Euro's Rally against Dollar Finds it Limits

- Written by: Sam Coventry

File image of Friedrich Merz, Reichstag building, plenary hall, Berlin / Germany. Photographer: Thomas Köhler / photothek, for bundestag.de.

The euro's outlook has improved, but near-term gains might be harder to come by.

Economists who were predicting the euro would fall to parity with the U.S. dollar this year are changing tack.

Germany's recent policy shift in favour of increased defence and infrastructure spending and a slowing economy have markedly shifted the outlook.

TD Bank and Goldman Sachs are examples of two major institutions that have abandoned parity forecasts.

The increased spending, they argue, will buoy European interest rates and growth in the coming months, so there's less reason to be bearish about the EUR/USD.

However, chasing the rally from here comes with risks.

"The market narrative has quickly shifted from U.S. exceptionalism to European reflation, reflected in positioning and price action. That's where things seem to be headed in the medium term, but all transitions are complicated and often unpredictable," says Mark McCormick, Head of FX and EM Strategy at TD Bank.

The euro responded to the German and EU defence announcements by surging by 4.60% from trough to peak in March.

Above: EURUSD at daily intervals.

Another important driver of euro strength in recent weeks has been the hope of an imminent peace deal for Ukraine.

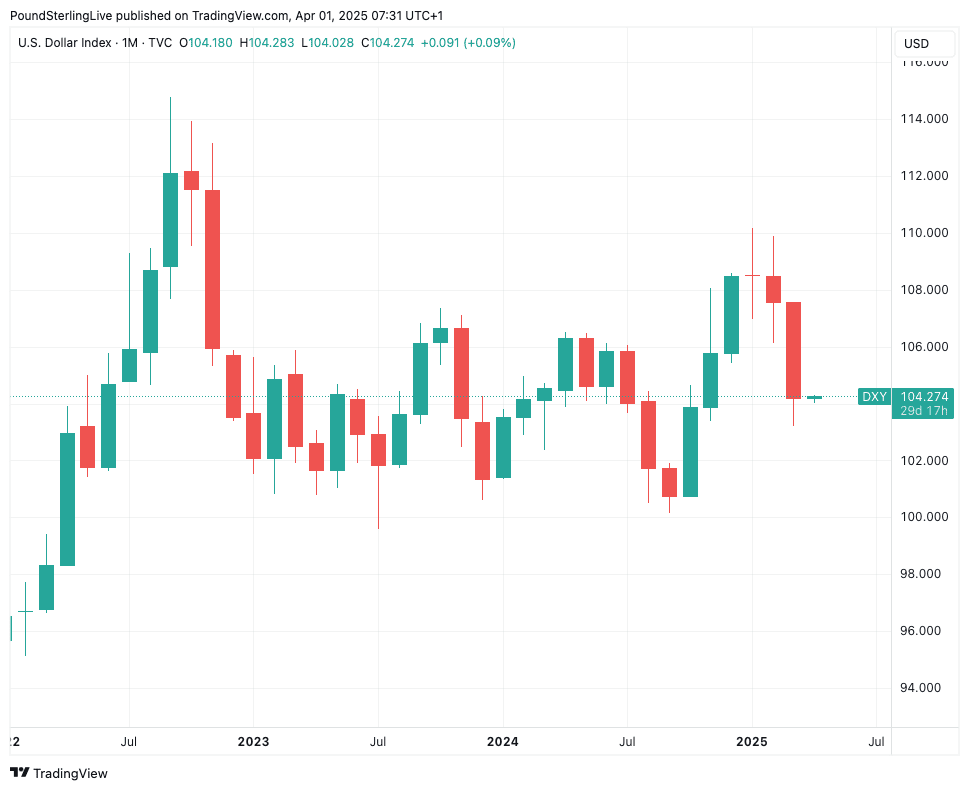

By contrast, the American currency has been bearish: February was the U.S. Dollar index’s worst month since September 2024, with a loss of 0.8% overall, but March was more significant, with a 3.14% loss on the cards.

Fading U.S. economic growth data saw the probability of a Fed rate cut in June rise to 79%.

As market participants see the Eurozone's economy reach a turning point while becoming hesitant on U.S. growth, a bullish path opens for the euro in its matchup with the dollar.

Above: The Dollar Index at monthly intervals.

Shifting to Defence and Infrastructure

In the words of Rick Meckler of Cherry Lane Investments, “The market likes certainty. It likes a plan”.

This is exactly what Ursula von der Leyen, the EU president, gave it at the beginning of March with the European Commission's defence strategy.

The feeling of confidence was augmented by the decision of Germany’s top four political leaders – Friedrich Merz, Markus Soder, Lars Klingbeil, and Saskia Esken – to establish a fund for infrastructure development worth 500 billion euros over the next ten years.

Merz also said he would adjust the constitutional restrictions on fiscal debt to open up capital flows towards defence and infrastructure.

But There's a Time Lag

Yet these moves appear to be good news for Europe’s biggest economy in the long term, and "we do... think that things can get worse before getting better", says BNP Paribas.

On Europe’s more imminent horizon is a trade war that looks set to limit the bloc's recovery potential.

Indeed, ING say the key factor guiding the euro will be “the eurozone’s structural unpreparedness to face the consequences of Trump’s tariffs”, which “continues to form the basis of our bearish EUR view”.

"Germany's fiscal move is a game changer, but it will take time. Months and quarters, not days and weeks. Now that sentiment and positioning is super bearish the USD, it's time to be data dependent again. None of the high frequency data we track validates the EUR's recent move," says McCormick.

Interest Rates Can Still Support USD

Concerns about slowing U.S. growth convinced some analysts to anticipate more than three Fed rate cuts this year.

However, with U.S. inflation rising again, this might prove optimistic.

"We think this is exaggerated and maintain our expectation of a maximum two cuts this year," says BNP Paribas, while also expecting the European Central Bank to cut rates twice in 2025, each time by 25 basis points.

The interest rate differential would then favour dollar dominance over the euro in currency trading. ING also expects a maximum of two Fed rate cuts this year and that the Fed won’t be moved to change their minds by the weak consumer data.

Near the end of February 2025, several Fed members, including Beth Hammack, said they would hesitate to lower interest rates further before seeing concrete data on the economy’s response to last year’s cuts.

For Hammack, the risk of reheating inflation is still considerable, "and this will likely mean holding the federal funds rate steady for some time", she says. This casts doubt over that 79.1% certainty of a rate cut in June since – at least much of the time – the Fed do mean what they say.

Structural Headwinds

Trade uncertainty remains the single biggest headwind for Europe’s economy, with some economists suggesting it can knock as much as 0.5% off real GDP in the first three quarters of the year.

Plus, there is the ongoing problem of European manufacturers losing business to the Chinese as energy prices in Europe remain above long-term levels.

Energy costs are well below the highs they saw after the Russian invasion of Ukraine, but, as of mid-February, natural gas prices were still relatively high – holding at $14 per million British thermal units (BTUs), as compared with the price of US natural gas futures at the time, which was only about $4.23 per million BTUs.

These structural obstacles may keep Eurozone enthusiasm muted in the months ahead, which would hamper the euro’s potential to gain.