Pound-to-Dollar Week Ahead: Consolidating amid Brexit Relief and after U.S. Job Surprises

- Written by: James Skinner

- GBP/USD stopped by 200-day average after best week since March.

- Faces tough resistance at 1.2675 but tipped to find support at 1.2298.

- Brexit relief washes over GBP as USD revels in May payrolls surprise.

- Job surge sees U.S. coronavirus recovery begin sooner than expected.

Image © Federal Reserve Bank of New York

- GBP/USD spot exchange rate at time of writing: 1.2667

- Bank transfer rates (indicative guide): 1.2325-2413

- FX specialist rates (indicative guide): 1.2478-1.2554

- More on acquiring market beating rates here

The Pound-to-Dollar rate notched up its largest gain since March last week but was halted Friday by its 200-day moving-average and now enters a period of consolidation in a new, higher trading range.

Sterling rose sharply on Friday after the UK's Brexit negotiator David Frost said trade talks will continue despite no progress overcoming long-standing differences in a range of areas. Prime Minister Boris Johnson had indicated that he might walk away from the table in June if it seemed unlikely a deal would be ready before year-end so the extension was a relief for the Pound.

But the rally was curtailed when the Bureau of Labor Statistics announced a surprise increase in U.S. employment for the month of May, confounding market expectations for a loss of more than 7 million jobs and another spike in the unemployment rate. Sterling ended the week with a 0.27% gain over the Dollar but it was still up some 2.58% for the period, its largest one-week move to the upside since its bounceback from 1985 lows that began on March 23.

"GBP/USD is approaching the top of the range at 1.2643/70 once again. This is the location of the 200 day ma and we would allow it to hold the initial test, dips lower should find initial support at 1.2468/86 ahead of the short term uptrend at 1.2298, which is expected to hold," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank, who has a neutral-to-positive outlook for the exchange rate so long as it's above 1.20.

The Pound has now risen for three consecutive weeks against a flagging Dollar, with much of its gains coming before the decision to extend the Brexit talks through summer, and may have slipped into a new, higher trading range since breaking back above 1.24. It has been grinding higher against the Dollar because of weakness in the U.S. currency, but a number of analysts say greenback is looking oversold following an eight-days long run of losses that was only just broken on Friday.

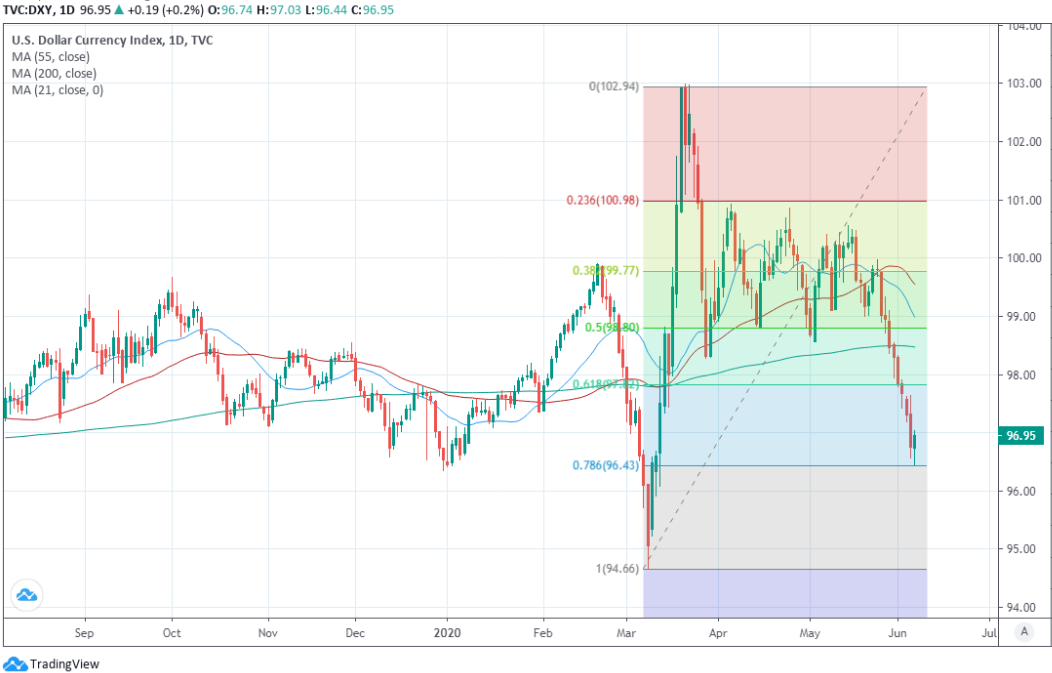

Above: Pound-to-Dollar rate with 200-day moving-average in green, uptrend support at Fibonacci retracements of March fall.

