RBS: Chinese Yuan Must be Devalued 20% as China Bleeds Private Capital

No wonder the US dollar is higher - $170 BN worth of private Chinese capital fled the country in December alone, and signs are the flow is accelerating.

Chinese authorities are making what appear to us to be bizzare and desperate attempts to maintian the value of their currency. It is argued that until they realise the CNY needs to be lower, and more action taken, Chinese investors will continue to shift their capital out of the country.

The issue if Chinese investment could answer part of the question as to where the US dollar is headed in 2016.

Higher interest rates in the US will suck up global capital which is hungry for yield, thus forcing up the value of the dollar. We must now ask where the majority of this money is coming from.

The answer is China; yes, everything financial leads us to China in 2016 it seems.

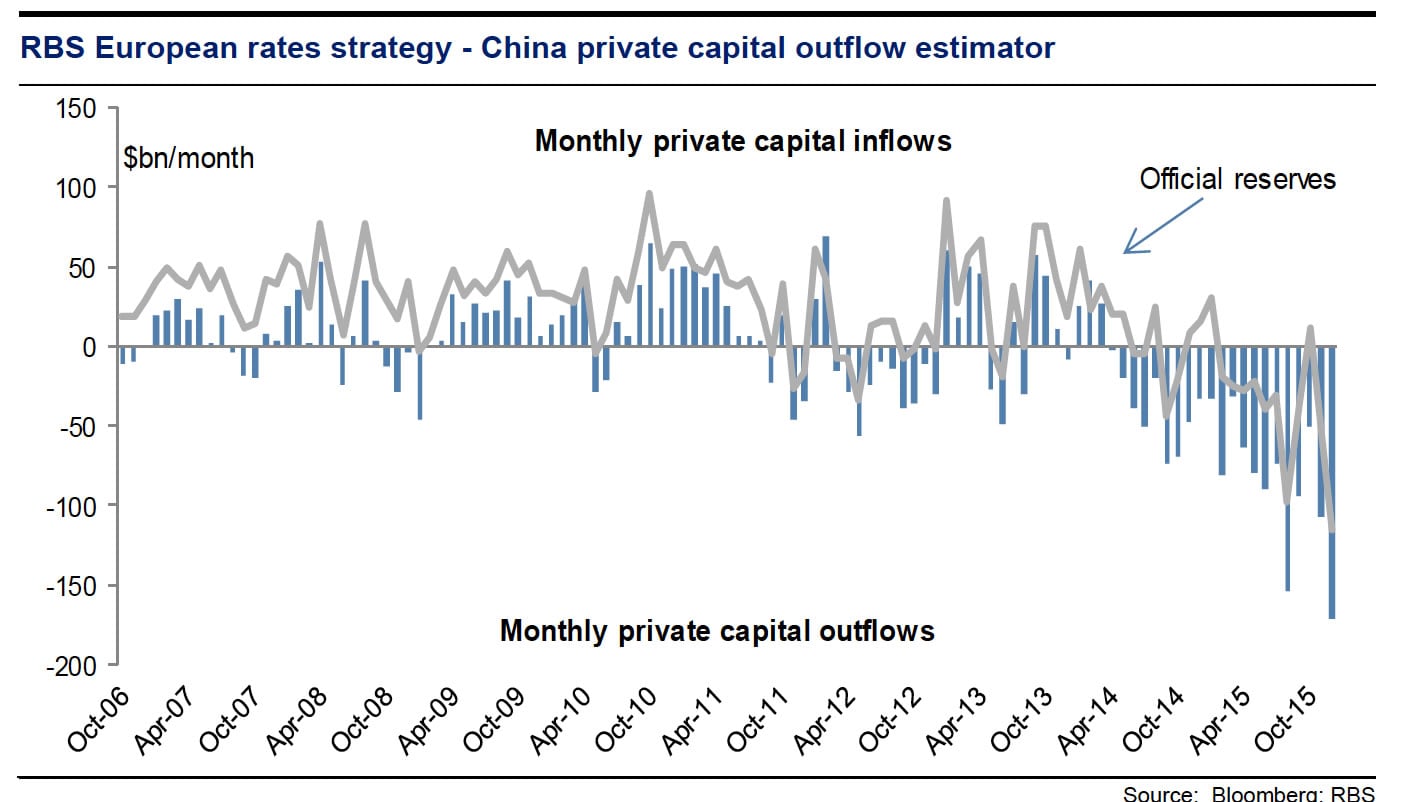

This is the Most Important Chart in the World

Analysis by Giles Gale, Head of European Rates Research at RBS in London suggests that around $170bn worth of private capital left China in December (subject to confirmation from the current account balance and FDI data).

That is $170 BN worth of capital being converted into dollars.

The chart tells us we are now witnessing record outflows.

“Small wonder then that the USD is rising, since this is money going straight back into USD, whereas the offsetting flow – selling of reserves – is spread across many countries,” says Andrew Roberts, Giles’ colleague and Head European Research at RBS.

And, JPMorgan's Fixed Income analysts warn that, "the Chinese capital outflow picture appears to have entered a new phase in [the third quarter], broadening to include foreign direct investment and portfolio instruments, something that could make future capital outflows practically boundless."

This capital could arguably be put to more productive use being reinvested in the Chinese economy. If it were left in Chinese shares then perhaps we would not have seen the eye-watering losses witnessed over the start of 2016.

RBS’ FX team do caution that while the biggest holding is in USD, it is certainly not 100% of the reserve holding.

“For our purposes, what counts is that this outflow is accelerating,” says Roberts; we in turn read between the lines and assume demand for the US dollar is also accelerating.

Roberts has named the above chart “the most important chart in the world” as it shows the extreme urgency for China to get its FX rate where it should be if it wants to hold onto its precious capital.

