Longer-Term U.S. Dollar Outlook "Deteriorating" says Analyst, but Near-Term Gains against the Pound and Euro Still Possible

- Imminent market sell-off to boost USD

- But effect to be short-lived

- Longer-term outlook sees USD weakness

Image © Adobe Images

![]() - GBP/USD spot exchange rate at time of writing: 1.2326

- GBP/USD spot exchange rate at time of writing: 1.2326

- Bank transfer rates (indicative guide): 1.1995-1.2080

- FX specialist rates (indicative guide): 1.2090-1.2215 >> more information

The U.S. Dollar is being tipped to outperform its rivals in the near-term, however the longer-term outlook for the currency is deteriorating according to new research.

Analysis from ABN AMRO - the Dutch-based global investment, commercial and retail bank - suggests the safe-haven buying of assets that has become associated with the coronavirus crisis should ultimately play out further and lend support to the dollar in the coming weeks.

"However, the longer-term outlook for the dollar is deteriorating," says Georgette Boele, Senior FX Strategist at ABN AMRO, regarding the multi-month horizon.

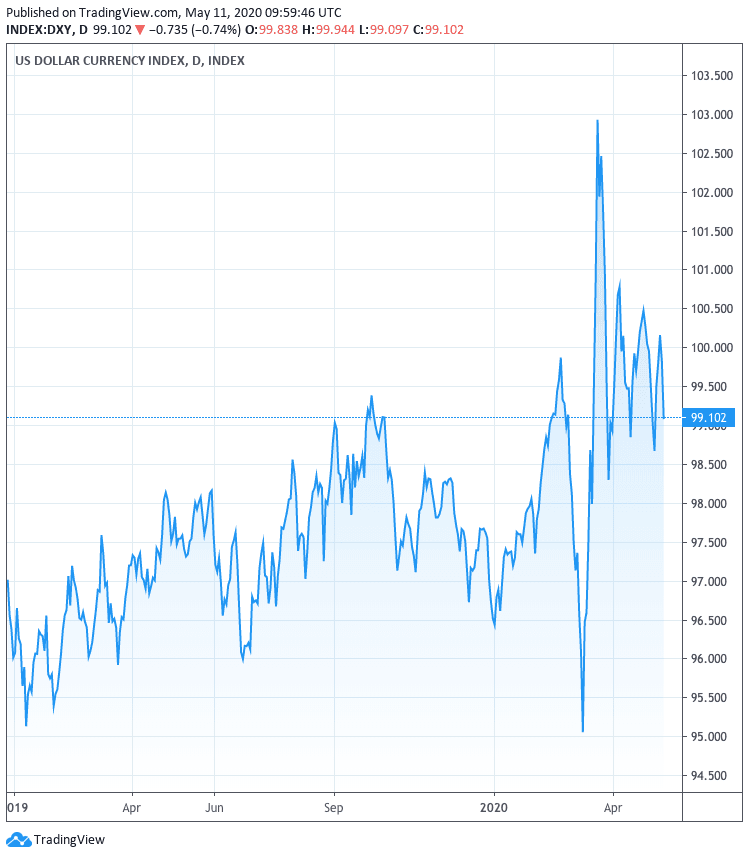

The Dollar has outperformed the majority of its most liquid peers over the course of 2020, with the Dollar index - a broad measure of overall USD performance - steadily rising over the course of the past year.

The gains peaked during a period of intense market instability as government's around the world reacted to the spread of covid-19 by shutting down their economies. The market sell-off triggered a rush to safety as demand for liquidity spiked, and while the Dollar has pared some of its gains the world's de facto reserve currency remains elevated and its broad trend remains consistent with an appreciating asset.

Looking at the Dollar's individual performances, we can see it has risen against all its major peers apart from the Japanese Yen in 2020, which is not entirely unsurprising given that the Yen is also widely considered to be a 'safe haven' in times of market stress.

The overarching theme of 'risk-on / risk-off' has ensured the Australian-U.S. Dollar exchange rate has fallen 7.8% in 2020, the Pound-to-Dollar exchange rate has fallen 7% and the Euro-to-Dollar rate is down 3.6%.

"Do we expect this trend to continue? In the near-term (up to 3 months) yes, on the longer-term no," says Boele, of the Dollar's period of relative outperformance.

The Dollar should benefit in the near-term as ABN AMRO expect another wave of risk-off in financial markets as investors are considered to be too optimistic on the speed and strength of economic recovery.

"There is an enormous gap between the economic reality and what analysts forecast, on the one hand, and the optimism among investors for the second half of this year, on the other. This should support the U.S. Dollar as most liquid safe haven currency," says Boele.

The prospect of further gains in the Dollar over coming weeks (the short-term) ultimately rests on another bout of risk aversion related to the covid-19 crisis, and we would expect a potential trigger to be a resurgence in cases in economies that have passed their peaks.

News of fresh outbreaks in China's Wuhan and South Korea are two events on our radar, which are potentially aiding the softer start to markets at the beginning of the new week.

We would also keep an eye on evolving relations between the U.S. and China with U.S. President Donald Trump looking keen to raise the heat with China as the November election approaches. Flare-ups in geopolitical anxieties traditionally favour the Greenback.

For now though the market has tended to look through any scares with weakness typically tending to be restricted and merely offering investors fresh opportunities to buy into the recovery story.

"In our view, USD upside is limited and downside pressure on the currency can re‑assert itself in part because the risk of a more severe and protracted global recession has diminished. Global lockdown measures are slowly being unwound and US April job losses were not as bad as expected," says Elias Haddad, Foreign Exchange Strategist at CBA.

ABN AMRO agree that the Dollar is due for a bout of weakness, but just not yet.

Once an expected next wave of market stresses passes, and a more sustainable recovery becomes embedded, the U..S Dollar is forecast to see its fortunes shift noticeably.

"After macro and earnings disappointments in the next few months, later this year investors could start to look forward to a strong and durable recovery in 2021. Therefore, over the medium term, investors will shy away from safe haven currencies such as the US dollar and Japanese yen and be open for alternatives," says Boele.

Another driver of long-term potential downside is the U.S. Federal Reserve which has reacted to the coronacrisis by substantially increasing the supply of dollars into both the domestic and global economy, as it adopted a 'whatever it takes' approach to the crisis.

"Never has QE been so aggressive and large in history," says Boele referring to the Fed's open-ended quantitative easing programme that sees it buy as many bonds as required to keep yields contained.

"Because of the unlimited QE by the Fed, there is already some more confidence in financial markets. As soon as safe haven demand fades, the Dollar will decline. The QE is simply too large for the Dollar to ignore," says Boele.