UK Economy Suffers Unprecedented Crunch According to Flash PMIs

- Current crash greater than crash of 2008-2009

- Service sector activity comes to virtual standstill

- Complete halt to activity avoided thanks to financial services

Image © Adobe Images

The UK economy suffered an unprecedented seizure in the March-April period according to the first wholistic set of data covering the coronavirus lockdown period and economists are warning that the recovery out of the crisis will be slow.

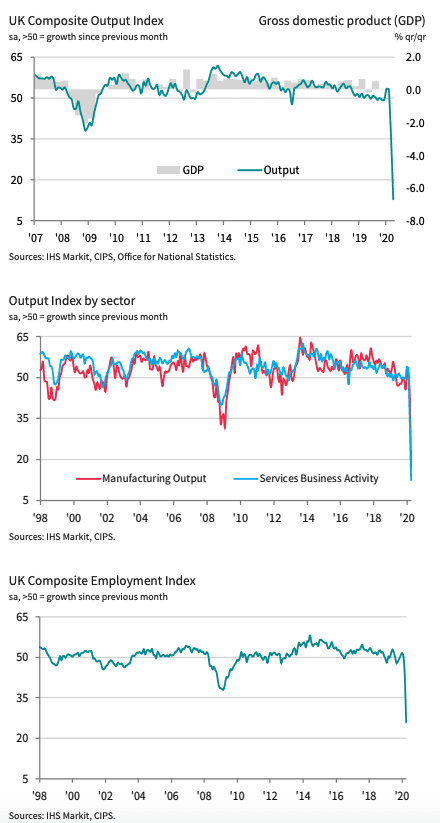

The IHS Markit Composite PMI for April read at 12.9, which is substantially below the 31 that was expected by the market and well below the 36 reported in March, which signals GDP could be down by around 6% in the past month alone.

The decline in economic activity was primarily driven by a slump to 12.3 in the Services PMI, which is well below the 29 forecast and the previous month's reading of 34.5.

The Manufacturing PMI came in at 32.9 which is again lower than consensus forecasts at 42 and below the previous month's reading of 47.8.

According to IHS Markit the collapse in economic activity was driven by widespread business shutdowns at home and abroad in response to the coronavirus disease 2019 (COVID-19) pandemic. The decline in the Composite PMI signalled by far the fastest decline in business activity since comparable figures were first compiled over two decades ago.

"The eye-watering declines in April’s flash PMIs confirm the lockdown has pushed the economy into a recession of unprecedented speed and depth. Particularly worrying was the large drop in the employment balance, providing further support to our view that a perfect V-shaped recovery is extremely unlikely," says Ruth Gregory, Senior UK Economist at Capital Economics.

The data signals that the economy is undergoing a fall that easily exceeds the downturn seen at the height of the global financial crisis of 2008-2009.

Around half of all survey respondents reported lower staffing numbers in April, although IHS Markit say there were numerous reports that the fall reflected the use of the UK government scheme to place employees on furlough.

The reaction by Sterling has been rather sanguine, after all the fall in the UK's economic activity is matched by that of its Eurozone counterparts. We saw earlier a similar fall in activity reported in Australia. In short, the world's major economies are all lumped into the same basket and this does not interest currency markets.

Rather, it is the escape velocity from the crisis that could have more of an impact.

"The sharp decline in UK PMIs emphasises the sheer scale of the economic hit from Covid-19. But the more important concern now is the recovery, and despite bold economic measures from the government and Bank of England, we expect this to be a slow process," says James Smith, Developed Markets Economist at ING Bank.

Bigger the lockdown in April = Bigger the fall in April services PMI reading.

— Viraj Patel (@VPatelFX) April 23, 2020

Latest figures (Share of Consumption in GDP):

???????? 19.6 (75%)

???????? 22.8 (75%)

???????? 10.4 (77%)

???????? 15.9 (72%)

???????? 11.7

???????? 12.3 (84%)

Global Consumer Recession pic.twitter.com/ObrcGM2e7a

Goods producers overwhelmingly linked lower output to plant shutdowns or reduced production capacity, as well as cancelled orders across manufacturing supply chains following the COVID-19 pandemic. In manufacturing, the sharpest drop in output was registered in the textiles & clothing sector, largely reflecting collapsed demand from the retail sector, though the transport sector, including car production, also reported an especially steep decline.

The manufacturing sector was understandably left better off than its services sector counterpart, which accounts for over 80% of UK economic activity.

This is understandable given the complete shutdowns of pubs, restaurants, hotels and other socially-orientated businesses.

Customer-facing service providers often reported a complete shutdown of their business operations in April amid the public health emergency, while a wide range of survey respondents commented on weaker demand following temporary closures among their clients.

According to IHS Markit the least marked downturn was seen in financial services, though even here the scale of the decline was unprecedented, joining all major sub-sectors of services seeing record falls in business activity by wide margins.

Concerning the outlook, Capital Economics say that on past form, the PMI survey is consistent with GDP contracting by at least 6% m/m in April, far sharper than any of the monthly falls seen during the global financial crisis.

"Given the PMIs measure how widespread rather than how deep the falls in output are and do not cover the retail sector, the survey is not even capturing the full extent of the damage. We think that the actual fall in GDP in April may be nearer to 20% m/m and that for as long as the lockdown is in place, output will be about 25% below its normal level," says Gregory.

Economists at ING do expect a partial rebound in economic growth in the third quarter assuming the harsher elements of lockdown are eased over the next couple of months. "But more importantly, we don’t expect the UK economy to recover to its pre-virus size until 2022 at the earliest," says Smith.

Smith expects businesses and consumers generally to remain very wary about spending decisions until the virus threat has gone, particularly given the increasing consensus that this could take quite some time.