Swiss Franc's U.S. Treasury Clash Warns of Risks to Other Currencies

- Written by: James Skinner

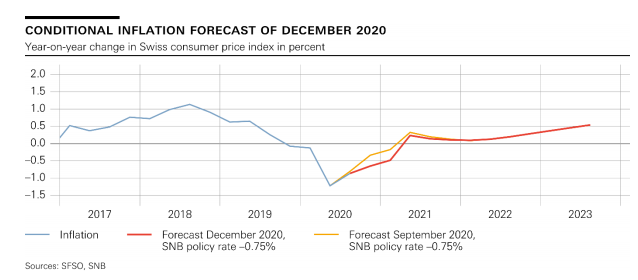

Image © SNB

- GBP/CHF spot rate at time of writing: 1.1966

- Bank transfer rate (indicative guide): 1.1417-1.1500

- FX specialist providers (indicative guide): 1.1654-1.1725

- More information on FX specialist rates here

The Swiss Franc was universally stronger on Friday if not for an unchanged USD/CHF that is at the centre of a looming confrontation between Bern and Washington, which is itself a symptom of broader global problem and a warning of growing risks that lurk along path ahead for other currencies.

Switzerland's Franc rose alongside the U.S. Dollar but not against it ahead of the weekend in demonstration of a safe-haven quality that is also a factor in a spat which threatened to escalate on Wednesday after the U.S. Treasury Department officially designated the country as a 'currency manipulator'.

"Switzerland met all three criteria under the 2015 Act over the four quarters through June," says the U.S. Treasury, after Swiss National Bank (SNB) currency transactions exceeded 2% of national GDP during the period.

U.S. officials maintain an ever-present threat to designate as a currency manipulator, any country which runs a $20 billion-plus trade surplus with the United States, carries out currency intervention exceeding 2% of GDP and which also has a current account surplus exceeding 2% of GDP.

Above: USD/CHF rate ahown at daily intervals alongside U.S. Dollar Index (black line, left axis).

The SNB's battle to achieve its elusive-yet-still-mandated targets, while buttressing the Swiss economy as it grapples with the effect of coronavirus-containment efforts have led the bank to meet the final of the three criteria after years in which the country continuously featured on Washington's watchlist.

Washington has now advocated that "Switzerland should employ a more balanced macroeconomic policy mix," as well as urged that "the SNB to deploy a broader and more balanced mix of monetary policy instruments, including domestic quantitative easing."

"The SNB unsurprisingly, countered strongly in communications after its meeting yesterday arguing that the US Treasury currency report does not adequately account for Switzerland’s particular situation. We concur with that and it is hard to lay out credible grounds to show SNB action is grounded in gaining a competitive advantage through currency manipulation," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

Source: MUFG.

U.S. Treasury officials now intend to come calling on Bern in the New Year to "press for the adoption of," exactly the policies prescribed by Washington, although the SNB at least has already made clear this Thursday that it intends to send them packing when they do. The nub of the problem is a multi-decade decline in trend rates of GDP growth that have left the economy unable to produce the 2% inflation average the SNB is charged with using monetary policy to safeguard or otherwise deliver.

This problem is not unique to Switzerland as the U.S. also suffers from it too. In fact, precipitous declines in GDP growth and inflation are endemic right the way across the developed world and are the foremost challenges faced by policymakers and political leaders alike. They are inextricably linked to, if not are, the problems which effectively installed the outgoing President Donald Trump into the White House having stoked electoral demand for his internationally-contentious 'America First' agenda.

"Switzerland has been held bang to rights. However, the criteria list and the case for the prosecution have more holes in them than a block of Emmental," says David Oxley at Capital Economics.

Source: Swiss National Bank.

"The designation is doubly insulting to the SNB because if Swiss policymakers were trying to gain a competitive advantage, they are clearly not doing a very good job! The franc is more than 10% stronger against the euro than the CHF 1.20 ceiling imposed in 2011-2015 and is close to its highest level in real trade-weighted terms since the Frankenshock," Oxley adds.