Friday's Brexit update removes an immediate headwind from Sterling's path but it's not clear if it's enough for the British currency to attract some investor interest in its own right. Talks are still deadlocked and a risk to the Pound given the lingering prospect of something like a 'no deal' Brexit playing out at year-end, and the Dollar could have recovery potential for the week ahead.

The Dollar has been sold heavily and although the outlook for it remains in question, Friday's payrolls report marked the beginning of a jobs rebound that came sooner than markets expected and could be a gamechanger for sentiment toward the currency given the pre-virus trend of U.S. economic outperformance. The U.S. economy created 2.5 million new jobs last month and the unemployment rate fell from 14.7% to 13.3% when consensus was for 7.7 million jobs lost and a jobless rate of 19.4%.

"The US Dollar has begun to turn lower, alongside a broader pro-cyclical rotation across markets. In light of its high valuation the currency’s downside could be substantial if the depreciation trend continues—perhaps in excess of 20% on a trade-weighted basis. However, further Dollar weakness will likely be uneven across regions initially. We currently see the most attractive long opportunities in non-Asia pro-risk currencies with favorable FX fundamentals—especially NOK and MXN. The Euro should benefit from Dollar weakness over time, but we would not anticipate a sharp move higher over the near-term," says Zach Pandl, global co-head of foreign exchange strategy at Goldman Sachs.

The payrolls report could be a gamechanger for sentiment in the short-term, especially in light of earlier losses and at least in relation to currencies like the lower yielding Yen, Franc and Euro, which all ceded ground to the greenback on Friday. It also helped the Dollar Index to break its losing streak and drove the Pound-to-Dollar rate back below its 200-day moving-average at 1.2675, leaving both vulnerable to corrective moves in the short-term at least.

Above: Pound-to-Dollar rate with 200-day moving-average in green, uptrend support at Fibonacci retracements of March fall.

"It is still too early to call whether the USD bull-run is coming to an end but the policies put in place to tackle the impact of COVID-19 could now be having a clearer negative influence on the dollar that may persist. Technically, the USD sell-off over the past two weeks is looking stretched and RSI measures suggest some pull-back over the short-term is feasible. But that may be the opportunity to position for a more sustained drop in the dollar. The FOMC next week will be important," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

Beyond the very short-term, the Dollar has been undermined by the optimistic mood among investors who've chosen to look past the coronavirus collapse being borne out in economic data, to position for the beginning of a new business cycle. And the broader outlook has been undermined by the colossal amount of Dollars unloaded onto the market by the Federal Reserve (Fed) during the acute stage of the crisis when the Dollar Index surged 4.5% in the week ending March 23.

Even the Brexit-blighted Pound has benefitted from these trends so Wednesday's Fed policy decision will be important for the Pound-to-Dollar rate, with markets looking for guidance on how long bond yields and benchmark interest rates are likely to be kept at current historic lows. If the Fed neglects to take any action or to commit to an extended period of zero interest rates then the Dollar could welcome the 19:00 announcement, which will be followed by a 19:30 press conference.

"USDCAD retains a soft technical undertone but USD losses have slowed through the latter part of the week as the market digests the sharp decline in spot seen on Monday. We note that some technical signals are showing signs of stretch—the USD is looking somewhat oversold—but we also note that the underlying bear trend is strongly entrenched on the short/medium term oscillators and the weekly study is poised to tilt more negative for the USD; we think scope for USD rebounds under these circumstances is limited, especially with the market yet to show any clear signs of reversing higher," says Juan Manuel Herrera, a strategist at Scotiabank.

Once past the Fed the UK economy will be in focus at 07:00 Friday with the Office for National Statistics (ONS) set to publish GDP figures for April, which was the first full month where the economy was under lock and key. Consensus favours a -18% month-on-month fall in GDP but any larger-than-expected contraction might be enough to get markets thinking about the volume of government spending and BoE easing that could yet be required to get the economy back on track.

The data could ensure a soft end to the week for the Pound if it reveals that the damage was greater than markets anticipated, more so given that the UK is yet to take any meaningful steps to reopen the economy. Supposedly non-essential retailers will be able to reopen again from June 15, but this is a full month later than the U.S. and many European economies and it remains to be seen how long it will be before the restaurant and pub trades can open their doors again.