Riksbank in Wonderland

A central bank which pays people to borrow from it, an economy that is one of the fastest growing in Europe; non-existent unemployment hand-in-hand with virtually zero inflation - welcome to the topsy-turvy economics of Sweden.

Fear of the stalking spectre of deflation has led the Swedish Riksbank to cuts its base lending rate even deeper into negative territory, from -0.35% previously to an even lower rate of -0.50%.

The negative rate effectively means it will now pay banks a half a percent per year to borrow money from it, an inversion of the commercial relationship which would normally be the case.

Annualised Inflation in the birthplace of IKEA, the Volvo and the inimitable strains of ABBA, has remained stubbornly low at 0.1% for four months in a row to December.

However, inflation in the summer was even worse when it slumped to a yearly low of -0.4 in June.

Despite recovering from this deep low, qualms about the negative impact on inflation of break-bottom commodity prices, as a well as other global risk phenomena, such as Chinese yuan depreciation and the economic slow-down in many emerging market economies prompted a defensive manoeuvre from the Riksbank.

Most analysts had forecast a -10bps cut, however the Swedish central bank surprised with a -15bps cut instead.

In its press release the Riksbank said, “The economy continues to strengthen but inflation is expected to be lower during 2016 than previously forecast.”

Growth and Deflation Unlikely Bedfellows

The Swedish economy offers an extreme example of a wider phenomenon in which inflation remains inexplicably low despite the economy strengthening.

Growth in 2015 was relatively high at 3.7%, and is forecast to be 3.5% in 2016; and the Swedish economy has the highest employment rate in the EU.

The same has been seen, albeit to a lesser degree, in the U.S and the U.K, which have had to continually delay normalizing their monetary policy despite relatively robust growth and low unemployment.

The Riksbank has courted controversy as the first central bank in the world to cut its repo rate below zero – the ECB and BOJ have both cut their deposit rates below zero but not their lending rates.

It was also the first bank to increase interest rates following the financial crisis, a move which made it the target of much criticism.

The latest decision seems to have also led to much debate starting within the hallowed corridors and offices of the Riksbank itself, since the decision to cut was only narrowly supported by a vote of four to two.

Reaction to ECB

FX Analysts at Barclays think the Riksbank’s move was a: “pre-emptive move by the Riksbank ahead of additional policy stimulus globally and in particular by the ECB.”

The note goes on to outline how Barclays expect the ECB to cut their deposit rate by 10 basis points in March, a view which is rapidly becoming the consensus – even perhaps at the tame end increasingly dovish predictions.

Barclay’s interpret the cut as part of a new global ‘currency war’ where central banks compete to weaken their currencies in order to maintain a competitive advantage for their exporters.

They further expect this to mark the end of the bank’s easing cycle, as the strong economy and low unemployment are expected to eventually pressure inflation higher:

“Today’s decision was not unanimous with two out of six members of the Executive board, namely Deputy Governors Martin Floden and Henry Ohlsson, entering reservations against the decision and advocating an unchanged rate.

“Deputy Governor Floden also re-iterated his reservation against the decision to extend the delegation mandate for FX interventions.

“In our view, this is a clear sign of division between members of the Bank’s Executive Board and as such, we see little scope for aggressive further easing in the form of repo rate cuts. Moreover, given the SEK’s NEER undervaluation, we continue to find FX interventions as highly unlikely.”

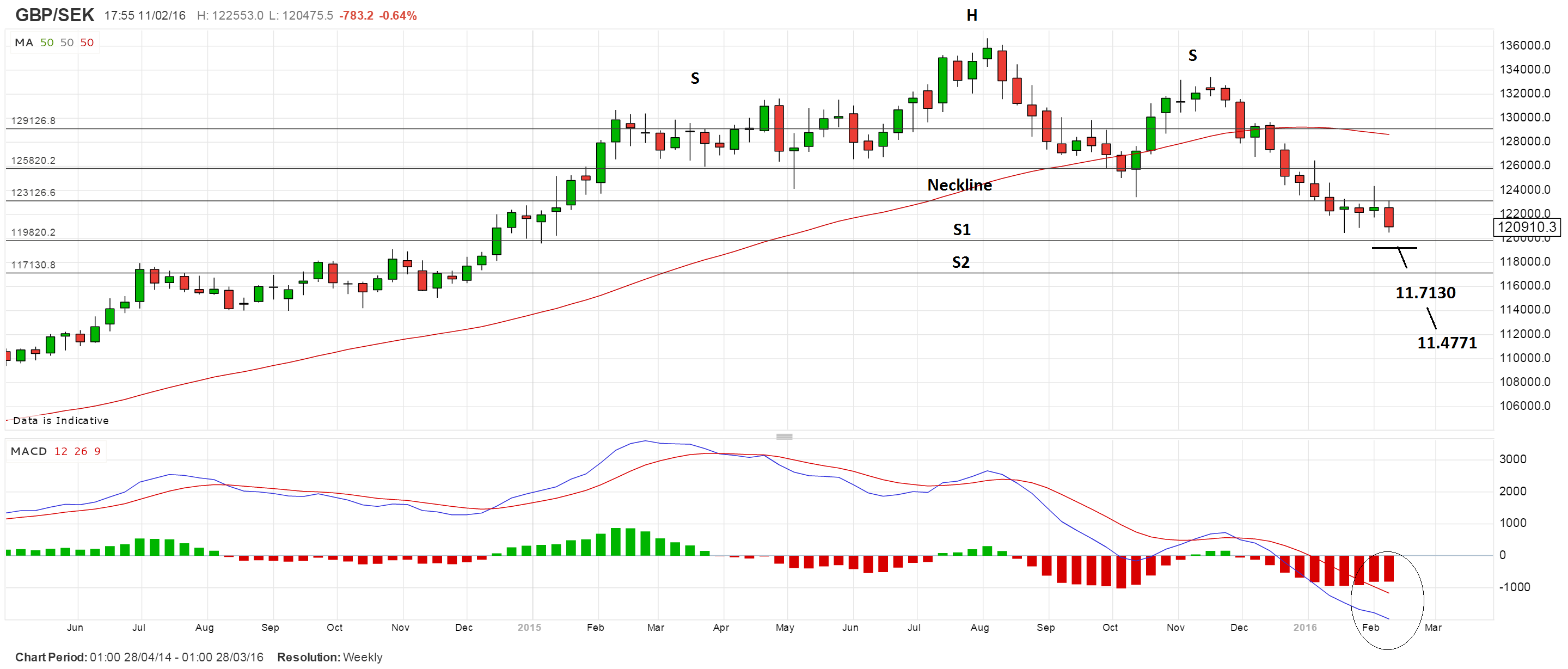

Bearish Chart

The weekly chart of GBP/SEK is showing a very bearish head and shoulders pattern along the highs.

This has already broken below its neckline at 12.3130 and has moved down to lows of 12.0458.

Using the height of the pattern you can calculate the target, which is conservatively at 11.4771, or more riskily at 10.9608.

Ideally we would like to see a break below the S1 monthly pivot just short of the current weekly lows, confirmed by a break below 11.9700.

The S2 Monthly Pivot at 11.7133 would offer the first ‘stop off’ point, however, eventually I would expect the exchange rate to fall all the way to the initial target for the pattern at 11.4771, which is the 61.8% extrapolation of the height of the pattern down, and the minimum expected target.

MACD, which is a measure of momentum is supported the bearish forecast, as it is falling sharply in line with price.