Swiss monetarty authorities have long rejected the "quantitative easing" policy prescribed by U.S. officials, which has been effective for neither the U.S. Federal Reserve (Fed) nor any other central bank which has thus far tried it. The purpose of such programmes is to force down borrowing costs for everybody by compressing government yields, which is then meant to stimulate debt-funded economic activity and so lift inflation back toward central bank targets.

Nowhere has that happened anywhere and everywhere the thus-far-failed policy has been used, in its more-than decade lifetime of experimentation. Swiss officials, having rejected involvement in the bond market, instead prefer to use newly created central bank reserves to buy U.S. Dollars and in the process lean against appreciation of the Swiss Franc relative to the Euro, which is the country's most important trading partner currency.

Above: USD/CHFrate ahown at monthly intervals alongside U.S. Dollar Index (black line, left axis).

The Franc's tendency to strengthen either because of global instability, or simply idiosyncratic economic weakness in places like the Eurozone, subsidise ever-cheaper Swiss imports of European and other goods which can reduce consumer prices and prevent the SNB from meeting its target to deliver inflation of 2%. The fact that a stronger currency disadvantages exports and so threatens the economy is a relevant, but secondary consideration for the bank.

"It’s true that Switzerland’s bilateral trade surplus with the US has blown out this year. But as the Treasury concedes, this is mainly because of a pick-up in US demand for Swiss gold during the early stages of the pandemic, which has since normalised," Oxley says. "What’s more, the steady increase in the Swiss trade surplus over the past five years or so has been driven by pharmaceuticals, which are relatively insensitive to price changes. More generally, the Treasury concedes that its criteria do not take into account services trade, in which the US has a sizeable bilateral trade surplus with Switzerland."

The foreign exchange focused SNB, when faced with a falling EUR/CHF rate that results from either a strengthening Franc or a weakening Euro, has little choice other than to sell Francs and buy Dollars because the Euro is not its own currency and the EUR/USD market may be too large for it to prop up. The mechanics of the currency market are such that the EUR/CHF rate itself is often little more than the difference between price action in USD/CHF and EUR/USD.

SNB officials said Thursday that they "willing to intervene more strongly in the foreign exchange market," where necessary, suggesting an ongoing and heightened risk of confrontation, although the squabble over the Treasury's criteria as well as relative merits of FX transactions and quantitative easing reflect an oversight of the real problem.

Above: EUR/CHFrate ahown at monthly intervals alongside USD/CHF (black line, left axis).

"The BIS Real Effective Exchange Rate as of the end of November is about 8% above the average covering the period back to 1994. The SNB message yesterday was clear – there will be no change in the monetary policy strategy," MUFG's Halpenny says. "Perhaps more importantly though, the BoJ announced a full review of its monetary policy. The review will consider “further effective and sustainable monetary easing” and is scheduled to conclude quickly, by March 2021. We see this in part as a reflection of possibly building risks of JPY appreciation through the 100-level – something we now expect next year."

The problem remains subpar inflation and falling rates of developed world growth, which becomes potent as risk to other currencies with every day that this year's U.S. Dollar decline continues. This problem and the accompanying risks will grow even larger still if this year's great, big Dollar decline really does continue at least through 2021 because in the zero sum currency market, declines for the Dollar reflect gains for somebody else's unit of account.

That in turn means cheaper imports, further weakness in consumer prices and when it comes to export or trade oriented economies; impaired competitiveness which threatens the growth outlook. In the case of the Swiss Franc, it also means more intervention from the SNB, while bringing closer the day when other lenders of last resort may also begin to consider either overt or covert involvement in the currency market.

"The coronavirus pandemic is continuing to have a strong adverse effect on the economy. Against this difficult backdrop, the SNB is maintaining its expansionary monetary policy with a view to stabilising economic activity and price developments. The SNB is keeping the SNB policy rate and interest on sight deposits at the SNB at −0.75%. In light of the highly valued Swiss franc, the SNB remains " the SNB says in its December policy decision.