leading refining facilities, has been a significant player in the global gold market.

"As a result, the Swiss trade balance has remained in surplus territory: in essence, Swiss trade resilience to the global terms of trade shock has been another reason why CHF has been more durable in the current environment," says Sharma.

"Its trade in gold perhaps explains the long standing correlation between CHF and the precious metal, a link which has weakened for JPY," he adds.

Compare GBP to CHF Exchange Rates

Find out how much you could save on your pound to Swiss franc transfer

Potential saving vs high street banks:

CHF 2,825.00

Free • No obligation • Takes 2 minutes

Four of the world's biggest gold refineries are in Switzerland, three of them in the southern canton of Ticin.

It is estimated that two-thirds of the world's gold is refined in Switzerland, which would add significant value to the country's export earnings given the sharp rise in the value of the precious metal in 2022.

According to Roberto Grassi of the Fidinam financial consultancy the situation came about as the big Swiss banks owned the refineries.

"During World War Two, because of the large amount of gold that was stored in Switzerland, the banks decided to set up their own refineries, producing bars," Grassi told the BBC.

Between 2012 and 2019 Switzerland exported 400 tonnes of gold a year on average to India and about 600 tonnes a year to mainland China and Hong Kong combined.

Swiss gold exports rose again in 2021 to their highest since 2018 as demand for bullion in China and India, the biggest consumer markets, recovered from a collapse early in the COVID-19 pandemic, Swiss customs data showed.

Gold prices have surged in 2022 as investors seek out a hedge against rampant global inflation, adding further value to Swiss exports.

"If gold is therefore being used as the commodity hedge against inflation, then the FX counterpart has increasingly been CHF and not JPY, helping to further explain the divergence between the two," says Sharma.