“With a severely over-valued currency, the problem they face in our view is continual enormous capital outflow, which has to be stemmed by reserves shrinkage,” says Roberts.

Roberts reckons the Chinese Yuan should be 20% lower than where it is now if the outflow is to be arrested.

It has fallen in the region of 6% since mid 2015 but the overarching argument put forward by the research team at RBS is that more devaluation in the Yuan is needed, and it is needed quickly.

Roberts says he will never regard high reserves as a sign of strength, “the world seems somewhat perverse in thinking this, but it is certainly the case that the worst case for China was always going to be ‘do nothing, let capital outflow (bad for the domestic economy), offset by reserve selling, and when reserves run out, then devalue, but from a position of weakness’.”

This seems inconceivable in the opinion of the RBS economist.

“It is possible, of course, but as we have been arguing for months, it is just totally illogical. Which makes the status quo on FX very unlikely to prevail in my opinion,” says Roberts.

Currency Wars to Heat Up

The message we are getting is that further CNY devaluations will be coming our way in 2016 as the global currency war intensifies.

The two protagonists are likely to be the Eurozone and China, each desperate to ensure their currencies are low enough to boost flagging demand for their goods on the global stage.

Should they succeed then the euro and Chinese Yuan will be lower at the end of 2016 - and the dollar will thus have to be higher.

“China’s real effective exchange rate has risen rapidly and China’s competitiveness loss is acute. As China’s growth now slows, this looks inappropriate and we think the renminbi weakens steadily in 2016,” says David Simmons, Head of Currency Research at RBS.

As the currency depreciates, currency flight accelerates and reserves fall faster.

This certainly plays into the pro-USD theme favoured by the majority of currency strategists as falling reserves will be achieved by releasing billions of US dollars onto the global markets. In fact we argued last year that the mid-2015 USD slow-down may have had its roots in the cutting of Chinese reserves.

Importantly, devaluaing the Chinese currency will stem private capital outflows as the Yuan will not be able to buy as much as it once could on the global stage and capital is put to more profitable use within China.

“As USD/CNY rises in 2016, we think USD/Asia rises too,” says Simmons.