New Zealand Dollar Steadier on Feet but Economic Test Looms Ahead

- Written by: James Skinner

“Like Murder on the Orient Express, a plethora of headwinds are ready to stick the knife in, with higher interest rates, ongoing cost pressures, slowing construction, softer agriculture production and more cautious households in the frame,” - Nat Keall, ASB Bank.

Image © Adobe Stock

The New Zealand Dollar rebounded from near the bottom of the major currency bucket in the final session of the week but will face fresh challenges from near and afar in the days ahead when first-quarter Kiwi GDP data will be released in close proximity to the latest Federal Reserve (Fed) decision.

New Zealand’s Dollar had been among the biggest fallers in the Thursday session when the Euro slumped against almost all counterpart currencies and stock markets sold off nearly across the board in a cacophony of losses.

Those losses appeared driven by a spike in U.S. bond yields, the risk of fresh coronavirus containment measures in Shanghai and the market response to Thursday’s landmark European Central Bank (ECB) monetary policy decision.

But many currencies from across the Asia Pacific region including the New Zealand Dollar showed greater resilience on Friday even after stronger than expected U.S. inflation data prompted the market to look again at its assumptions about Federal Reserve (Fed) interest rates.

“The word of the week was stagflation, with global markets fretting about the risk of global growth stalling even as inflation pressures remain high. Surging oil prices have only added to these concerns, with oil trading at around USD120/barrel over the week (versus USD73/barrel at the start of the year),” says Sharon Zollner, chief economist at ANZ.

Above: NZD/USD shown at hourly intervals alongside S&P 500 index (blue), EUR/USD (black) and Renminbi-Dollar rate (green). Click image for closer inspection.

Above: NZD/USD shown at hourly intervals alongside S&P 500 index (blue), EUR/USD (black) and Renminbi-Dollar rate (green). Click image for closer inspection.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

“But don’t expect downside growth risks to deter global (and local) central banks from continuing to rapidly hike interest rates. Inflation pressures are still far too strong – and many central banks are really only just starting their campaigns to restore price stability,” Zollner added in a Friday note.

While the Australian and the New Zealand Dollars were among the most resilient of the G10 currencies on Friday, downside risks to economic growth will be front and centre for the Kiwi next week when Statistics New Zealand publishes its estimate of first quarter GDP on Wednesday.

This is scheduled for just hours after the Fed announces its June policy decision and economists will be pouring over the data for clues about how much longer Kiwi growth rates can hold up under the weight of multiple burdens.

“Like Murder on the Orient Express, a plethora of headwinds are ready to stick the knife in, with higher interest rates, ongoing cost pressures, slowing construction, softer agriculture production and more cautious households in the frame,” says Nat Keall, an economist at ASB Bank.

“None of these are unique challenges for New Zealand – the circumstances faced by the global economy are challenging and there aren’t any quick fixes. And its not to say the economy doesn’t have real strengths too – we are optimistic NZ exports will hold up well thanks to high prices and resilient global demand. But growth will be slower over 2022 and 2023,” Keall said on Friday.

Above: NZD/USD shown at daily intervals alongside S&P 500 index (blue), EUR/USD (black) and Renminbi-Dollar rate (green). Click image for closer inspection.

Above: NZD/USD shown at daily intervals alongside S&P 500 index (blue), EUR/USD (black) and Renminbi-Dollar rate (green). Click image for closer inspection.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

Consensus estimates suggest the market will look for New Zealand’s growth rate to have ebbed from 3% in the final months of 2021 to 0.5% during the opening quarter, although ASB’s Keall is forecasting a 0.6% growth rate.

ANZ’s Zollner and colleagues, on the other hand, have recently cut their forecast and are looking for zero growth last quarter in what would potentially prove to be a headwind for the New Zealand Dollar next week.

Even more so if the Federal Reserve, soon after any such zero growth reading, attempts to outhawk an already hawkish market with its policy decision.

“Higher local interest rates aren’t lending NZD any support, and if anything, they are exacerbating hard-landing fears, which are, in turn, weighing on domestic NZD sentiment,” says David Croy, a strategist at ANZ and colleague of Zollner.

“The USD is making a comeback ahead of next week’s FOMC meeting, which is understandable given heightened volatility. Our forecasts call for a mild appreciation from here, but if a hard landing were to occur, our forecasts would be at risk,” Croy also said on Friday.

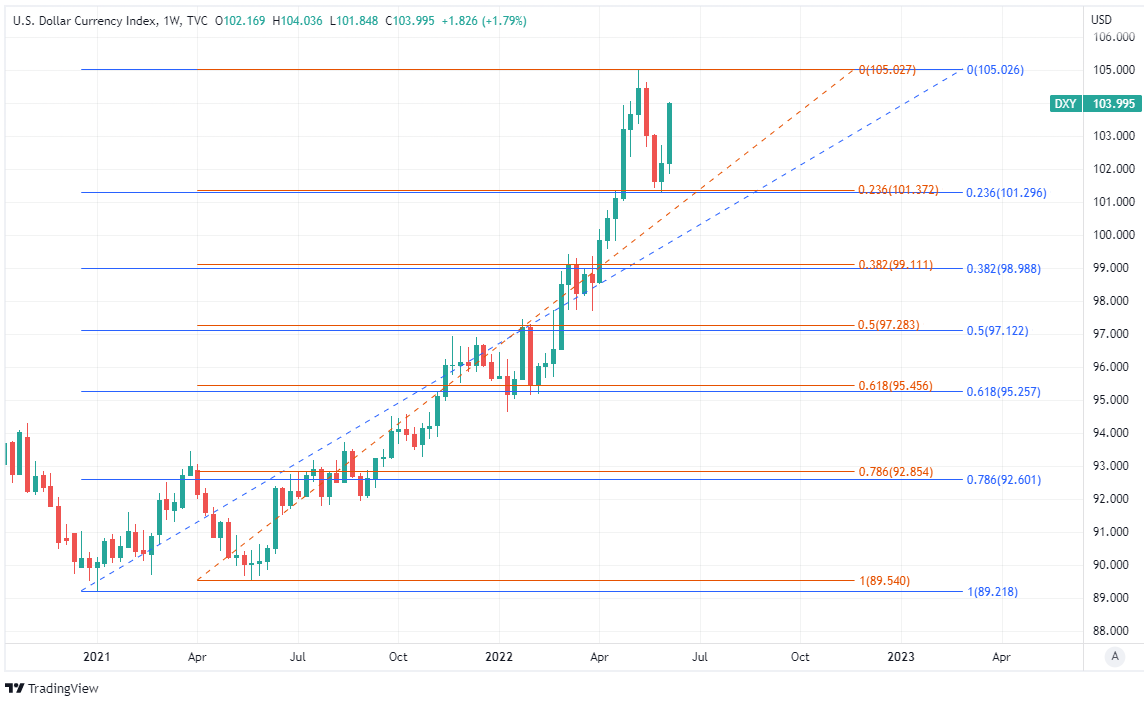

Above: U.S. Dollar Index shown at weekly intervals with Fibonacci retracements January and June 2021 uptrends indicating medium and long-term areas of technical support. Click image for closer inspection.