Pound Sterling Fights Back against Euro, But JP Morgan Looks For Deeper Losses

- Written by: Gary Howes

- GBPEUR fights to hold 1.15

- Short-term rebound potential ahead of month-end

- Slump in Eurozone money supply undermines EUR outlook

- But JP Morgan prefers EURGBP lower still

Image © Adobe Images

The Pound to Euro exchange rate has stabilised above the 1.15 mark in line with a broader consolidation of Pound Sterling after a torrid month of losses left it oversold on a technical basis, but the outlook still favours further losses according to a major Wall Street bank.

Analysts at JP Morgan maintain the Pound can fall against the Euro and Dollar in the coming weeks, even if consolidation in GBP exchange rates looks to be the theme as we step into October.

"The Bank of England left rates unchanged which is a clear negative for Sterling given the sell-side consensus for a hike," says analyst James Nelligan at JP Morgan in a recent briefing to clients.

Pound-Euro on Monday was just below 1.15 where it appears some near-term support might be building, which is consistent with a need for consolidation in other major GBP exchange rates that have reached oversold conditions.

Most notable are the Pound-Dollar and Pound-Canadian Dollar pairs which have entered deeply oversold levels - not seen since the height of the Truss mini-budget crisis - and corrections here would make a short-term rebound across the entire Sterling complex more likely.

But, strength will be limited according to JP Morgan wich looks for the broader story to be one of decline for the Pound as the spread between UK and Eurozone (and U.S.) bonds remains unsupportive in the wake of the Bank of England decision to halt hiking.

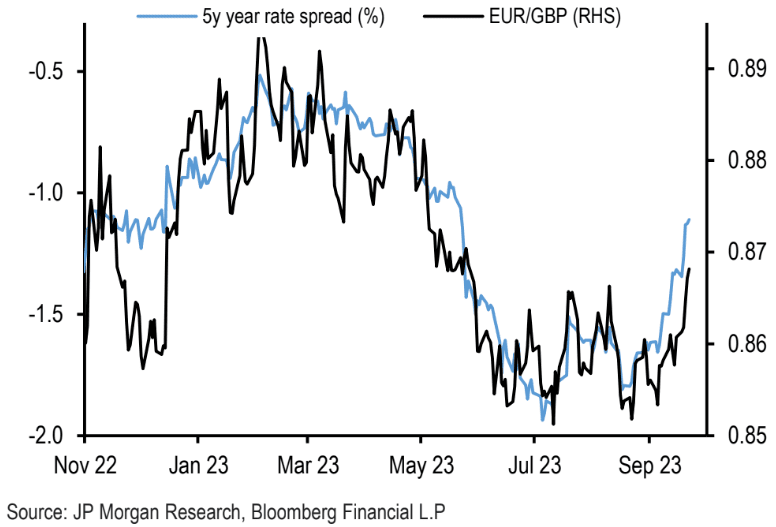

"EUR/GBP is still lagging rate spreads (above 0.87 implied) but our preferred expression is GBP/USD (low-end fair value 1.21). Rate spreads suggest EUR/GBP should be above 0.87," says Nelligan.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

UK bond yields had outperformed peers in Germany, the U.S. and elsewhere up until August because markets were expecting the Bank of England to deliver more hikes than peers as it battled inflation.

But these expectations faded amidst cooling domestic data, culminating in the Bank last week calling a stop to the hiking cycle, saying it believed it had raised rates enough to ensure inflation would continue to fall steadily towards its 2.0% target.

The Bank's guidance attempted to convey it would maintain a tightening bias, but there were some dovish elements to the statement with the MPC noting that "the recent acceleration in the AWE not apparent in other measures of wages".

Above: "EUR vs GBP 5y swap rate spread, EUR/GBP spot" - JP Morgan.

JP Morgan says the Bank's reference to declining alternative measures of wage growth "is interesting" and that's partly a nod to the small decline in private sector wage growth seen in the last print.

Commentary on the labour market elsewhere in the statement still cites the overall picture as tight.

Economists we follow say the Bank's decision to skip a rate hike, despite this tight labour market and inflation being amongst the highest in the developed world, could be a mistake. Indeed, we have heard numerous views suggesting the decision represents a hit to the Bank's credibility.

"The UK is one of the few countries for which we really see a wage price spiral in the making. The Bank of England decision to skip is not very reassuring. The pound is at risk," says Ludovic Subran, Chief Economist at Allianz.

Subran says the UK could be about to see "knee-jerk reactions" by the Bank to incoming data that could potentially result in a "stop-and-go hiking cycle".

JP Morgan's economists meanwhile say the bar is now set high for future hikes given recent shifts in key data and they hold a forecast for Bank Rate to be on hold for this year and next year.

EUR/GBP is still lagging rate spreads, which implies to the strategy team EUR/GBP should be above 0.87, which gives a Pound-Euro conversion below 1.15.

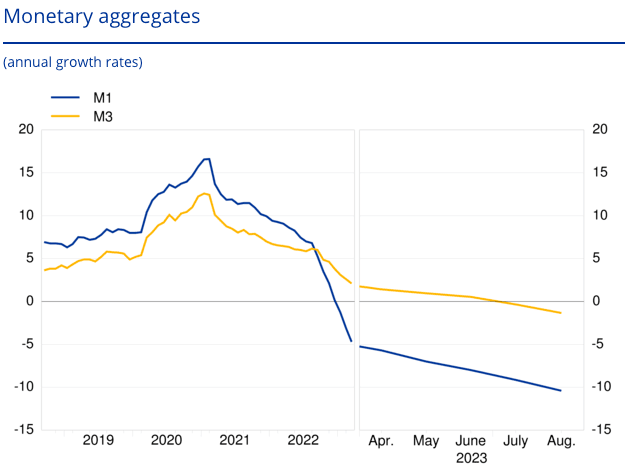

Euro Under Pressure As Money Supply Plummets

Part of the Euro's recent loss of momentum against the Pound can be explained by the midweek release of Eurozone money supply data.

M3 money supply - a gauge of money flowing through the economy - fell 1.3% year-on-year in August, suggesting the impact of the European Central Bank's interest rate hikes is being felt.

The implication of a falling money supply is weakened demand and, ultimately, lower inflation.

Image courtesy of the ECB.

"Annual M3 growth has slowed from more than 12% in early 2021, and almost 4% at the end of 2022, to -0.4% as of July. That reflects the impact of higher interest rates," says Rhys Herbert, an economist at Lloyds Bank.

Alex Kuptsikevich, senior market analyst at FxPro, says such a contraction in money supply and credit significantly dampens the region's economic outlook.

"Unlike in the US, in Europe, most loans are made at floating rates, so an increase in the ECB's key rate simultaneously tightens the conditions for both new and existing loans. Thanks to this feature, the transmission mechanism of monetary policy works faster. As a result, fewer rate hikes are needed to cool the economy and, through it, inflation," says Kuptsikevich.

The ECB could therefore find it has tightened enough.

This puts the ECB and Bank of England in a similar situation, which suggests there should be limited scope for the Euro to advance much further as Eurozone yields will struggle to outperform.